Answered step by step

Verified Expert Solution

Question

1 Approved Answer

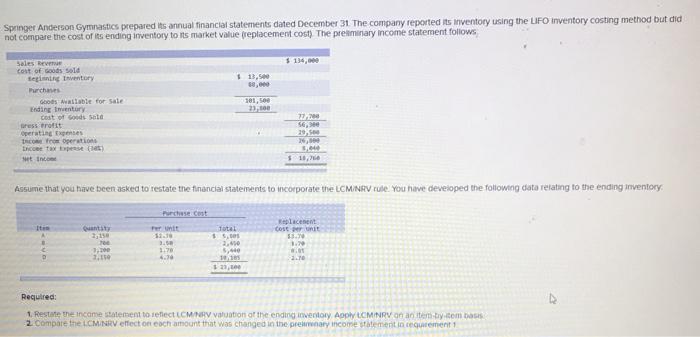

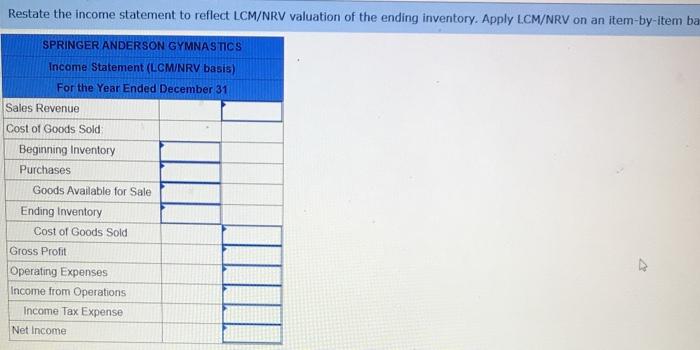

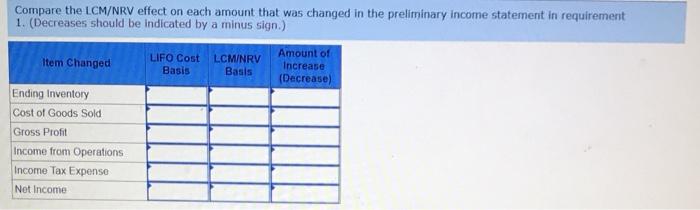

Springer Anderson Gymnastics prepared its annual financial statements dated December 31. The company reported its inventory using the LIFO inventory costing method but did not

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Next Step Advanced Medical Coding And Auditing 2016

Authors: Carol J. Buck MS CPC CCS-P

1st Edition

978-0323389105