Answered step by step

Verified Expert Solution

Question

1 Approved Answer

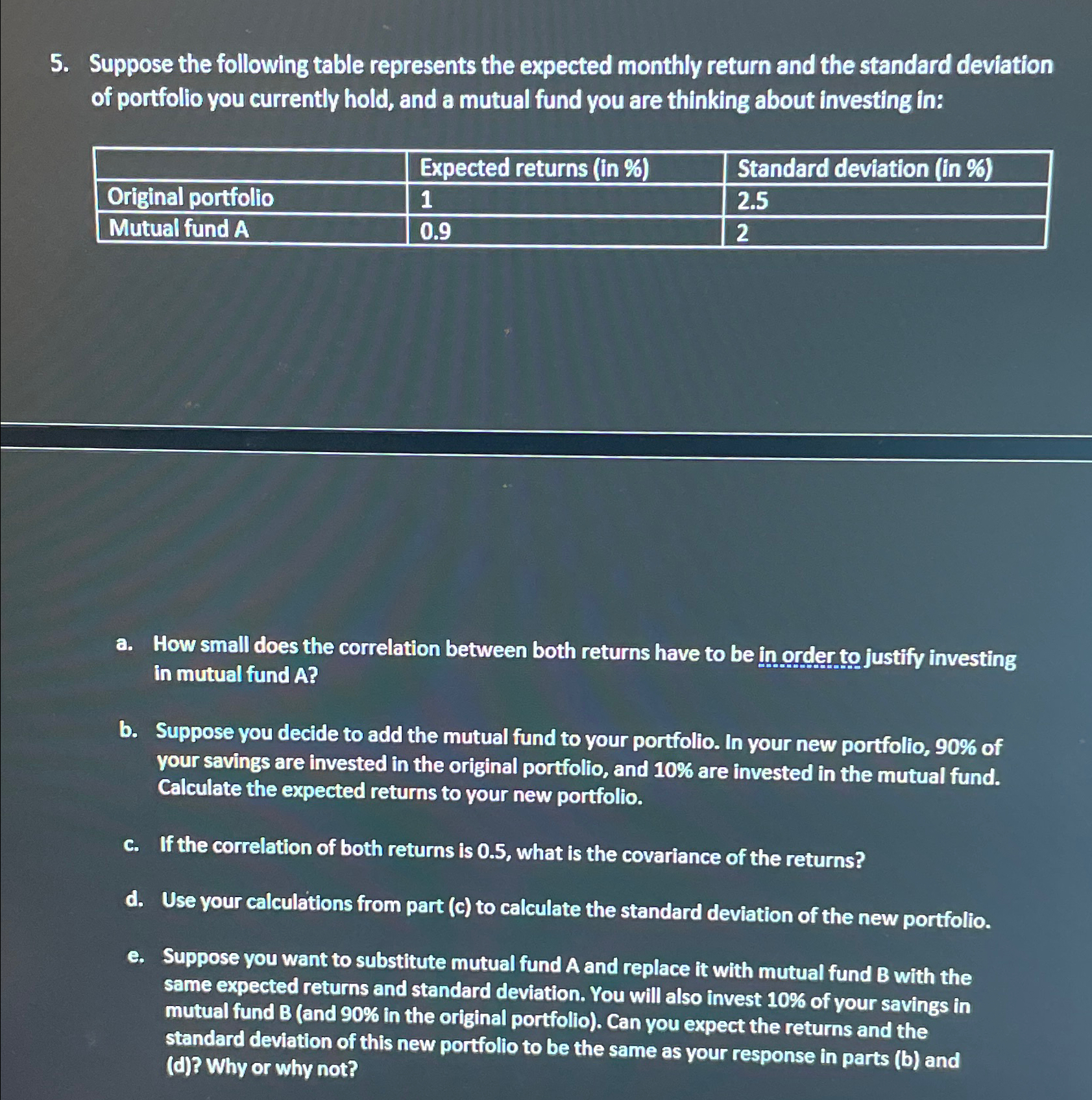

Suppose the following table represents the expected monthly return and the standard deviation of portfolio you currently hold, and a mutual fund you are thinking

Suppose the following table represents the expected monthly return and the standard deviation of portfolio you currently hold, and a mutual fund you are thinking about investing in:

tableExpected returns in Standard deviation in Original portfolio,Mutual fund A

a How small does the correlation between both returns have to be in order to justify investing in mutual fund

b Suppose you decide to add the mutual fund to your portfolio. In your new portfolio, of your savings are invested in the original portfolio, and are invested in the mutual fund. Calculate the expected returns to your new portfolio.

c If the correlation of both returns is what is the covariance of the returns?

d Use your calculations from part c to calculate the standard deviation of the new portfolio.

e Suppose you want to substitute mutual fund A and replace it with mutual fund with the same expected returns and standard deviation. You will also invest of your savings in mutual fund B and in the original portfolio Can you expect the returns and the standard deviation of this new portfolio to be the same as your response in parts b and d Why or why not?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Complete Personal Finance Handbook

Authors: Teri B Clark

1st Edition

160138047X, 978-1601380470