Answered step by step

Verified Expert Solution

Question

1 Approved Answer

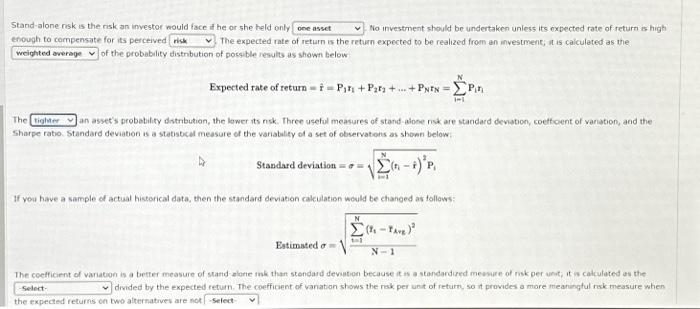

Stand-alone risk is the risk an investor would face if he or she held only one asset No investment should be undertaken unless its expected

Stand-alone risk is the risk an investor would face if he or she held only one asset No investment should be undertaken unless its expected rate of return is high enough to compensate for its perceived risk The expected rate of return is the return expected to be realized from an investment, it is calculated as the weighted average of the probability distribution of possible results as shown below Expected rate of return = f = Pr + Pr2+...+PNIN = = Pin The tighter V an asset's probability distribution, the lower its risk. Three useful measures of stand-alone risk are standard deviation, coefficient of variation, and the Sharpe ratio. Standard deviation is a statistical measure of the variability of a set of observations as shown below: Standard deviation == -Select- N (-1) 'P -) i=1 If you have a sample of actual historical data, then the standard deviation calculation would be changed as follows: Estimated = N i=1 N (ft FAvg.) - t-1 N-1 The coefficient of variation is a better measure of stand-alone risk than standard deviation because it is a standardized measure of risk per unit, it is calculated as the divided by the expected return. The coefficient of variation shows the risk per unit of return, so it provides a more meaningful risk measure when the expected returns on two alternatives are not -Select-

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Preppers Financial Guide

Authors: Jim Cobb

1st Edition

1612434037, 978-1612434032