Answered step by step

Verified Expert Solution

Question

1 Approved Answer

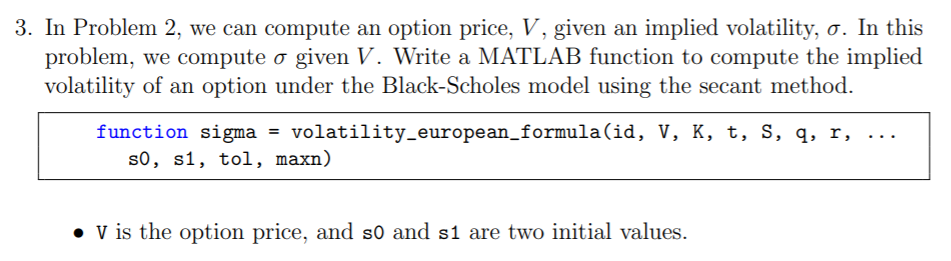

Solve in Matlab!! 3. In Problem 2, we can compute an option price, V, given an implied volatility, o. In this problem, we compute o

Solve in Matlab!!

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Demystifying Databases A Hands On Guide For Database Management

Authors: Shiva Sukula

1st Edition

8170005345, 978-8170005346