Specific subject : Taxation MYS - ACCA

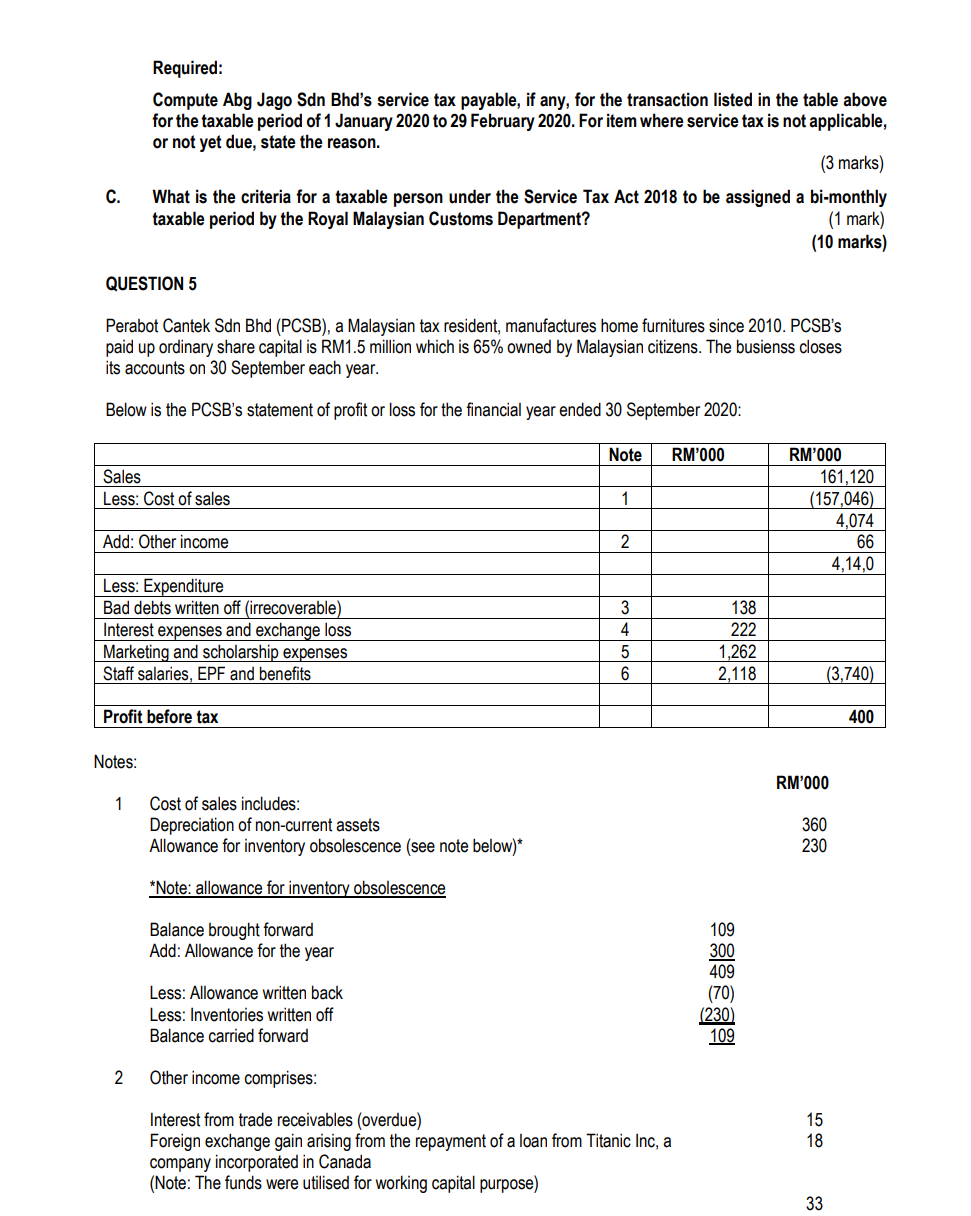

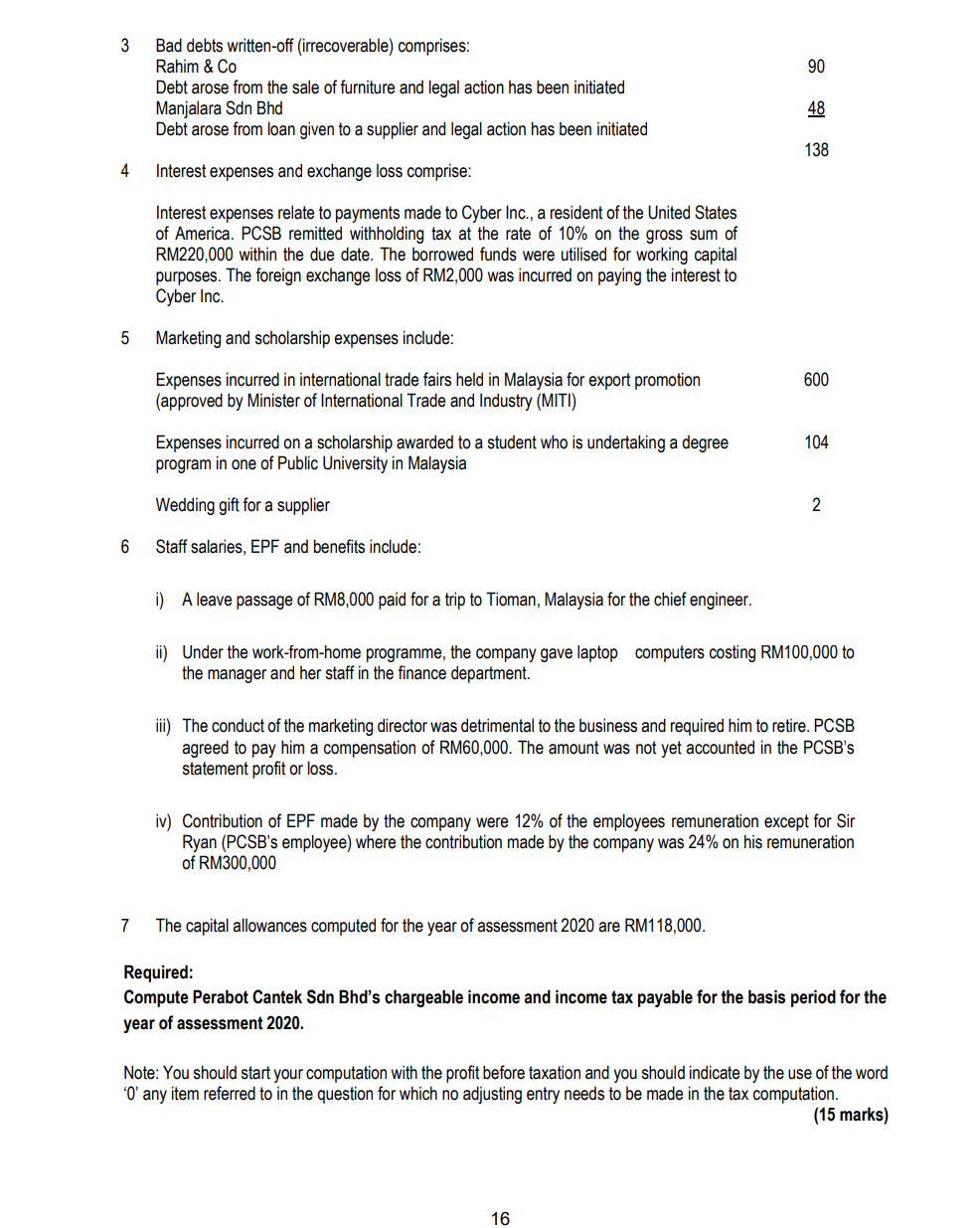

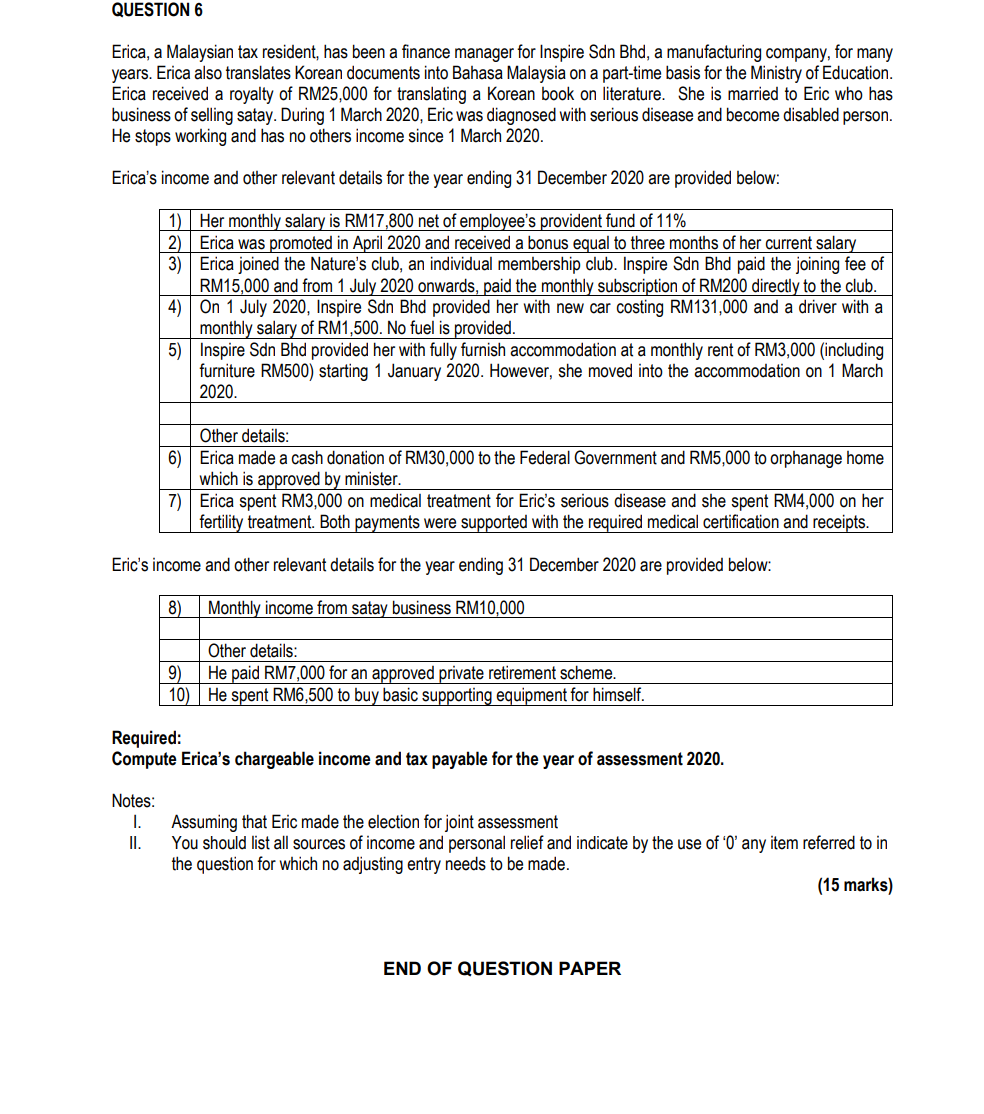

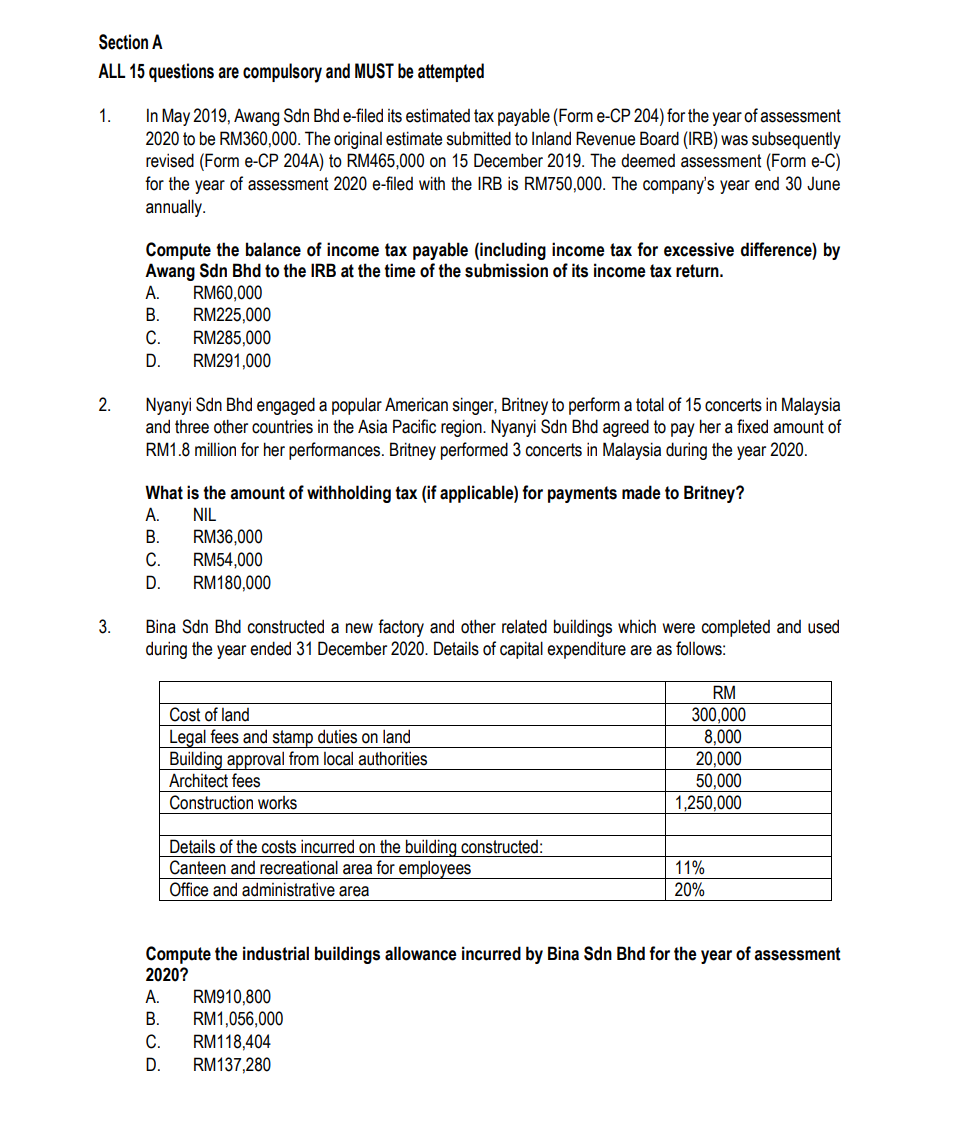

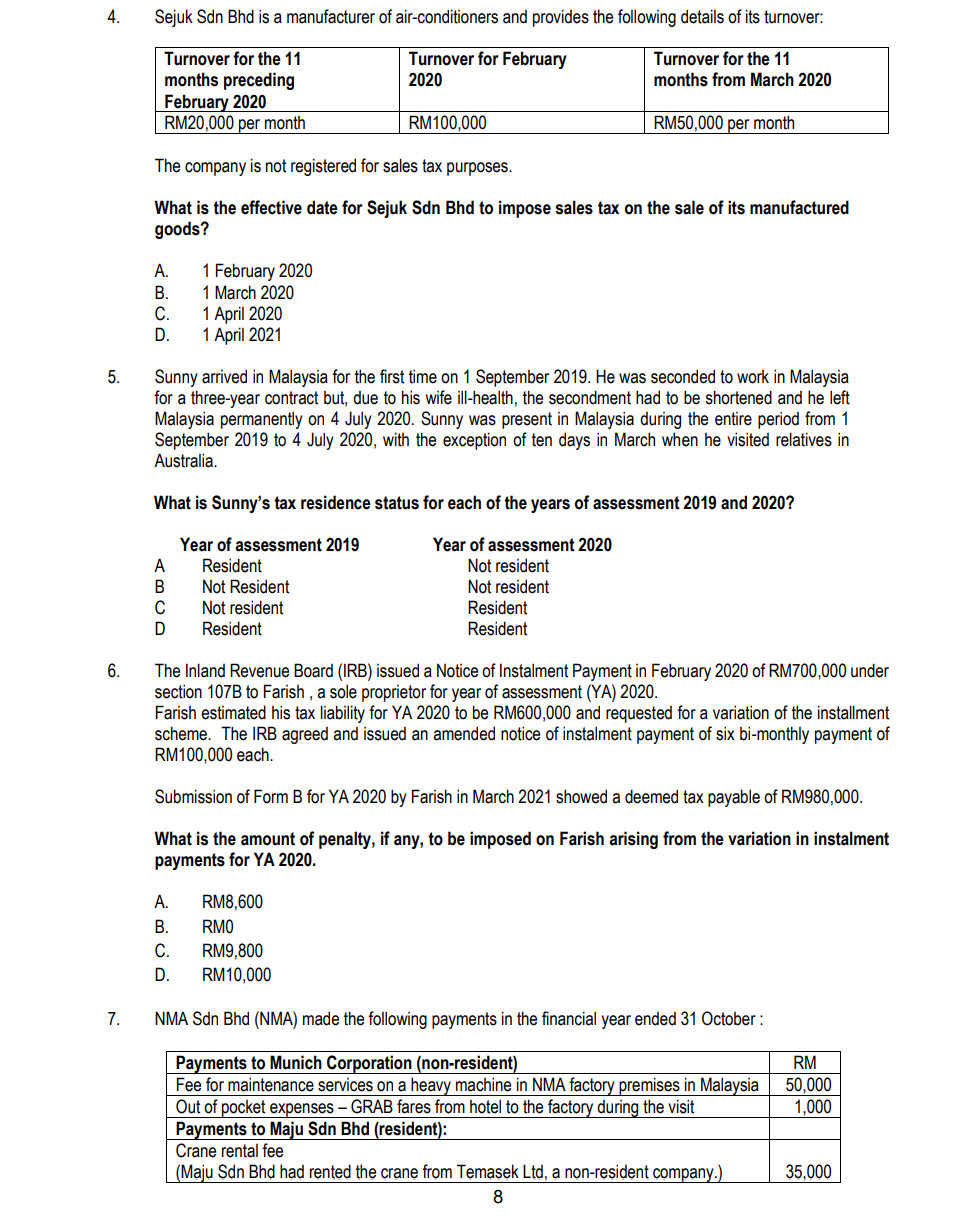

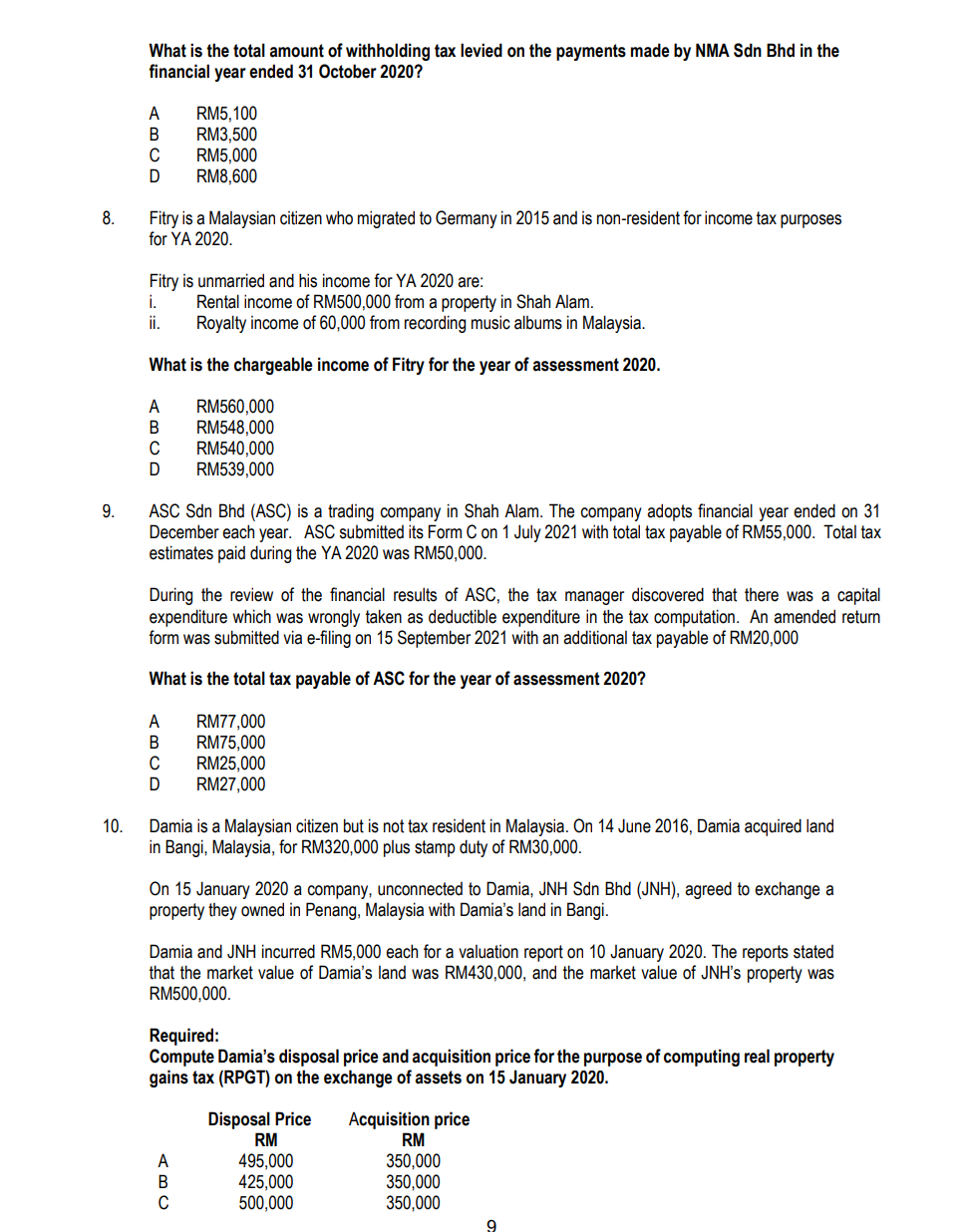

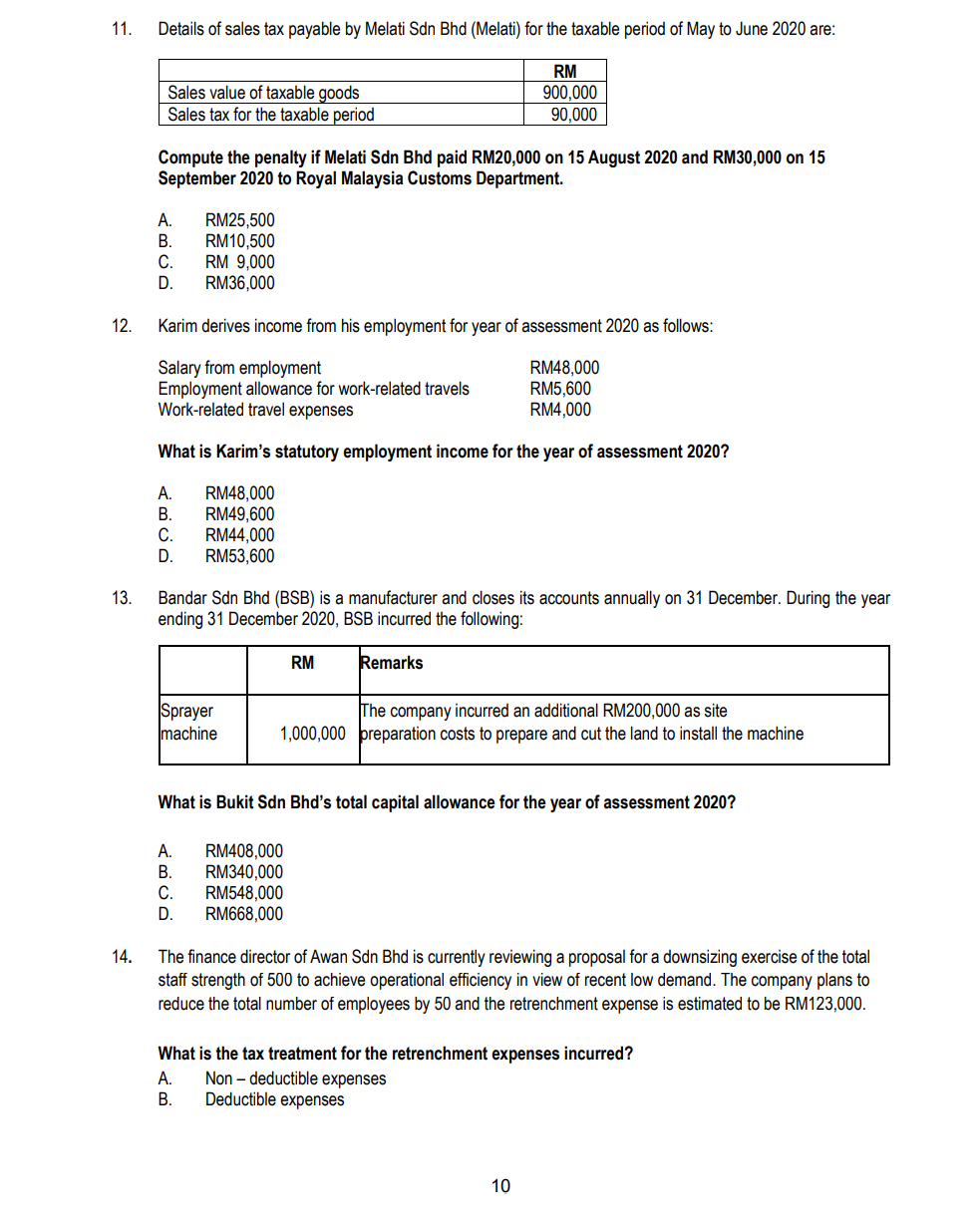

Section B - ALL SIX questions are compulsory and MUST be attempted QUESTION 1 (a) Star Sdn Bhd (SSB), a newly incorporated resident company involved in manufacturing, closes its account on 30 June every year. In the basis year 2020, SSB made the following payments to Jet Ltd (a non-resident company) RM800,000 for the purchase of a machine. RM270,000 for the installation of the machine at SSB's factory in Puchong. RM90,000 for the technical advice on the operation of the machine. The technical advice was provided onsite to all engineers of SSB on the day of installation. . Jet Ltd does not have any permanent establishment in Malaysia. On 25 January 2020, SSB paid the net amount after deducting withholding tax to Jet Ltd. However, SSB did not remit the withholding tax to the Inland Revenue Board of Malaysia (IRBM). Note: Ignore the provision of Double Taxation Agreement Required: (0) Compute the amount of withholding tax and penalty (if any) payable by Star Sdn Bhd to IRBM. (2 marks) (ii) Calculate the amount of withholding tax payable to RBM if Star Sdn Bhd does not deduct withholding tax from the payment made to Jet Ltd. (2 marks) (b) Paramount Sdn Bhd (PSB) is a Malaysian resident company which operates an internationally renowned fast-food chain. PSB has entered into a franchise agreement with Lala Ltd, a non-resident company. Under the terms of this agreement, PSB is required to pay a royalty annually based on its annual sales. For the year ended 30 September 2020, the gross royalty payable was computed as RM100,000 and this was paid to Lala Ltd on 20 October 2020. Required: (0) State the date by which the withholding tax on the royalty payment should have been remitted to the Inland Revenue Board (IRB). (1 mark) (ii) State the consequences for Paramount Sdn Bhd of its non-compliance with the withholding tax requirements. (3 marks) (iii) Compute the amount of withholding tax due and the penalty for its late payment (2 marks) Total: 10 marks QUESTION 2 Daisy Sdn Bhd, a manufacturing company, incurred the following expenses during the year ended 30 September 2020: Cost of land Stamp duty on the purchase of the land Legal charges on the Sale and Purchase Agreement RM 345,000 5,000 3,000 12 Cost of construction of the buildings: A factory A storage building* A canteen and restrooms Living quarters for factory workers Living quarters for administrative staff RM 300,000 54,000 36,000 90,000 120.000 600,000 Legal charges on the Contract Agreement for the construction of the buildings Architect fees regarding the buildings 10,000 20,000 The construction of all the buildings was completed in February 2020 and the buildings were put into use for the business from March 2020. The company also incurred RM75,000 on cutting and levelling the land to prepare a site for the installation of heavy machinery, costing RM800,000, purchased in January 2020. The machinery was put into use for the business from March 2020. * The storage building, which is used for the storage of the finished products, is adjacent to the factory. Required: Compute Daisy Sdn Bhd's allowances under Schedule 3 of the Income Tax Act for the year of assessment 2020, together with the residual expenditure carried forward. (10 marks) QUESTION 3 Harry, a Norway citizen had signed a sale and purchase agreement on 28 February 2016 to acquire a piece of land from Ameer for RM540,000. His plan was to construct a bungalow under Malaysia as a Second Home' program. Harry had secured a bank loan for the land acquisition and had to bear a total interest cost of RM28,000. On 1 May 2016, the land ownership was transferred to Harry and he incurred the following costs: Cost of legal fees Stamp duty RM 6,200 20,000 In July 2016, Harry spent RM35,000 for levelling, drainage and fencing the land. On 25 December 2016, he received RM700,000 as compensation from his neighbour when the land was badly damaged in a fire caused by his neighbour's open burning. In 2017, Harry constructed a small bungalow on the land for RM400,000. Harry decided to return to Norway and sold the bungalow to his good friend, Porter (a Philippine citizen) for RM1,800,000 on 1 October 2019. The legal fees and valuation fees for the disposal were RM12,000 and RM6,000 respectively. On 13 November 2020, Porter transferred the bungalow to his son, David on his wedding day when the market value of the property was RM2,000,000. Required: i. Compute the real property gains tax payable, if any, payable by Harry on the disposal. ii. Compute the real property gains tax payable, if any, payable by Porter, on the transfer of the property to David on 13 November 2020. 13 Note: You should indicate by the use of the word '0', where appropriate, any item referred to in the question for which no adjusting entry needs to be made in the tax computation. (10 marks) QUESTION 4 A. Calla Sdn Bhd is a manufacturer of furniture, registered under the Sales Tax Act 2018, and closes its accounts annually on 31 December. The sales tax rate applicable to furniture is 10%. Details of the transaction in the period from 1 January 2020 to 31 March 2020 are shown below: Date 25 January 2020 2 February 2020 Details of transactions RM (Value before any tax) Invoice for goods sold to PU Raj 200,000 Sdn Bhd. Payment was received on 10 March 2020. Made a gift of goods consisting of 19,000 (cost) the furniture it manufactures to the market value of the goods Rumah Harapan, an approved donated was RM20,000 charitable organisation. Invoice for goods sold to Little Bhd. 30,000 Payment terms in the contract allowed for a 90-days period and payment was received accordingly. 12 March 2020 Required: i) Compute the sales tax payable by Calla Sdn Bhd on the transaction listed in the table above for the taxable period of 1 January 2020 to 29 February 2020. Note: You should indicate by the use of 'O' any item referred to in the table for Calla Sdn Bhd on which no sales tax is due for the relevant taxable period. (3 marks) ii) State the due date to pay sales tax and penalty due, assuming the sales tax was paid on 2 May 2020. (3 marks) B. Abg Jago Sdn Bhd, a service tax registrant, is in the business providing telecommunication services and close its accounts annually on 31 December. Details of the transactions for the months of January 2020 and February 2020 and other relevant information are shown below: Date invoiced was issued 25 January 2020 Date payment received 14 February 2020 30 December 2019 Details Invoice for telecommunication services to a customer, ABC Enterprise, for RM150,000 Received payment of RM50,000 for an invoice issued to a customer, Lily Sdn Bhd Invoice for telecommunication services to a customer, Amar Sdn Bhd, for RM100,000 5 January 2020 25 February 2020 2 March 2020 Required: Compute Abg Jago Sdn Bhd's service tax payable, if any, for the transaction listed in the table above for the taxable period of 1 January 2020 to 29 February 2020. For item where service tax is not applicable, or not yet due, state the reason. (3 marks) What is the criteria for a taxable person under the Service Tax Act 2018 to be assigned a bi-monthly taxable period by the Royal Malaysian Customs Department? (1 mark) (10 marks) C. QUESTION 5 Perabot Cantek Sdn Bhd (PCSB), a Malaysian tax resident, manufactures home furnitures since 2010. PCSB's paid up ordinary share capital is RM1.5 million which is 65% owned by Malaysian citizens. The busienss closes its accounts on 30 September each year. Below is the PCSB's statement of profit or loss for the financial year ended 30 September 2020: Note RM'000 Sales Less: Cost of sales 1 RM'000 161,120 (157,046) 4,074 66 4,14,0 Add: Other income 2 Less: Expenditure Bad debts written off (irrecoverable) Interest expenses and exchange loss Marketing and scholarship expenses Staff salaries, EPF and benefits 3 4 5 6 138 222 1,262 2,118 (3,740) Profit before tax 400 Notes: RM'000 1 Cost of sales includes: Depreciation of non-current assets Allowance for inventory obsolescence (see note below)* 360 230 *Note: allowance for inventory obsolescence Balance brought forward Add: Allowance for the year Less: Allowance written back Less: Inventories written off Balance carried forward 109 300 409 (70) (230) 109 2 Other income comprises: 15 18 Interest from trade receivables (overdue) Foreign exchange gain arising from the repayment of a loan from Titanic Inc, a company incorporated in Canada (Note: The funds were utilised for working capital purpose) 33 3 90 Bad debts written-off (irrecoverable) comprises: Rahim & Co Debt arose from the sale of furniture and legal action has been initiated Manjalara Sdn Bhd Debt arose from loan given to a supplier and legal action has been initiated 48 138 4 Interest expenses and exchange loss comprise: Interest expenses relate to payments made to Cyber Inc., a resident of the United States of America. PCSB remitted withholding tax at the rate of 10% on the gross sum of RM220,000 within the due date. The borrowed funds were utilised for working capital purposes. The foreign exchange loss of RM2,000 was incurred on paying the interest to Cyber Inc. 5 Marketing and scholarship expenses include: 600 Expenses incurred in international trade fairs held in Malaysia for export promotion (approved by Minister of International Trade and Industry (MITI) 104 Expenses incurred on a scholarship awarded to a student who is undertaking a degree program in one of Public University in Malaysia Wedding gift for a supplier 2 6 Staff salaries, EPF and benefits include: i) A leave passage of RM8,000 paid for a trip to Tioman, Malaysia for the chief engineer. ii) Under the work-from-home programme, the company gave laptop computers costing RM100,000 to the manager and her staff in the finance department. iii) The conduct of the marketing director was detrimental to the business and required him to retire. PCSB agreed to pay him a compensation of RM60,000. The amount was not yet accounted in the PCSB's statement profit or loss. iv) Contribution of EPF made by the company were 12% of the employees remuneration except for Sir Ryan (PCSB's employee) where the contribution made by the company was 24% on his remuneration of RM300,000 7 The capital allowances computed for the year of assessment 2020 are RM118,000. Required: Compute Perabot Cantek Sdn Bhd's chargeable income and income tax payable for the basis period for the year of assessment 2020. Note: You should start your computation with the profit before taxation and you should indicate by the use of the word 'O' any item referred to in the question for which no adjusting entry needs to be made in the tax computation. (15 marks) 16 QUESTION 6 Erica, a Malaysian tax resident, has been a finance manager for Inspire Sdn Bhd, a manufacturing company, for many years. Erica also translates Korean documents into Bahasa Malaysia on a part-time basis for the Ministry of Education. Erica received a royalty of RM25,000 for translating a Korean book on literature. She is married to Eric who has business of selling satay. During 1 March 2020, Eric was diagnosed with serious disease and become disabled person. He stops working and has no others income since 1 March 2020. Erica's income and other relevant details for the year ending 31 December 2020 are provided below: 1) Her monthly salary is RM17,800 net of employee's provident fund of 11% 2) Erica was promoted in April 2020 and received a bonus equal to three months of her current salary 3) Erica joined the Nature's club, an individual membership club. Inspire Sdn Bhd paid the joining fee of RM15,000 and from 1 July 2020 onwards, paid the monthly subscription of RM200 directly to the club. 4) On 1 July 2020, Inspire Sdn Bhd provided her with new car costing RM131,000 and a driver with a monthly salary of RM1,500. No fuel is provided. 5) Inspire Sdn Bhd provided her with fully furnish accommodation at a monthly rent of RM3,000 (including furniture RM500) starting 1 January 2020. However, she moved into the accommodation on 1 March 2020 Other details: 6) Erica made a cash donation of RM30,000 to the Federal Government and RM5,000 to orphanage home which is approved by minister 7) Erica spent RM3,000 on medical treatment for Eric's serious disease and she spent RM4,000 on her fertility treatment. Both payments were supported with the required medical certification and receipts. Eric's income and other relevant details for the year ending 31 December 2020 are provided below: 8) Monthly income from satay business RM10,000 Other details: 9) He paid RM7,000 for an approved private retirement scheme. 10) He spent RM6,500 to buy basic supporting equipment for himself. Required: Compute Erica's chargeable income and tax payable for the year of assessment 2020. Notes: 1. II. Assuming that Eric made the election for joint assessment You should list all sources of income and personal relief and indicate by the use of 'O' any item referred to in the question for which no adjusting entry needs to be made. (15 marks) END OF QUESTION PAPER Section A ALL 15 questions are compulsory and MUST be attempted 1. In May 2019, Awang Sdn Bhd e-filed its estimated tax payable (Form e-CP 204) for the year of assessment 2020 to be RM360,000. The original estimate submitted to Inland Revenue Board (IRB) was subsequently revised (Form e-CP 204A) to RM465,000 on 15 December 2019. The deemed assessment (Form e-C) for the year of assessment 2020 e-filed with the IRB is RM750,000. The company's year end 30 June annually. Compute the balance of income tax payable (including income tax for excessive difference) by Awang Sdn Bhd to the IRB at the time of the submission of its income tax return. A. RM60,000 B. RM225,000 C. RM285,000 D. RM291,000 2. Nyanyi Sdn Bhd engaged a popular American singer, Britney to perform a total of 15 concerts in Malaysia and three other countries in the Asia Pacific region. Nyanyi Sdn Bhd agreed to pay her a fixed amount of RM1.8 million for her performances. Britney performed 3 concerts in Malaysia during the year 2020. What is the amount of withholding tax (if applicable) for payments made to Britney? A. NIL B. RM36,000 C. RM54,000 D. RM180,000 3. Bina Sdn Bhd constructed a new factory and other related buildings which were completed and used during the year ended 31 December 2020. Details of capital expenditure are as follows: Cost of land Legal fees and stamp duties on land Building approval from local authorities Architect fees Construction works RM 300,000 8,000 20,000 50,000 1,250,000 Details of the costs incurred on the building constructed: Canteen and recreational area for employees Office and administrative area 11% 20% Compute the industrial buildings allowance incurred by Bina Sdn Bhd for the year of assessment 2020? A. RM910,800 B. RM1,056,000 C. RM118,404 D. RM137,280 4. Sejuk Sdn Bhd is a manufacturer of air-conditioners and provides the following details of its turnover: Turnover for February 2020 Turnover for the 11 months from March 2020 Turnover for the 11 months preceding February 2020 RM20,000 per month RM100,000 RM50,000 per month The company is not registered for sales tax purposes. What is the effective date for Sejuk Sdn Bhd to impose sales tax on the sale of its manufactured goods? A. B. C. D. 1 February 2020 1 March 2020 1 April 2020 1 April 2021 5. Sunny arrived in Malaysia for the first time on 1 September 2019. He was seconded to work in Malaysia for a three-year contract but, due to his wife ill-health, the secondment had to be shortened and he left Malaysia permanently on 4 July 2020. Sunny was present in Malaysia during the entire period from 1 September 2019 to 4 July 2020, with the exception of ten days in March when he visited relatives in Australia. What is Sunny's tax residence status for each of the years of assessment 2019 and 2020? A B D Year of assessment 2019 Resident Not Resident Not resident Resident Year of assessment 2020 Not resident Not resident Resident Resident 6. The Inland Revenue Board (IRB) issued a Notice of Instalment Payment in February 2020 of RM700,000 under section 107B to Farish, a sole proprietor for year of assessment (YA) 2020. Farish estimated his tax liability for YA 2020 to be RM600,000 and requested for a variation of the installment scheme. The IRB agreed and issued an amended notice of instalment payment of six bi-monthly payment of RM100,000 each. Submission of Form B for YA 2020 by Farish in March 2021 showed a deemed tax payable of RM980,000. What is the amount of penalty, if any, to be imposed on Farish arising from the variation in instalment payments for YA 2020. A. B. C. D. RM8,600 RMO RM9,800 RM10,000 7. NMA Sdn Bhd (NMA) made the following payments in the financial year ended 31 October : RM 50,000 1,000 Payments to Munich Corporation (non-resident) Fee for maintenance services on a heavy machine in NMA factory premises in Malaysia Out of pocket expenses - GRAB fares from hotel to the factory during the visit Payments to Maju Sdn Bhd (resident): Crane rental fee (Maju Sdn Bhd had rented the crane from Temasek Ltd, a non-resident company.) 8 35,000 What is the total amount of withholding tax levied on the payments made by NMA Sdn Bhd in the financial year ended 31 October 2020? A B D RM5,100 RM3,500 RM5,000 RM8,600 8. Fitry is a Malaysian citizen who migrated to Germany in 2015 and is non-resident for income tax purposes for YA 2020. Fitry is unmarried and his income for YA 2020 are: i. Rental income of RM500,000 from a property in Shah Alam. ii. Royalty income of 60,000 from recording music albums in Malaysia. What is the chargeable income of Fitry for the year of assessment 2020. A B D RM560,000 RM548,000 RM540,000 RM539,000 9. ASC Sdn Bhd (ASC) is a trading company in Shah Alam. The company adopts financial year ended on 31 December each year. ASC submitted its Form C on 1 July 2021 with total tax payable of RM55,000. Total tax estimates paid during the YA 2020 was RM50,000. During the review of the financial results of ASC, the tax manager discovered that there was a capital expenditure which was wrongly taken as deductible expenditure in the tax computation. An amended return form was submitted via e-filing on 15 September 2021 with an additional tax payable of RM20,000 What is the total tax payable of ASC for the year of assessment 2020? A B D RM77,000 RM75,000 RM25,000 RM27,000 10. Damia is a Malaysian citizen but is not tax resident in Malaysia. On 14 June 2016, Damia acquired land in Bangi, Malaysia, for RM320,000 plus stamp duty of RM30,000. On 15 January 2020 a company, unconnected to Damia, JNH Sdn Bhd (JNH), agreed to exchange a property they owned in Penang, Malaysia with Damia's land in Bangi. Damia and JNH incurred RM5,000 each for a valuation report on 10 January 2020. The reports stated that the market value of Damia's land was RM430,000, and the market value of JNH's property was RM500,000. Required: Compute Damia's disposal price and acquisition price for the purpose of computing real property gains tax (RPGT) on the exchange of assets on 15 January 2020. A B Disposal Price RM 495,000 425,000 500,000 Acquisition price RM 350,000 350,000 350,000 9 11. Details of sales tax payable by Melati Sdn Bhd (Melati) for the taxable period of May to June 2020 are: Sales value of taxable goods Sales tax for the taxable period RM 900,000 90,000 Compute the penalty if Melati Sdn Bhd paid RM20,000 on 15 August 2020 and RM30,000 on 15 September 2020 to Royal Malaysia Customs Department. A. B. C. D. RM25,500 RM10,500 RM 9,000 RM36,000 12. Karim derives income from his employment for year of assessment 2020 as follows: Salary from employment Employment allowance for work-related travels Work-related travel expenses RM48,000 RM5,600 RM4,000 What is Karim's statutory employment income for the year of assessment 2020? A. B. C. D RM48,000 RM49,600 RM44,000 RM53,600 13. Bandar Sdn Bhd (BSB) is a manufacturer and closes its accounts annually on 31 December. During the year ending 31 December 2020, BSB incurred the following: RM Remarks Sprayer machine The company incurred an additional RM200,000 as site 1,000,000 preparation costs to prepare and cut the land to install the machine What is Bukit Sdn Bhd's total capital allowance for the year of assessment 2020? A. B. C. D. RM408,000 RM340,000 RM548,000 RM668,000 14. The finance director of Awan Sdn Bhd is currently reviewing a proposal for a downsizing exercise of the total staff strength of 500 to achieve operational efficiency in view of recent low demand. The company plans to reduce the total number of employees by 50 and the retrenchment expense is estimated to be RM123,000. What is the tax treatment for the retrenchment expenses incurred? A. Non-deductible expenses B. Deductible expenses 10 Section B - ALL SIX questions are compulsory and MUST be attempted QUESTION 1 (a) Star Sdn Bhd (SSB), a newly incorporated resident company involved in manufacturing, closes its account on 30 June every year. In the basis year 2020, SSB made the following payments to Jet Ltd (a non-resident company) RM800,000 for the purchase of a machine. RM270,000 for the installation of the machine at SSB's factory in Puchong. RM90,000 for the technical advice on the operation of the machine. The technical advice was provided onsite to all engineers of SSB on the day of installation. . Jet Ltd does not have any permanent establishment in Malaysia. On 25 January 2020, SSB paid the net amount after deducting withholding tax to Jet Ltd. However, SSB did not remit the withholding tax to the Inland Revenue Board of Malaysia (IRBM). Note: Ignore the provision of Double Taxation Agreement Required: (0) Compute the amount of withholding tax and penalty (if any) payable by Star Sdn Bhd to IRBM. (2 marks) (ii) Calculate the amount of withholding tax payable to RBM if Star Sdn Bhd does not deduct withholding tax from the payment made to Jet Ltd. (2 marks) (b) Paramount Sdn Bhd (PSB) is a Malaysian resident company which operates an internationally renowned fast-food chain. PSB has entered into a franchise agreement with Lala Ltd, a non-resident company. Under the terms of this agreement, PSB is required to pay a royalty annually based on its annual sales. For the year ended 30 September 2020, the gross royalty payable was computed as RM100,000 and this was paid to Lala Ltd on 20 October 2020. Required: (0) State the date by which the withholding tax on the royalty payment should have been remitted to the Inland Revenue Board (IRB). (1 mark) (ii) State the consequences for Paramount Sdn Bhd of its non-compliance with the withholding tax requirements. (3 marks) (iii) Compute the amount of withholding tax due and the penalty for its late payment (2 marks) Total: 10 marks QUESTION 2 Daisy Sdn Bhd, a manufacturing company, incurred the following expenses during the year ended 30 September 2020: Cost of land Stamp duty on the purchase of the land Legal charges on the Sale and Purchase Agreement RM 345,000 5,000 3,000 12 Cost of construction of the buildings: A factory A storage building* A canteen and restrooms Living quarters for factory workers Living quarters for administrative staff RM 300,000 54,000 36,000 90,000 120.000 600,000 Legal charges on the Contract Agreement for the construction of the buildings Architect fees regarding the buildings 10,000 20,000 The construction of all the buildings was completed in February 2020 and the buildings were put into use for the business from March 2020. The company also incurred RM75,000 on cutting and levelling the land to prepare a site for the installation of heavy machinery, costing RM800,000, purchased in January 2020. The machinery was put into use for the business from March 2020. * The storage building, which is used for the storage of the finished products, is adjacent to the factory. Required: Compute Daisy Sdn Bhd's allowances under Schedule 3 of the Income Tax Act for the year of assessment 2020, together with the residual expenditure carried forward. (10 marks) QUESTION 3 Harry, a Norway citizen had signed a sale and purchase agreement on 28 February 2016 to acquire a piece of land from Ameer for RM540,000. His plan was to construct a bungalow under Malaysia as a Second Home' program. Harry had secured a bank loan for the land acquisition and had to bear a total interest cost of RM28,000. On 1 May 2016, the land ownership was transferred to Harry and he incurred the following costs: Cost of legal fees Stamp duty RM 6,200 20,000 In July 2016, Harry spent RM35,000 for levelling, drainage and fencing the land. On 25 December 2016, he received RM700,000 as compensation from his neighbour when the land was badly damaged in a fire caused by his neighbour's open burning. In 2017, Harry constructed a small bungalow on the land for RM400,000. Harry decided to return to Norway and sold the bungalow to his good friend, Porter (a Philippine citizen) for RM1,800,000 on 1 October 2019. The legal fees and valuation fees for the disposal were RM12,000 and RM6,000 respectively. On 13 November 2020, Porter transferred the bungalow to his son, David on his wedding day when the market value of the property was RM2,000,000. Required: i. Compute the real property gains tax payable, if any, payable by Harry on the disposal. ii. Compute the real property gains tax payable, if any, payable by Porter, on the transfer of the property to David on 13 November 2020. 13 Note: You should indicate by the use of the word '0', where appropriate, any item referred to in the question for which no adjusting entry needs to be made in the tax computation. (10 marks) QUESTION 4 A. Calla Sdn Bhd is a manufacturer of furniture, registered under the Sales Tax Act 2018, and closes its accounts annually on 31 December. The sales tax rate applicable to furniture is 10%. Details of the transaction in the period from 1 January 2020 to 31 March 2020 are shown below: Date 25 January 2020 2 February 2020 Details of transactions RM (Value before any tax) Invoice for goods sold to PU Raj 200,000 Sdn Bhd. Payment was received on 10 March 2020. Made a gift of goods consisting of 19,000 (cost) the furniture it manufactures to the market value of the goods Rumah Harapan, an approved donated was RM20,000 charitable organisation. Invoice for goods sold to Little Bhd. 30,000 Payment terms in the contract allowed for a 90-days period and payment was received accordingly. 12 March 2020 Required: i) Compute the sales tax payable by Calla Sdn Bhd on the transaction listed in the table above for the taxable period of 1 January 2020 to 29 February 2020. Note: You should indicate by the use of 'O' any item referred to in the table for Calla Sdn Bhd on which no sales tax is due for the relevant taxable period. (3 marks) ii) State the due date to pay sales tax and penalty due, assuming the sales tax was paid on 2 May 2020. (3 marks) B. Abg Jago Sdn Bhd, a service tax registrant, is in the business providing telecommunication services and close its accounts annually on 31 December. Details of the transactions for the months of January 2020 and February 2020 and other relevant information are shown below: Date invoiced was issued 25 January 2020 Date payment received 14 February 2020 30 December 2019 Details Invoice for telecommunication services to a customer, ABC Enterprise, for RM150,000 Received payment of RM50,000 for an invoice issued to a customer, Lily Sdn Bhd Invoice for telecommunication services to a customer, Amar Sdn Bhd, for RM100,000 5 January 2020 25 February 2020 2 March 2020 Required: Compute Abg Jago Sdn Bhd's service tax payable, if any, for the transaction listed in the table above for the taxable period of 1 January 2020 to 29 February 2020. For item where service tax is not applicable, or not yet due, state the reason. (3 marks) What is the criteria for a taxable person under the Service Tax Act 2018 to be assigned a bi-monthly taxable period by the Royal Malaysian Customs Department? (1 mark) (10 marks) C. QUESTION 5 Perabot Cantek Sdn Bhd (PCSB), a Malaysian tax resident, manufactures home furnitures since 2010. PCSB's paid up ordinary share capital is RM1.5 million which is 65% owned by Malaysian citizens. The busienss closes its accounts on 30 September each year. Below is the PCSB's statement of profit or loss for the financial year ended 30 September 2020: Note RM'000 Sales Less: Cost of sales 1 RM'000 161,120 (157,046) 4,074 66 4,14,0 Add: Other income 2 Less: Expenditure Bad debts written off (irrecoverable) Interest expenses and exchange loss Marketing and scholarship expenses Staff salaries, EPF and benefits 3 4 5 6 138 222 1,262 2,118 (3,740) Profit before tax 400 Notes: RM'000 1 Cost of sales includes: Depreciation of non-current assets Allowance for inventory obsolescence (see note below)* 360 230 *Note: allowance for inventory obsolescence Balance brought forward Add: Allowance for the year Less: Allowance written back Less: Inventories written off Balance carried forward 109 300 409 (70) (230) 109 2 Other income comprises: 15 18 Interest from trade receivables (overdue) Foreign exchange gain arising from the repayment of a loan from Titanic Inc, a company incorporated in Canada (Note: The funds were utilised for working capital purpose) 33 3 90 Bad debts written-off (irrecoverable) comprises: Rahim & Co Debt arose from the sale of furniture and legal action has been initiated Manjalara Sdn Bhd Debt arose from loan given to a supplier and legal action has been initiated 48 138 4 Interest expenses and exchange loss comprise: Interest expenses relate to payments made to Cyber Inc., a resident of the United States of America. PCSB remitted withholding tax at the rate of 10% on the gross sum of RM220,000 within the due date. The borrowed funds were utilised for working capital purposes. The foreign exchange loss of RM2,000 was incurred on paying the interest to Cyber Inc. 5 Marketing and scholarship expenses include: 600 Expenses incurred in international trade fairs held in Malaysia for export promotion (approved by Minister of International Trade and Industry (MITI) 104 Expenses incurred on a scholarship awarded to a student who is undertaking a degree program in one of Public University in Malaysia Wedding gift for a supplier 2 6 Staff salaries, EPF and benefits include: i) A leave passage of RM8,000 paid for a trip to Tioman, Malaysia for the chief engineer. ii) Under the work-from-home programme, the company gave laptop computers costing RM100,000 to the manager and her staff in the finance department. iii) The conduct of the marketing director was detrimental to the business and required him to retire. PCSB agreed to pay him a compensation of RM60,000. The amount was not yet accounted in the PCSB's statement profit or loss. iv) Contribution of EPF made by the company were 12% of the employees remuneration except for Sir Ryan (PCSB's employee) where the contribution made by the company was 24% on his remuneration of RM300,000 7 The capital allowances computed for the year of assessment 2020 are RM118,000. Required: Compute Perabot Cantek Sdn Bhd's chargeable income and income tax payable for the basis period for the year of assessment 2020. Note: You should start your computation with the profit before taxation and you should indicate by the use of the word 'O' any item referred to in the question for which no adjusting entry needs to be made in the tax computation. (15 marks) 16 QUESTION 6 Erica, a Malaysian tax resident, has been a finance manager for Inspire Sdn Bhd, a manufacturing company, for many years. Erica also translates Korean documents into Bahasa Malaysia on a part-time basis for the Ministry of Education. Erica received a royalty of RM25,000 for translating a Korean book on literature. She is married to Eric who has business of selling satay. During 1 March 2020, Eric was diagnosed with serious disease and become disabled person. He stops working and has no others income since 1 March 2020. Erica's income and other relevant details for the year ending 31 December 2020 are provided below: 1) Her monthly salary is RM17,800 net of employee's provident fund of 11% 2) Erica was promoted in April 2020 and received a bonus equal to three months of her current salary 3) Erica joined the Nature's club, an individual membership club. Inspire Sdn Bhd paid the joining fee of RM15,000 and from 1 July 2020 onwards, paid the monthly subscription of RM200 directly to the club. 4) On 1 July 2020, Inspire Sdn Bhd provided her with new car costing RM131,000 and a driver with a monthly salary of RM1,500. No fuel is provided. 5) Inspire Sdn Bhd provided her with fully furnish accommodation at a monthly rent of RM3,000 (including furniture RM500) starting 1 January 2020. However, she moved into the accommodation on 1 March 2020 Other details: 6) Erica made a cash donation of RM30,000 to the Federal Government and RM5,000 to orphanage home which is approved by minister 7) Erica spent RM3,000 on medical treatment for Eric's serious disease and she spent RM4,000 on her fertility treatment. Both payments were supported with the required medical certification and receipts. Eric's income and other relevant details for the year ending 31 December 2020 are provided below: 8) Monthly income from satay business RM10,000 Other details: 9) He paid RM7,000 for an approved private retirement scheme. 10) He spent RM6,500 to buy basic supporting equipment for himself. Required: Compute Erica's chargeable income and tax payable for the year of assessment 2020. Notes: 1. II. Assuming that Eric made the election for joint assessment You should list all sources of income and personal relief and indicate by the use of 'O' any item referred to in the question for which no adjusting entry needs to be made. (15 marks) END OF QUESTION PAPER Section A ALL 15 questions are compulsory and MUST be attempted 1. In May 2019, Awang Sdn Bhd e-filed its estimated tax payable (Form e-CP 204) for the year of assessment 2020 to be RM360,000. The original estimate submitted to Inland Revenue Board (IRB) was subsequently revised (Form e-CP 204A) to RM465,000 on 15 December 2019. The deemed assessment (Form e-C) for the year of assessment 2020 e-filed with the IRB is RM750,000. The company's year end 30 June annually. Compute the balance of income tax payable (including income tax for excessive difference) by Awang Sdn Bhd to the IRB at the time of the submission of its income tax return. A. RM60,000 B. RM225,000 C. RM285,000 D. RM291,000 2. Nyanyi Sdn Bhd engaged a popular American singer, Britney to perform a total of 15 concerts in Malaysia and three other countries in the Asia Pacific region. Nyanyi Sdn Bhd agreed to pay her a fixed amount of RM1.8 million for her performances. Britney performed 3 concerts in Malaysia during the year 2020. What is the amount of withholding tax (if applicable) for payments made to Britney? A. NIL B. RM36,000 C. RM54,000 D. RM180,000 3. Bina Sdn Bhd constructed a new factory and other related buildings which were completed and used during the year ended 31 December 2020. Details of capital expenditure are as follows: Cost of land Legal fees and stamp duties on land Building approval from local authorities Architect fees Construction works RM 300,000 8,000 20,000 50,000 1,250,000 Details of the costs incurred on the building constructed: Canteen and recreational area for employees Office and administrative area 11% 20% Compute the industrial buildings allowance incurred by Bina Sdn Bhd for the year of assessment 2020? A. RM910,800 B. RM1,056,000 C. RM118,404 D. RM137,280 4. Sejuk Sdn Bhd is a manufacturer of air-conditioners and provides the following details of its turnover: Turnover for February 2020 Turnover for the 11 months from March 2020 Turnover for the 11 months preceding February 2020 RM20,000 per month RM100,000 RM50,000 per month The company is not registered for sales tax purposes. What is the effective date for Sejuk Sdn Bhd to impose sales tax on the sale of its manufactured goods? A. B. C. D. 1 February 2020 1 March 2020 1 April 2020 1 April 2021 5. Sunny arrived in Malaysia for the first time on 1 September 2019. He was seconded to work in Malaysia for a three-year contract but, due to his wife ill-health, the secondment had to be shortened and he left Malaysia permanently on 4 July 2020. Sunny was present in Malaysia during the entire period from 1 September 2019 to 4 July 2020, with the exception of ten days in March when he visited relatives in Australia. What is Sunny's tax residence status for each of the years of assessment 2019 and 2020? A B D Year of assessment 2019 Resident Not Resident Not resident Resident Year of assessment 2020 Not resident Not resident Resident Resident 6. The Inland Revenue Board (IRB) issued a Notice of Instalment Payment in February 2020 of RM700,000 under section 107B to Farish, a sole proprietor for year of assessment (YA) 2020. Farish estimated his tax liability for YA 2020 to be RM600,000 and requested for a variation of the installment scheme. The IRB agreed and issued an amended notice of instalment payment of six bi-monthly payment of RM100,000 each. Submission of Form B for YA 2020 by Farish in March 2021 showed a deemed tax payable of RM980,000. What is the amount of penalty, if any, to be imposed on Farish arising from the variation in instalment payments for YA 2020. A. B. C. D. RM8,600 RMO RM9,800 RM10,000 7. NMA Sdn Bhd (NMA) made the following payments in the financial year ended 31 October : RM 50,000 1,000 Payments to Munich Corporation (non-resident) Fee for maintenance services on a heavy machine in NMA factory premises in Malaysia Out of pocket expenses - GRAB fares from hotel to the factory during the visit Payments to Maju Sdn Bhd (resident): Crane rental fee (Maju Sdn Bhd had rented the crane from Temasek Ltd, a non-resident company.) 8 35,000 What is the total amount of withholding tax levied on the payments made by NMA Sdn Bhd in the financial year ended 31 October 2020? A B D RM5,100 RM3,500 RM5,000 RM8,600 8. Fitry is a Malaysian citizen who migrated to Germany in 2015 and is non-resident for income tax purposes for YA 2020. Fitry is unmarried and his income for YA 2020 are: i. Rental income of RM500,000 from a property in Shah Alam. ii. Royalty income of 60,000 from recording music albums in Malaysia. What is the chargeable income of Fitry for the year of assessment 2020. A B D RM560,000 RM548,000 RM540,000 RM539,000 9. ASC Sdn Bhd (ASC) is a trading company in Shah Alam. The company adopts financial year ended on 31 December each year. ASC submitted its Form C on 1 July 2021 with total tax payable of RM55,000. Total tax estimates paid during the YA 2020 was RM50,000. During the review of the financial results of ASC, the tax manager discovered that there was a capital expenditure which was wrongly taken as deductible expenditure in the tax computation. An amended return form was submitted via e-filing on 15 September 2021 with an additional tax payable of RM20,000 What is the total tax payable of ASC for the year of assessment 2020? A B D RM77,000 RM75,000 RM25,000 RM27,000 10. Damia is a Malaysian citizen but is not tax resident in Malaysia. On 14 June 2016, Damia acquired land in Bangi, Malaysia, for RM320,000 plus stamp duty of RM30,000. On 15 January 2020 a company, unconnected to Damia, JNH Sdn Bhd (JNH), agreed to exchange a property they owned in Penang, Malaysia with Damia's land in Bangi. Damia and JNH incurred RM5,000 each for a valuation report on 10 January 2020. The reports stated that the market value of Damia's land was RM430,000, and the market value of JNH's property was RM500,000. Required: Compute Damia's disposal price and acquisition price for the purpose of computing real property gains tax (RPGT) on the exchange of assets on 15 January 2020. A B Disposal Price RM 495,000 425,000 500,000 Acquisition price RM 350,000 350,000 350,000 9 11. Details of sales tax payable by Melati Sdn Bhd (Melati) for the taxable period of May to June 2020 are: Sales value of taxable goods Sales tax for the taxable period RM 900,000 90,000 Compute the penalty if Melati Sdn Bhd paid RM20,000 on 15 August 2020 and RM30,000 on 15 September 2020 to Royal Malaysia Customs Department. A. B. C. D. RM25,500 RM10,500 RM 9,000 RM36,000 12. Karim derives income from his employment for year of assessment 2020 as follows: Salary from employment Employment allowance for work-related travels Work-related travel expenses RM48,000 RM5,600 RM4,000 What is Karim's statutory employment income for the year of assessment 2020? A. B. C. D RM48,000 RM49,600 RM44,000 RM53,600 13. Bandar Sdn Bhd (BSB) is a manufacturer and closes its accounts annually on 31 December. During the year ending 31 December 2020, BSB incurred the following: RM Remarks Sprayer machine The company incurred an additional RM200,000 as site 1,000,000 preparation costs to prepare and cut the land to install the machine What is Bukit Sdn Bhd's total capital allowance for the year of assessment 2020? A. B. C. D. RM408,000 RM340,000 RM548,000 RM668,000 14. The finance director of Awan Sdn Bhd is currently reviewing a proposal for a downsizing exercise of the total staff strength of 500 to achieve operational efficiency in view of recent low demand. The company plans to reduce the total number of employees by 50 and the retrenchment expense is estimated to be RM123,000. What is the tax treatment for the retrenchment expenses incurred? A. Non-deductible expenses B. Deductible expenses 10