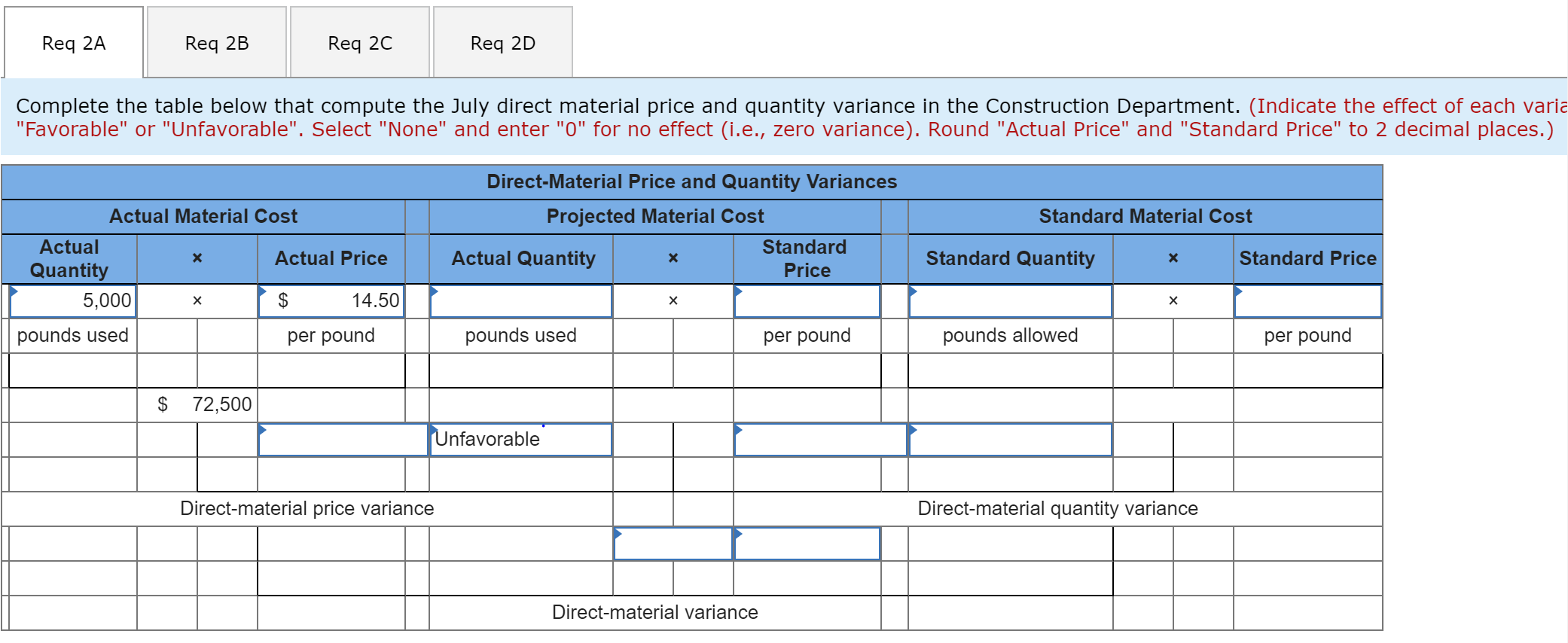

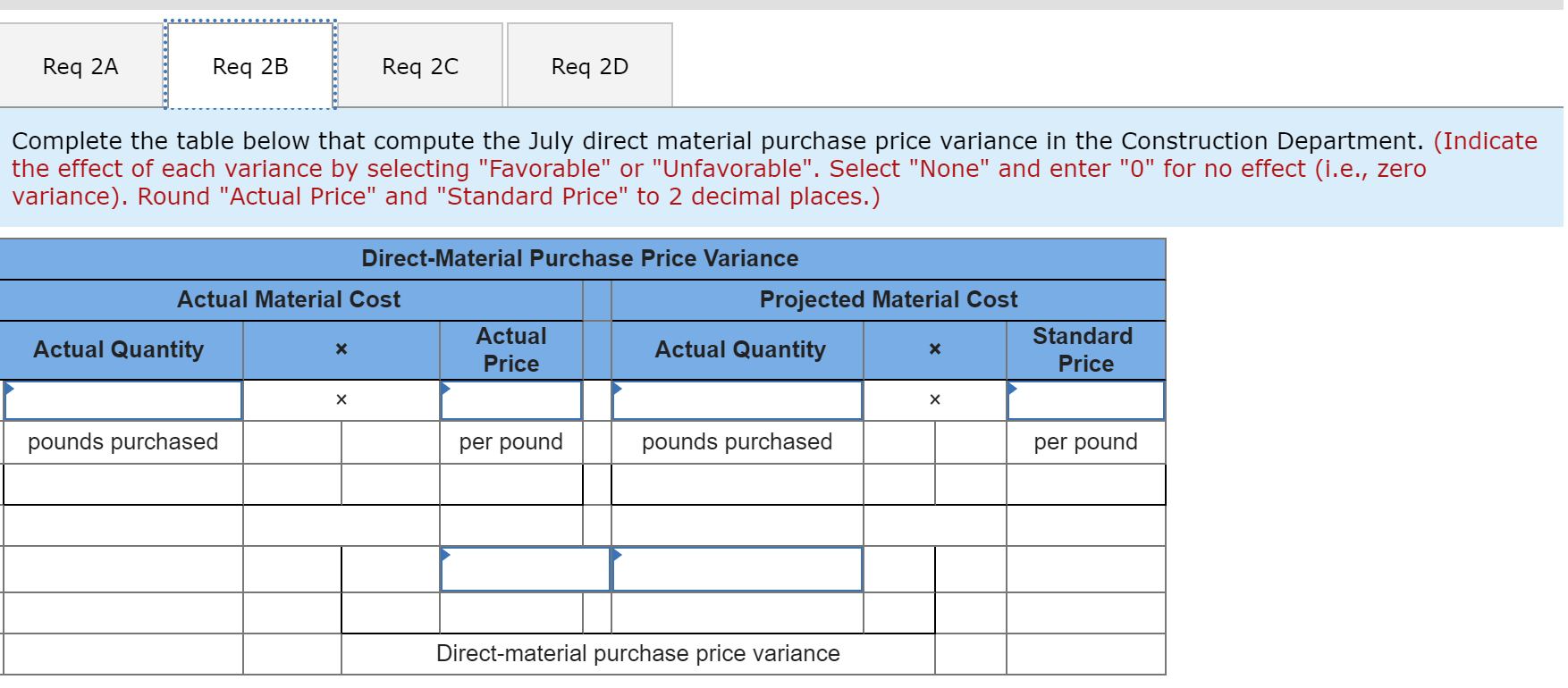

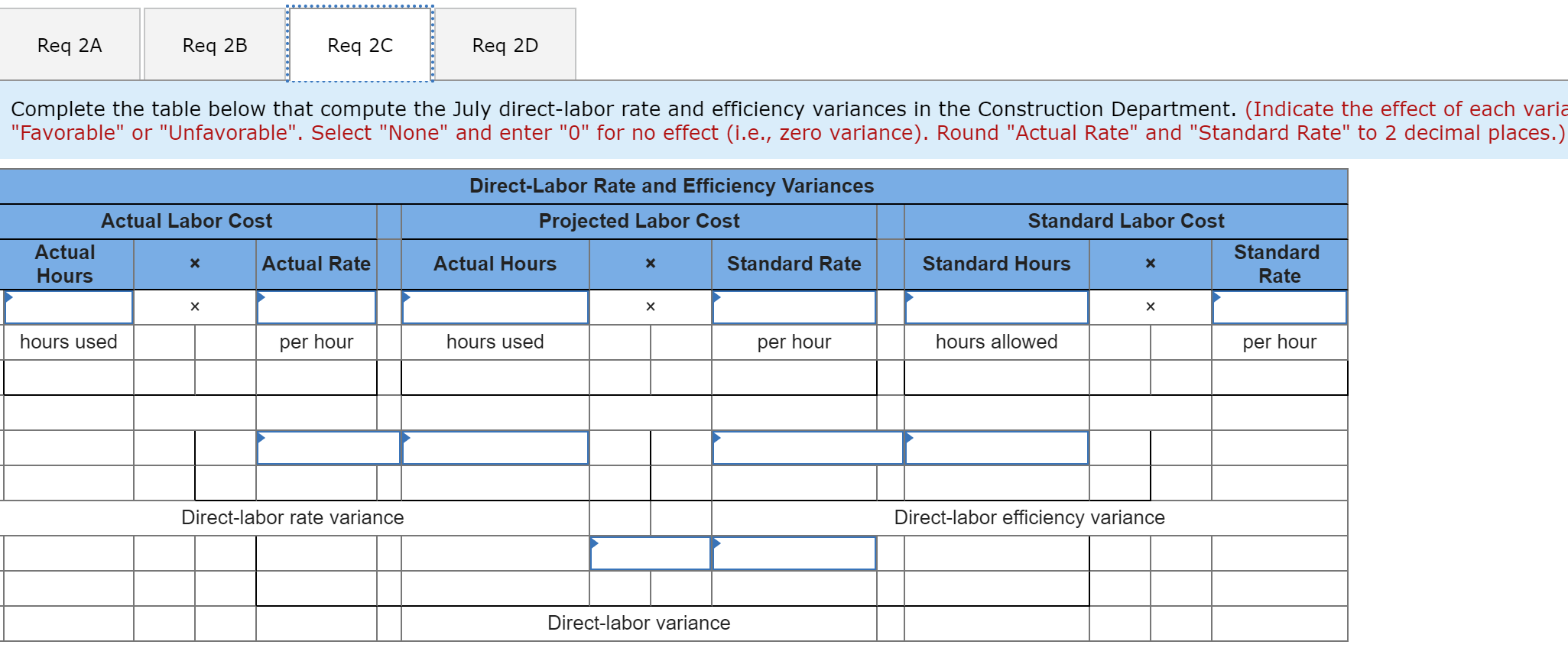

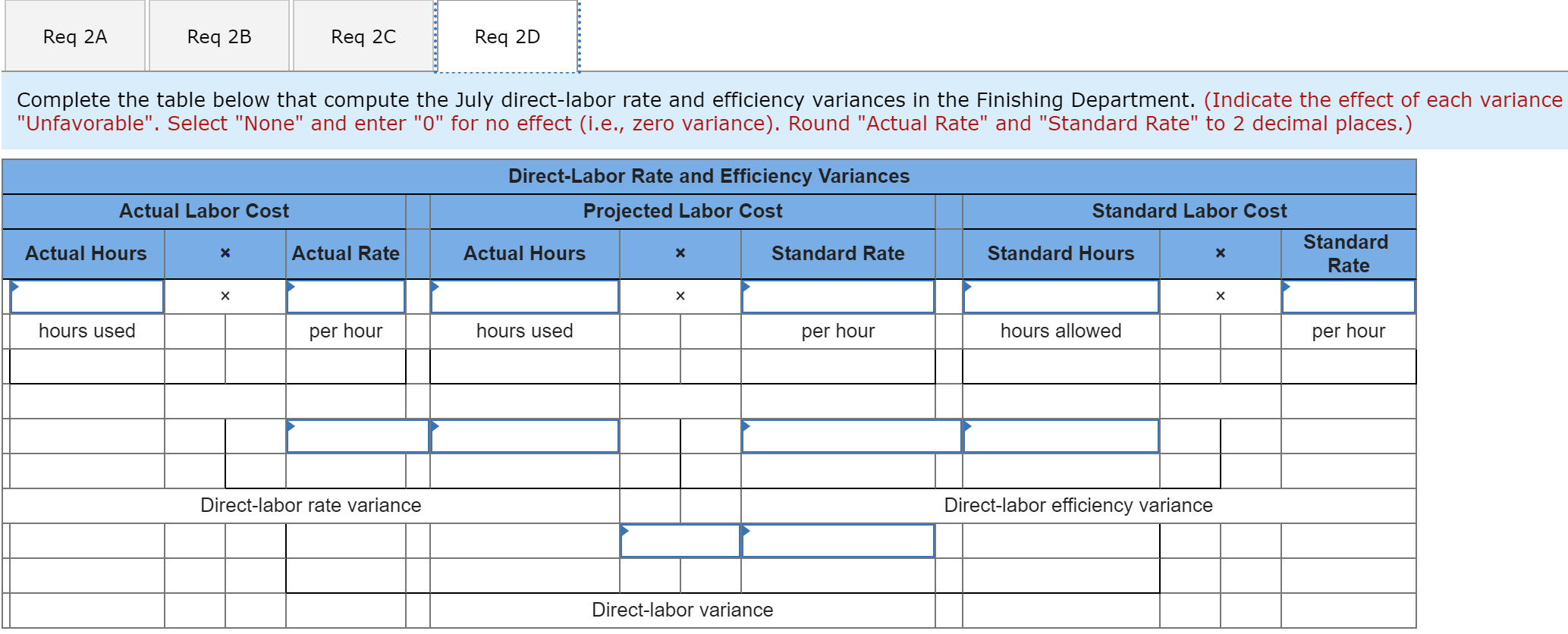

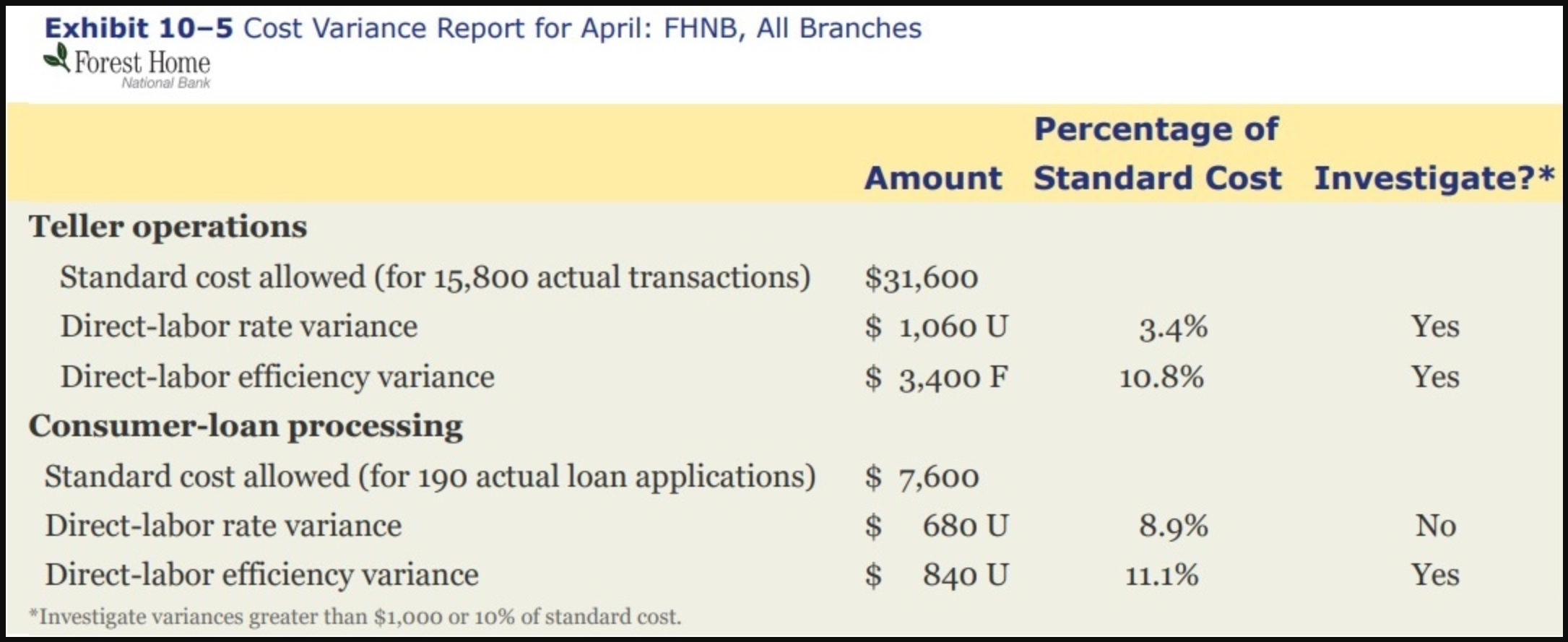

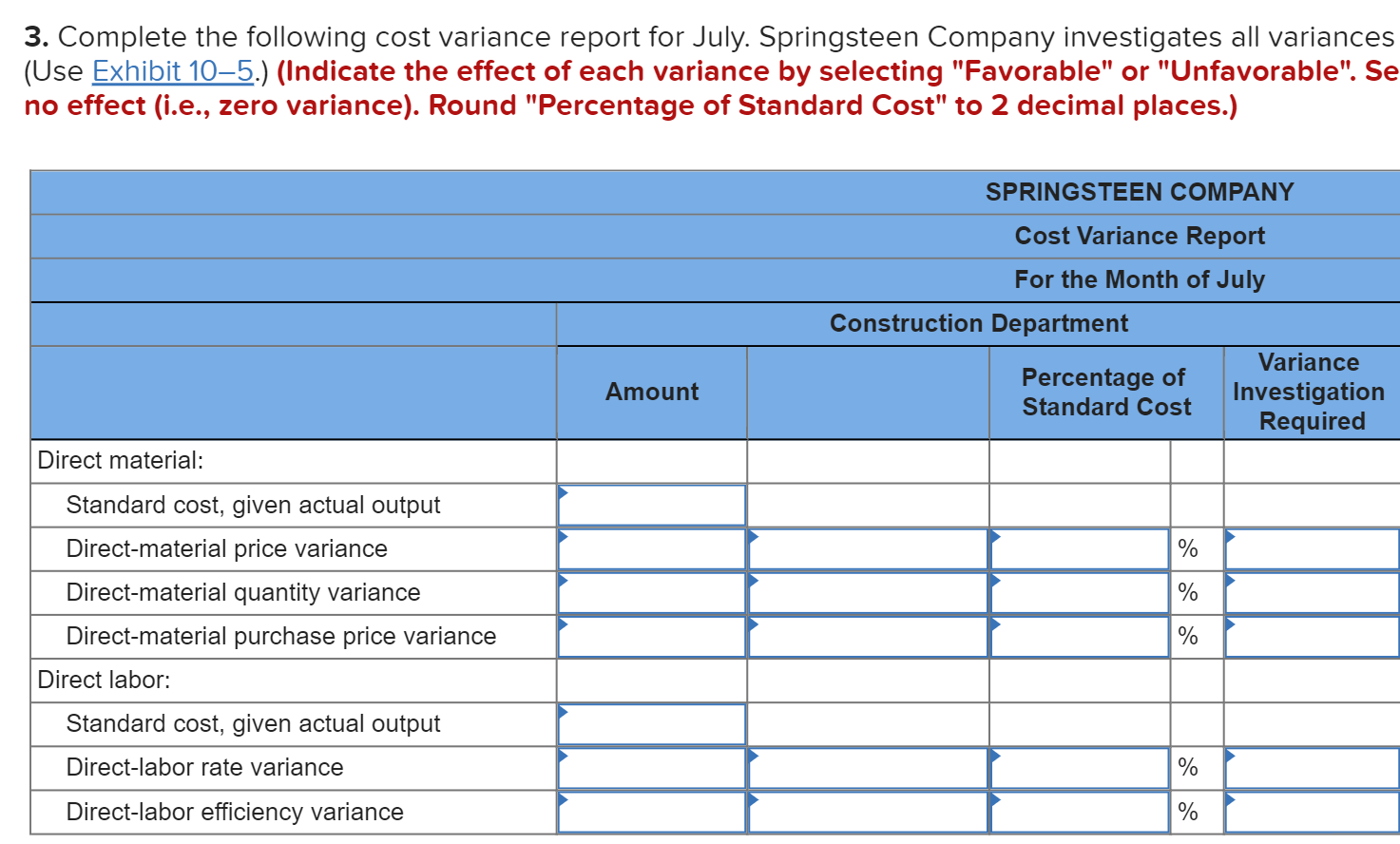

Springsteen Company manufactures guitars. The company uses a standard, job-order cost-accounting system in two production departments. In the Construction Department, the wooden guitars are built by highly skilled craftsmen and coated with several layers of lacquer. Then the units are transferred to the Finishing Department, where the bridge of the guitar is attached and the strings are installed. The guitars also are tuned and inspected in the Finishing Department. The diagram below depicts the production process. Construction Department Finishing Department (Basic guitar built from veneered wood.) (Bridge and strings attached; guitar tuned and inspected.) Each finished guitar contains seven pounds of veneered wood. In addition, one pound of wood is typically wasted in the production process. The veneered wood used in the guitars has a standard price of $14 per pound. The other parts needed to complete each guitar, such as the bridge and strings, cost $17 per guitar. The labor standards for Springsteen's two production departments are as follows: Construction Department: 6 hours of direct labor at $21 per hour Finishing Department: 2 hours of direct labor at $17 per hour The following pertains to the month of July. 1. There were no beginning or ending work-in-process inventories in either production department 2. There was no beginning finished-goods inventory. 3. Actual production was 550 guitars, and 350 guitars were sold on account for $425 each. 4. The company purchased 6,500 pounds of veneered wood at a price of $14.50 per pound. 5. Actual usage of veneered wood was 5,000 pounds of the wood purchased during July. 6. Enough parts (bridges and strings) to finish 650 guitars were purchased at a cost of $9,050. 7. The Construction Department used 3,100 direct-labor hours. The total direct-labor cost in the Construction Department was $62,000. 8. The Finishing Department used 1,150 direct-labor hours. The total direct-labor cost in that department was $20,700. 9. There were no direct-material variances in the Finishing Department. Req 2A Reg 2B Req 20 Req 2D Complete the table below that compute the July direct material price and quantity variance in the Construction Department. (Indicate the effect of each varia "Favorable" or "Unfavorable". Select "None" and enter "0" for no effect (i.e., zero variance). Round "Actual Price" and "Standard Price" to 2 decimal places.) Actual Material Cost Standard Material Cost Direct-Material Price and Quantity Variances Projected Material Cost Standard Actual Quantity Price X Actual Price X Standard Quantity X Standard Price Actual Quantity 5,000 $ 14.50 pounds used per pound pounds used per pound pounds allowed per pound $ 72,500 Unfavorable Direct-material price variance Direct-material quantity variance Direct-material variance Req 2A Req 2B Req 20 Req 2D Complete the table below that compute the July direct material purchase price variance in the Construction Department. (Indicate the effect of each variance by selecting "Favorable" or "Unfavorable". Select "None" and enter "0" for no effect (i.e., zero variance). Round "Actual Price" and "Standard Price" to 2 decimal places.) Direct-Material Purchase Price Variance Actual Material Cost Projected Material Cost Actual Actual Quantity Actual Quantity Price X Standard Price pounds purchased per pound pounds purchased per pound Direct-material purchase price variance Req 2A Req 2B Req 20 Req 2D Complete the table below that compute the July direct-labor rate and efficiency variances in the Construction Department. (Indicate the effect of each varia "Favorable" or "Unfavorable". Select "None" and enter "0" for no effect (i.e., zero variance). Round "Actual Rate" and "Standard Rate" to 2 decimal places.) Direct-Labor Rate and Efficiency Variances Projected Labor Cost Actual Labor Cost Actual Hours Standard Labor Cost Standard Standard Hours Rate Actual Rate Actual Hours X Standard Rate hours used per hour hours used per hour hours allowed per hour Direct-labor rate variance Direct-labor efficiency variance Direct-labor variance Req 2A Req 2B Req 20 Req 2D Complete the table below that compute the July direct-labor rate and efficiency variances in the Finishing Department. (Indicate the effect of each variance "Unfavorable". Select "None" and enter "O" for no effect (i.e., zero variance). Round "Actual Rate" and "Standard Rate" to 2 decimal places.) Direct-Labor Rate and Efficiency Variances Projected Labor Cost Actual Labor Cost Standard Labor Cost Actual Hours x Actual Rate Actual Hours x Standard Rate Standard Hours Standard Rate hours used per hour hours used per hour hours allowed per hour Direct-labor rate variance Direct-labor efficiency variance Direct-labor variance Exhibit 10-5 Cost Variance Report for April: FHNB, All Branches Forest Home National Bank Percentage of Amount Standard Cost Investigate?* $31,600 $ 1,060 U 3.4% Yes $ 3,400 F 10.8% Yes Teller operations Standard cost allowed (for 15,800 actual transactions) Direct-labor rate variance Direct-labor efficiency variance Consumer-loan processing Standard cost allowed (for 190 actual loan applications) Direct-labor rate variance Direct-labor efficiency variance * Investigate variances greater than $1,000 or 10% of standard cost. $ 7,600 $ 680 U 8.9% No $ 840 U 11.1% Yes 3. Complete the following cost variance report for July. Springsteen Company investigates all variances (Use Exhibit 105.) (Indicate the effect of each variance by selecting "Favorable" or "Unfavorable". Se no effect (i.e., zero variance). Round "Percentage of Standard Cost" to 2 decimal places.) SPRINGSTEEN COMPANY Cost Variance Report For the Month of July Construction Department Variance Percentage of Investigation Standard Cost Required Amount Direct material: % Standard cost, given actual output Direct-material price variance Direct-material quantity variance Direct-material purchase price variance % % Direct labor: Standard cost, given actual output Direct-labor rate variance % Direct-labor efficiency variance % Finishing Department Variance Investigation Required Amount Percentage of Standard Cost Variance Investigation Required % % % % %