Answered step by step

Verified Expert Solution

Question

1 Approved Answer

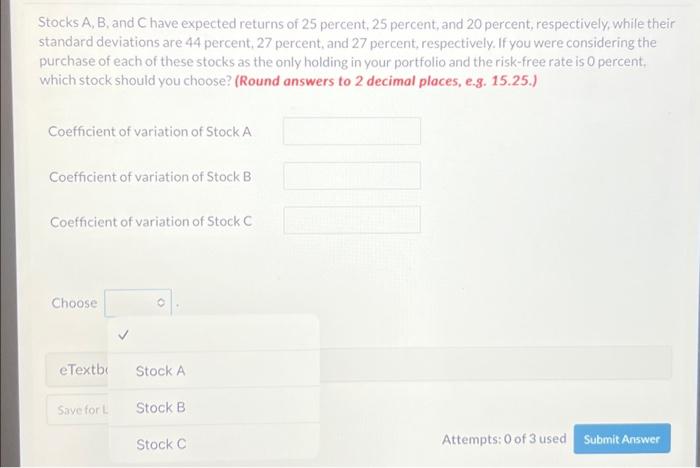

Stocks A, B, and C have expected returns of 25 percent, 25 percent, and 20 percent, respectively, while their standard deviations are 44 percent, 27

Stocks A, B, and C have expected returns of 25 percent, 25 percent, and 20 percent, respectively, while their standard deviations are 44 percent, 27 percent, and 27 percent, respectively. If you were considering the purchase of each of these stocks as the only holding in your portfolio and the risk-free rate is 0 percent, which stock should you choose? (Round answers to 2 decimal places, e.g. 15.25.) Coefficient of variation of Stock A Coefficient of variation of Stock B Coefficient of variation of Stock C Choose eTextb Save for L Stock A Stock B Stock C Attempts: 0 of 3 used Submit Answer

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Handbook Of Credit Portfolio Management

Authors: Greg Gregoriou, Christian Hoppe

1st Edition

0071598340, 978-0071598347