Answered step by step

Verified Expert Solution

Question

1 Approved Answer

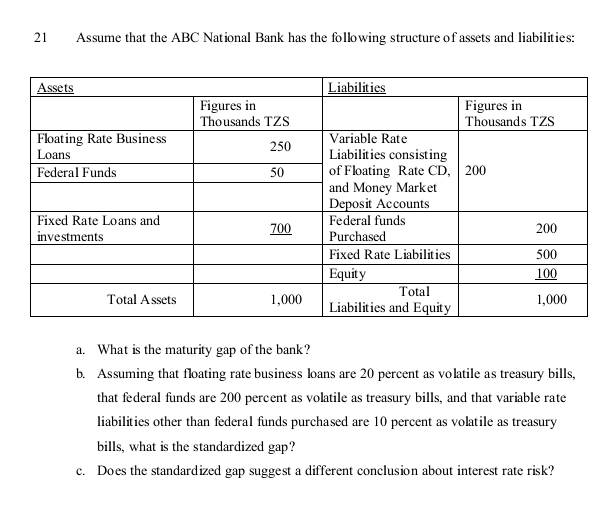

solve a question above Assume that the ABC National Bank has the following structure of assets and liabilities: a. What is the maturity gap of

solve a question above

Assume that the ABC National Bank has the following structure of assets and liabilities: a. What is the maturity gap of the bank? b. Assuming that floating rate business loans are 20 percent as volatile as treasury bills, that federal funds are 200 percent as volatile as treasury bills, and that variable rate liabilities other than federal funds purchased are 10 percent as volatile as treasury bills, what is the standardized gap? c. Does the standardized gap suggest a different conclusion about interest rate riskStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals Of Futures And Options Markets

Authors: John C. Hull

4th Edition

0130176028, 9780130176028