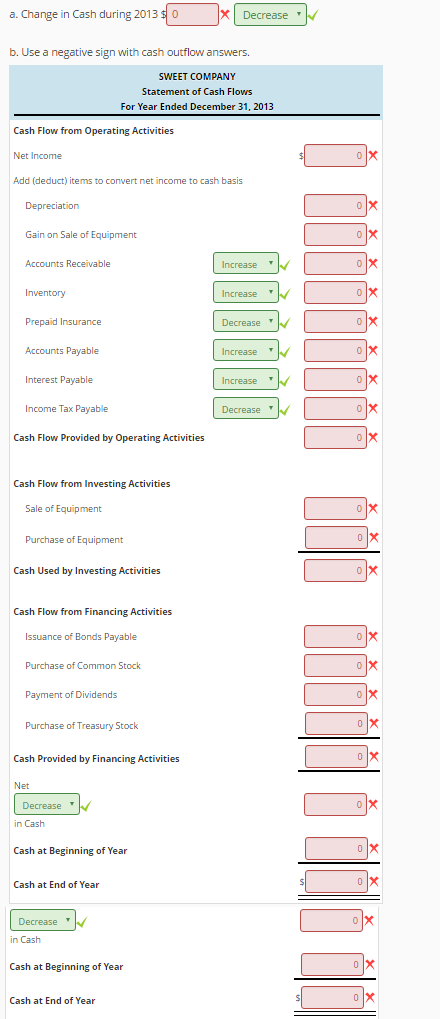

Question

Statement of Cash Flows (Indirect Method) The Sweet Company's income statement and comparative balance sheets as of December 31 of 2013 and 2012 are presented

Statement of Cash Flows (Indirect Method) The Sweet Company's income statement and comparative balance sheets as of December 31 of 2013 and 2012 are presented below:

| SWEET COMPANY Income Statement For the Year Ended December 31, 2013 | ||

|---|---|---|

| Sales Revenue | $1,324,400 | |

| Cost of Goods Sold | $709,800 | |

| Wages Expense | 284,200 | |

| Depreciation Expense | 84,000 | |

| Insurance Expense | 18,200 | |

| Interest Expense | 16,800 | |

| Income Tax Expense | 79,800 | |

| Gain on Sale of Equipment | (22,400) | 1,170,400 |

| Net Income | $154,000 | |

| SWEET COMPANY Balance Sheets | ||

|---|---|---|

| Dec. 31, 2013 | Dec. 31, 2012 | |

| Assets | ||

| Cash | $32,200 | $43,400 |

| Accounts Receivable | 95,200 | 60,200 |

| Inventory | 247,800 | 176,400 |

| Prepaid Insurance | 12,600 | 15,400 |

| Plant Assets | 1,241,800 | 1,078,000 |

| Accumulated Depreciation | (264,600) | (245,000) |

| Total Assets | $1,365,000 | $1,128,400 |

| Liabilities and Stockholders' Equity | ||

| Accounts Payable | $51,800 | $37,800 |

| Interest Payable | 7,000 | - |

| Income Tax Payable | 16,800 | 22,400 |

| Bonds Payable | 189,000 | 112,000 |

| Common Stock | 924,000 | 819,000 |

| Retained Earnings | 249,200 | 137,200 |

| Treasury Stock | (72,800) | - |

| Total Liabilities and Stockholders' Equity | $1,365,000 | $1,128,400 |

During the year, Sweet Company sold equipment for $37,800 cash that originally cost $79,800 and had $64,400 accumulated depreciation. New equipment was purchased for cash. Bonds payable and common stock were issued for cash. Cash dividends of $42,000 were declared and paid. At the end of the year, shares of treasury stock were purchased for cash. Accounts payable relate to merchandise purchases. Required a. Compute the change in cash that occurred during 2013. b. Prepare a statement of cash flows using the indirect method.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Accounting Oakton Community College Tools For Business Decision Making

Authors: Paul D. Kimmel ,Jerry J. Weygandt ,Donald E. Kieso

6th Edition

1118113632, 978-1118113639