Answered step by step

Verified Expert Solution

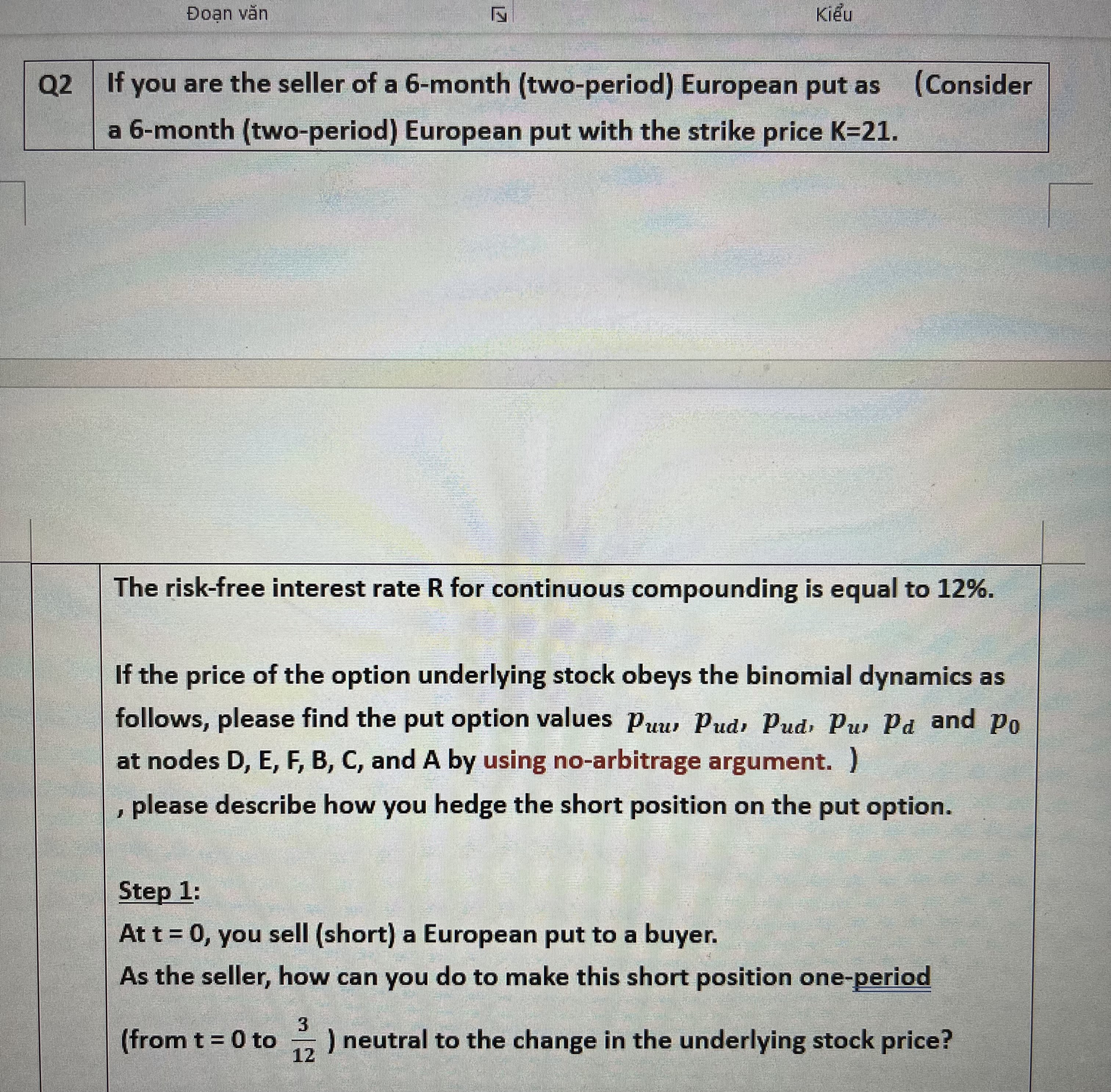

Question

1 Approved Answer

Step 1 : At t = 0 , you sell ( short ) a European put to a buyer. As the seller, how can you

Step :

At you sell short a European put to a buyer.

As the seller, how can you do to make this short position oneperiod from to neutral to the change in the underlying stock price?

Ans.

Step : At and

How much do you have in your bank account?

Ans.

When the price of the underlying stock goes up to $ the delta of the put option increase from to Show

Ans.

What's delta of the portfolio constructed at time if you keep the delta unchanged ie

Ans.

To make the portfolio delta neutral ie when how should you do

Step : At and

How much do you have in your bank account?

Ans.

When the price of the underlying stock goes down to $ the delta of the put option decrease from to Show

Ans.

To make the portfolio delta neutral ie when how should you do

Ans.

Step : Show your profits or losses when the stock price on the option maturity date is from

Ans.

Show your profits or losses when the stock price on the option maturity date is from

Ans.

Step : Show your profits or losses when the stock price on the option maturity date is from

Ans.

Show your profits or losses when the stock price on the option maturity date is from

Ans.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Global Financial Crisis What Have We Learnt

Authors: Steven Kates

1st Edition

0857934228, 978-0857934222