Answered step by step

Verified Expert Solution

Question

1 Approved Answer

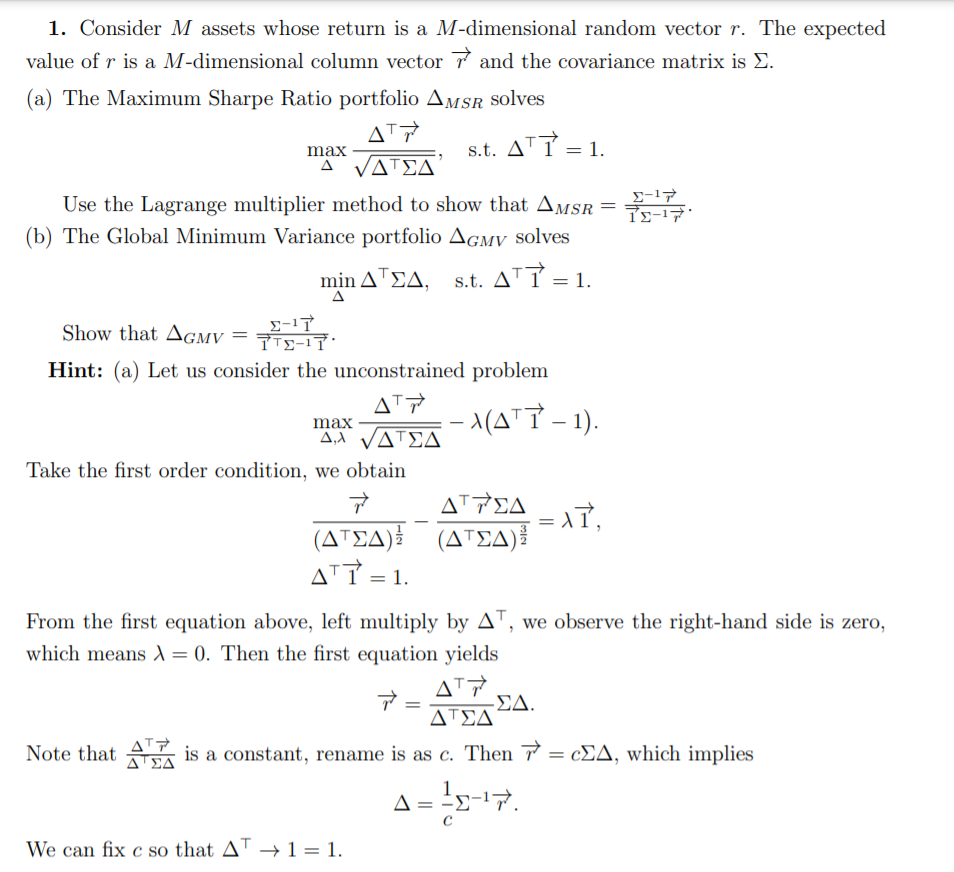

Solve a by using hint 1. Consider M assets whose return is a M-dimensional random vector r. The expected value of r is a M-dimensional

Solve a by using hint

1. Consider M assets whose return is a M-dimensional random vector r. The expected value of r is a M-dimensional column vector i and the covariance matrix is . (a) The Maximum Sharpe Ratio portfolio AMSR solves AT , max s.t. ATT = 1. AVATEA Use the Lagrange multiplier method to show that AMSR = 9-17 15-17 (b) The Global Minimum Variance portfolio AGMV solves min ATSA, S.t. ATT = 1. = 17, Show that AGMV 9-11 TTE-IT Hint: (a) Let us consider the unconstrained problem AT max - MATT - 1). 4,4 VATSA Take the first order condition, we obtain ATTA (ATEA) (ATEA) ATT = 1. From the first equation above, left multiply by AT, we observe the right-hand side is zero, which means 1 = 0. Then the first equation yields ATT . Note that AT is a constant, rename is as c. Then m = c2A, which implies A= 1 = 29-17). We can fix c so that AT +1=1. 1. Consider M assets whose return is a M-dimensional random vector r. The expected value of r is a M-dimensional column vector i and the covariance matrix is . (a) The Maximum Sharpe Ratio portfolio AMSR solves AT , max s.t. ATT = 1. AVATEA Use the Lagrange multiplier method to show that AMSR = 9-17 15-17 (b) The Global Minimum Variance portfolio AGMV solves min ATSA, S.t. ATT = 1. = 17, Show that AGMV 9-11 TTE-IT Hint: (a) Let us consider the unconstrained problem AT max - MATT - 1). 4,4 VATSA Take the first order condition, we obtain ATTA (ATEA) (ATEA) ATT = 1. From the first equation above, left multiply by AT, we observe the right-hand side is zero, which means 1 = 0. Then the first equation yields ATT . Note that AT is a constant, rename is as c. Then m = c2A, which implies A= 1 = 29-17). We can fix c so that AT +1=1Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Focus On Personal Finance

Authors: Jack Kapoor, Les Dlabay, Robert Hughes

3rd Edition

0073382426, 9780073382425