Answered step by step

Verified Expert Solution

Question

1 Approved Answer

solve step by step showing computations 2. Consider the following two investments: a=0.02500.025313131b=0.030.0150.02313131 (a) Compare these two assets using the Mean Variance criterion. (b) Write

solve step by step showing computations

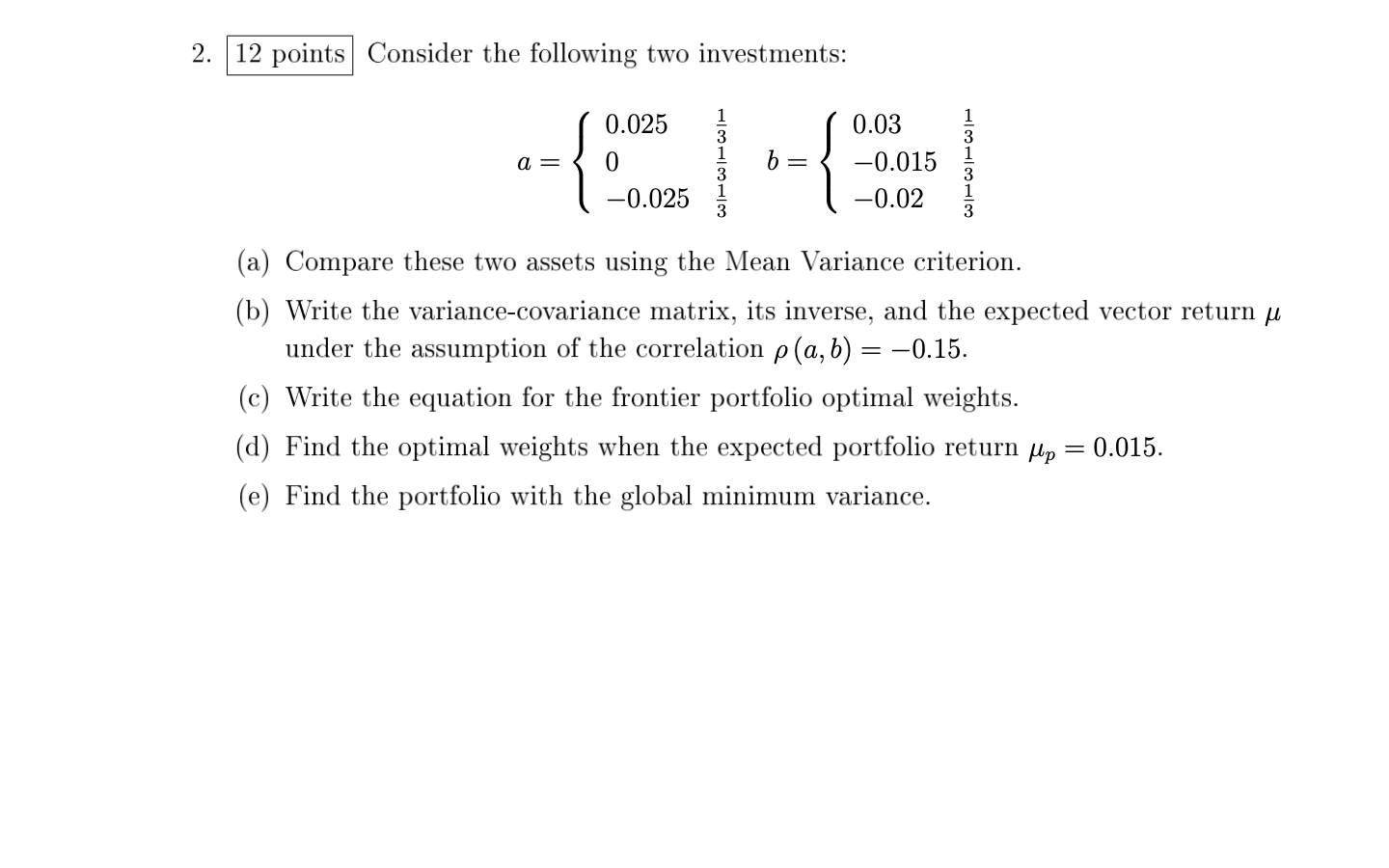

2. Consider the following two investments: a=0.02500.025313131b=0.030.0150.02313131 (a) Compare these two assets using the Mean Variance criterion. (b) Write the variance-covariance matrix, its inverse, and the expected vector return under the assumption of the correlation (a,b)=0.15. (c) Write the equation for the frontier portfolio optimal weights. (d) Find the optimal weights when the expected portfolio return p=0.015. (e) Find the portfolio with the global minimum varianceStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Cryptocurrency Complete Basics Guide For Beginners To Trading And Investing In Bitcoin Ethereum Altcoins Litecoin Ripple And Others

Authors: Rick Maverick

1st Edition

1985153068, 978-1985153066