Summer is approaching and Steven and Sue Mahan have finally decided that their idea of a successful Southwestern furniture, art, and jewelry trading company has come of age. They know that summer is a popular tourist time in New Mexico and could be the best time to start this new business. The Mahans have had a long-time interest in Southwestern art and furniture. Steven graduated from college with an economics degree about 15 years ago and received his MBA in finance a few years later. He has been working in Dallas, TX, as the controller of a major wholesale distributor company for many years. His wife, Sue, who will be a full partner in the business, spent the first 10 years of her career in retail sales. Over the last several years, she has assumed more administrative duties for the group she works with.

Steven and Sue know they bring the expertise and skill to run a successful business, but to ensure success they have been researching the market for over five year's. They also know that they must be very careful and thoroughly research the business and industry they are pursuing. They have traveled extensively to New Mexico and have spent a good deal of time getting to know the local artists (primarily ski bums). They have found that there is a great demand for Southwestern furniture in Texas and the Southwest.

The Mahans have decided to open a shop called Southwest Trading Company in Taos, NM, and act as both a retailer and supplier to furniture and art outlets in Texas. Steven's extensive contacts with businesses in Dallas and Houston have given him the orders needed to make the business a success as soon as they begin shipping the goods. Sue has already begun marketing the Southwestern products. Southwest Trading Company's arrangements with the local craftspeople will allow very aggressive pricing of the goods to retail establishments in Texas. This aggressive pricing has been well received and tentative orders are already in place.

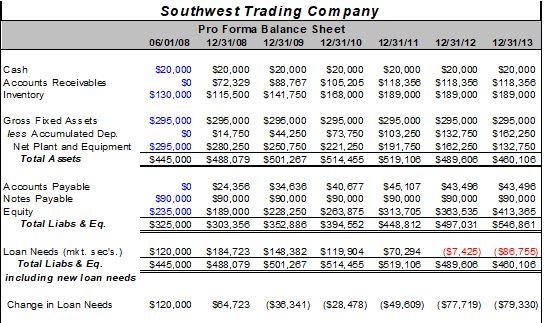

Steven has found an ideal location in Taos that is currently available. The owner is asking $275,000 for the space but Southwest Trading has a contract, contingent on financing, for $250,000. Steven and Sue have gotten bids on remodeling and should be able to renovate the space for about $45,000. Although they will purchase the building, the land is leased on a transferable lease with 65 years remaining. The Mahans have decided to invest $235,000, which represents most of their savings, into the venture. Sue's sister is also interested in the possibilities that the company exhibits and is lending Southwest $90,000. Repayment on the note to Sue's sister is not expected to begin for five years. They have estimated that they will need $130,000 in inventory to start the business and they will buy the inventory in cash to build goodwill with the local craftspeople. They also estimate that they will need $20,000 in cash to conduct day-to-day operations and bill payment.

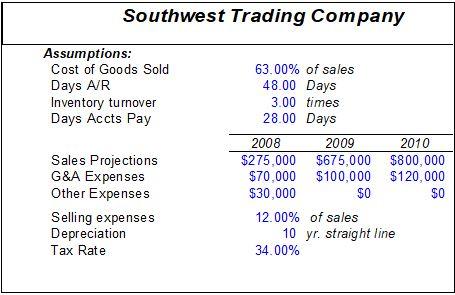

Wanting to use a local bank, Steven has approached Cary Farmer, the senior loan officer at Santa Fe National Bank in Santa Fe, NM, for financing. Steven's background in finance has allowed him to put together the following assumptions for their preliminary business plan. Steven believes that all renovations to the building and inventory can be in place by the end of June 2008.

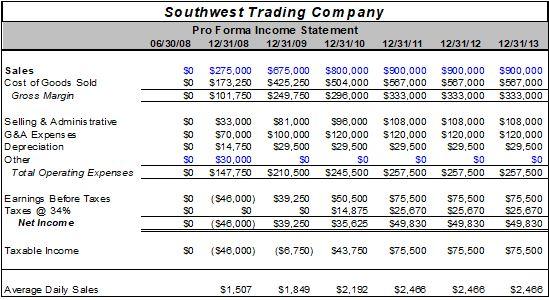

Sales are expected to be a bit lower the first year (July through December, 2008), since only six months will be included in the first fiscal year. Sales are expected to gtow significantly in the first full year, 2009, with growth leveling oft in the third and fourth years. Sales are expected to be $275,000, $675,000, $800,000, and $900,000 in 2008, 2009, 2010 and 2011, respectively. Sales are expected to level off after 2011.

Based on tentative agreements and orders, it is expected that cost of goods sold will average about 63 percent of sales.

General and administrative expenses are expected to be $70,000 for the six months in 2008, increase to $100,000 in 2009, and level off at $120,000 from 2010 forward. The land lease expenses and interest expenses are included in operational expenses.

Selling expenses are expected to be about 12 percent of sales and Sue is expecting to undertake extensive marketing and promotion efforts throughout Texas after the business is opened. It is expected that these additional promotional expenses will be about $30,000 in 2008 only.

The company will use 10-year straight-line depreciation of the building and improvements.

Southwest's effective tax rate is expected to be 34 percent.

Since they expect a good deal of business to be paid by credit card and to ship goods to Texas on credit, they expect to carry about 48 days of accounts receivable. They also expect that, because of the type of business they are entering, they will turn their inventory over about three times a year.

On the basis of the negotiations they have had with their craftspeople, suppliers, and other wholesale distributors, they estimate that they can count on about 28 days of accounts payable to help finance the business.

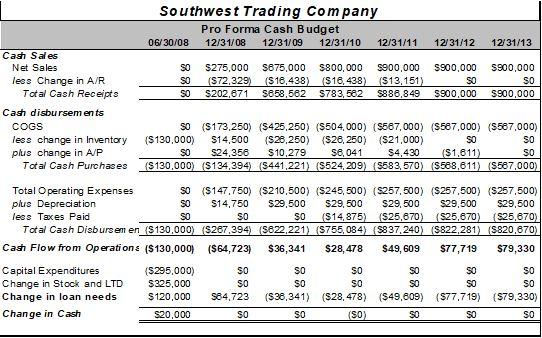

In preparing to go to the bank for the necessary loan, the Mahans want to prepare projected financial statements showing that Southwest Trading Company can make a profit and pay back the loan. They also want to know more precisely how much they will need to borrow from the bank to open the doors for business. The Mahans plan to prepare five years of balance sheet, income statement, and cash budget data for the bank. They must also develop an opening balance sheet as of the day they plan to open the doors, June 30, 2008.

- If the Bank commits to make this loan, how much money must it be willing to loan?

- What evidence does the Bank have that the Mahans are serious about this business venture?

- The projections provided to the Bank show no growth in sales after a few years. Why or why not should this be a problem in making this loan?

- What will provide the source of funds to repay the loan, and over what period of time should the loan be made.

- What should be your biggest concern about the financial statements?

- Would you make this loan? Whichever way you answer, please give two very brief reasons supporting your decision.

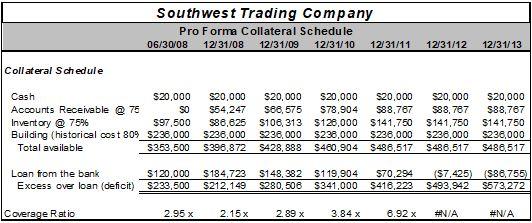

Southwest Trading Company Assumptions: Cost of Goods Sold Days A/R Inventory turnover Days Accts Pay Sales Projections G&A Expenses Other Expenses Selling expenses Depreciation Tax Rate 63.00% of sales 48.00 Days 3.00 times 28.00 Days 2008 2009 2010 $275,000 $675,000 $ $800,000 $70,000 $100,000 $120,000 $30,000 $0 $0 12.00% of sales 10 yr. straight line 34.00% Southwest Trading Company Pro Forma Balance Sheet 06/01/08 12/31/08 12/31/09 12/31/10 12/31/11 12/31/12 12/31/13 Cash Accounts Receivables Inventory $20,000 SO $130,000 $20,000 $72,329 $115,500 $20,000 988,767 $141.750 $20,000 $105,205 $168,000 $20,000 $118,358 $189,000 $20,000 S118,358 $189,000 $20,000 S118,356 $189,000 Gross Fixed Assets less Accumulated Dep. Net Plant and Equipment Total Assets $295,000 SO $295,000 $445,000 S296,000 $295,000 $295,000 S14,750 $44,250 $73,750 $280,250 $250.750 $221,250 S488,079 $501,267 S514,455 S295,000 S103,250 $191,750 $519,106 S295,000 S132,750 S162.250 S489,606 S295,000 $162.250 S132.750 S480,106 Accounts Payable Notes Payable Equity Total Liabs & Eq. SO $90,000 $225,000 $325,000 S24,358 $90,000 $189,000 $303,358 $34,636 $90,000 $228,250 $352,888 $40,677 $90,000 $263 875 $394,552 $45, 107 $90,000 S313,705 $448.812 $43,498 $90,000 S383,535 S497,031 $43,496 $90,000 S413,385 S548,861 Loan Needs (mkt. sec's.) Total Liabs & Eq. including new loan needs $120,000 S445,000 $184,723 $143,382 $488,079 $501,267 $119,904 $514,455 $70,294 $519, 100 {$7.425)86,755) S439,606 $480,106 Change in Loan Needs $120,000 984,723 ($38,341) (S28, 478) ($49.809) (877,719) (579,330) Southwest Trading Company Pro Forma Income Statement 06/30/08 12/31/08 12/31/09 12/31/10 12/31/11 12/31/12 12/31/13 Sales Cost of Goods Sold Gross Margin 888 $275,000 $173,250 $101.750 5675,000 S425,250 $249.750 $800,000 $504,000 S296,000 $900,000 S587,000 $333,000 S900,000 $587.000 $333,000 $900,000 S587,000 $333,000 SO SO Selling & Administrative G&A Expenses Depreciation Other Total Operating Expenses 88 888 $33,000 $70,000 $14.750 $30,000 S147,750 $81.000 S100.000 $29,500 SO S210.500 $98,000 $120,000 S29,500 SO $245,500 $ 108,000 S120,000 $29,500 $0 $257,500 $ 108,000 $120,000 $29,500 SO S257,500 $ 108,000 $120,000 $29,500 SO $257,500 Earnings Before Taxes Taxes @ 34% Net Income 888 (S46,000) SO (S46,000) $39,250 SO $39,250 $50,500 $14,875 $35,625 $75,500 $25,670 $49,830 $75,500 $25,670 S49,830 $75,500 $25.670 S49,830 Taxable income SO (S46,000) (S6,750) S43,750 $75,500 $75,500 $75,500 Average Daily Sales $1,507 $1,849 $2,192 S2.488 S2,468 $2,466 Southwest Trading Company Pro Forma Cash Budget 06/30/08 12/31/08 12/31/09 12/31/10 12/31/11 12/31/12 12/31/13 Cash Sales Net Sales SO $275,000 $875,000 $800,000 $900,000 $900.000 $900,000 lees Change in A/R SO (S72,329) (S16,438) (S16, 438) ($13,151) SO SO Total Cash Receipts SO S202,671 5658,562 $783,582 $886,849 S900.000 S900,000 Cash disbursements COGS So (S173,250) ($425,250) ($504,000) ($567,000) (S587,000) (S587,000) less change in Inventory ($130.000) $14,500 ($26,250) ($26,250) ($21,000) SO SO plus change in A/P SO $24.358 S10.279 S6, 041 $4,430 ($1.611) SO Total Cash Purchases (S130,000) (S134,394) (S441,221) (S524,209) (S583, 570) ($588,611) (S587,000) Total Operating Expenses SO (S147.750) (S210,500) ($245,500) (S257,500) ($257,500) ($257,500) plus Depreciation SO $14.750 $29,500 S29,500 $29,500 $29.500 $29,500 less Taxes Paid SO SO SO ($14,875) ($25.670) ($25.670) $25.670) Total Cash Disbursemen (S130,000) (S267,394) (5822,221) (S755, 084) (8837,240) ($822,281) (S820.870) Cash Flow from Operations ($130,000) ($64,723) $36,341 $28, 478 $49,609 $77,719 $79,330 Capital Expenditures (S295,000) SO SO So SO SO So Change in Stock and LTD $325,000 SO SO SO SO SO SO Change in loan needs $120,000 $84,723 (S36,341) ($28,478) ($49,609) ($77,719) (879,330) Change in Cash $20,000 SO SO (SO) SO SO SO Southwest Trading Company Pro Forma Collateral Schedule 06/30/08 12/31/08 12/31/09 12/31/10 12/31/11 12/31/12 12/31/13 Collateral Schedule Cash $20,000 $20,000 Accounts Receivable @ 75 SO $54,247 Inventory @ 759% $97,500 $86,625 Building (historical cost 809 5238,000 S238,000 Total available $353,500 $396,872 $20,000 $20,000 $20,000 S88,575 $78,904 $88,787 $106,313 $126,000 $141.750 S236,000 $238,000 S238,000 S428,888 S460,904 S486,517 $20,000 $88,787 $141,750 S238,000 S486,617 $20,000 $88,767 $141.750 $236,000 S486,517 Loen from the bank $120.000 Excess over loan (deficit) $233,500 $184,723 $212.149 $148.382 $119,904 $280,506 $341,000 $70,294 S416.223 (S7,425) ($86,755) $493,942 $573,272 Coverage Ratio 2.95 x 2.15 x 2.89 x 3.84 x 8.92 x #N/A #N/A Southwest Trading Company Assumptions: Cost of Goods Sold Days A/R Inventory turnover Days Accts Pay Sales Projections G&A Expenses Other Expenses Selling expenses Depreciation Tax Rate 63.00% of sales 48.00 Days 3.00 times 28.00 Days 2008 2009 2010 $275,000 $675,000 $ $800,000 $70,000 $100,000 $120,000 $30,000 $0 $0 12.00% of sales 10 yr. straight line 34.00% Southwest Trading Company Pro Forma Balance Sheet 06/01/08 12/31/08 12/31/09 12/31/10 12/31/11 12/31/12 12/31/13 Cash Accounts Receivables Inventory $20,000 SO $130,000 $20,000 $72,329 $115,500 $20,000 988,767 $141.750 $20,000 $105,205 $168,000 $20,000 $118,358 $189,000 $20,000 S118,358 $189,000 $20,000 S118,356 $189,000 Gross Fixed Assets less Accumulated Dep. Net Plant and Equipment Total Assets $295,000 SO $295,000 $445,000 S296,000 $295,000 $295,000 S14,750 $44,250 $73,750 $280,250 $250.750 $221,250 S488,079 $501,267 S514,455 S295,000 S103,250 $191,750 $519,106 S295,000 S132,750 S162.250 S489,606 S295,000 $162.250 S132.750 S480,106 Accounts Payable Notes Payable Equity Total Liabs & Eq. SO $90,000 $225,000 $325,000 S24,358 $90,000 $189,000 $303,358 $34,636 $90,000 $228,250 $352,888 $40,677 $90,000 $263 875 $394,552 $45, 107 $90,000 S313,705 $448.812 $43,498 $90,000 S383,535 S497,031 $43,496 $90,000 S413,385 S548,861 Loan Needs (mkt. sec's.) Total Liabs & Eq. including new loan needs $120,000 S445,000 $184,723 $143,382 $488,079 $501,267 $119,904 $514,455 $70,294 $519, 100 {$7.425)86,755) S439,606 $480,106 Change in Loan Needs $120,000 984,723 ($38,341) (S28, 478) ($49.809) (877,719) (579,330) Southwest Trading Company Pro Forma Income Statement 06/30/08 12/31/08 12/31/09 12/31/10 12/31/11 12/31/12 12/31/13 Sales Cost of Goods Sold Gross Margin 888 $275,000 $173,250 $101.750 5675,000 S425,250 $249.750 $800,000 $504,000 S296,000 $900,000 S587,000 $333,000 S900,000 $587.000 $333,000 $900,000 S587,000 $333,000 SO SO Selling & Administrative G&A Expenses Depreciation Other Total Operating Expenses 88 888 $33,000 $70,000 $14.750 $30,000 S147,750 $81.000 S100.000 $29,500 SO S210.500 $98,000 $120,000 S29,500 SO $245,500 $ 108,000 S120,000 $29,500 $0 $257,500 $ 108,000 $120,000 $29,500 SO S257,500 $ 108,000 $120,000 $29,500 SO $257,500 Earnings Before Taxes Taxes @ 34% Net Income 888 (S46,000) SO (S46,000) $39,250 SO $39,250 $50,500 $14,875 $35,625 $75,500 $25,670 $49,830 $75,500 $25,670 S49,830 $75,500 $25.670 S49,830 Taxable income SO (S46,000) (S6,750) S43,750 $75,500 $75,500 $75,500 Average Daily Sales $1,507 $1,849 $2,192 S2.488 S2,468 $2,466 Southwest Trading Company Pro Forma Cash Budget 06/30/08 12/31/08 12/31/09 12/31/10 12/31/11 12/31/12 12/31/13 Cash Sales Net Sales SO $275,000 $875,000 $800,000 $900,000 $900.000 $900,000 lees Change in A/R SO (S72,329) (S16,438) (S16, 438) ($13,151) SO SO Total Cash Receipts SO S202,671 5658,562 $783,582 $886,849 S900.000 S900,000 Cash disbursements COGS So (S173,250) ($425,250) ($504,000) ($567,000) (S587,000) (S587,000) less change in Inventory ($130.000) $14,500 ($26,250) ($26,250) ($21,000) SO SO plus change in A/P SO $24.358 S10.279 S6, 041 $4,430 ($1.611) SO Total Cash Purchases (S130,000) (S134,394) (S441,221) (S524,209) (S583, 570) ($588,611) (S587,000) Total Operating Expenses SO (S147.750) (S210,500) ($245,500) (S257,500) ($257,500) ($257,500) plus Depreciation SO $14.750 $29,500 S29,500 $29,500 $29.500 $29,500 less Taxes Paid SO SO SO ($14,875) ($25.670) ($25.670) $25.670) Total Cash Disbursemen (S130,000) (S267,394) (5822,221) (S755, 084) (8837,240) ($822,281) (S820.870) Cash Flow from Operations ($130,000) ($64,723) $36,341 $28, 478 $49,609 $77,719 $79,330 Capital Expenditures (S295,000) SO SO So SO SO So Change in Stock and LTD $325,000 SO SO SO SO SO SO Change in loan needs $120,000 $84,723 (S36,341) ($28,478) ($49,609) ($77,719) (879,330) Change in Cash $20,000 SO SO (SO) SO SO SO Southwest Trading Company Pro Forma Collateral Schedule 06/30/08 12/31/08 12/31/09 12/31/10 12/31/11 12/31/12 12/31/13 Collateral Schedule Cash $20,000 $20,000 Accounts Receivable @ 75 SO $54,247 Inventory @ 759% $97,500 $86,625 Building (historical cost 809 5238,000 S238,000 Total available $353,500 $396,872 $20,000 $20,000 $20,000 S88,575 $78,904 $88,787 $106,313 $126,000 $141.750 S236,000 $238,000 S238,000 S428,888 S460,904 S486,517 $20,000 $88,787 $141,750 S238,000 S486,617 $20,000 $88,767 $141.750 $236,000 S486,517 Loen from the bank $120.000 Excess over loan (deficit) $233,500 $184,723 $212.149 $148.382 $119,904 $280,506 $341,000 $70,294 S416.223 (S7,425) ($86,755) $493,942 $573,272 Coverage Ratio 2.95 x 2.15 x 2.89 x 3.84 x 8.92 x #N/A #N/A