Answered step by step

Verified Expert Solution

Question

1 Approved Answer

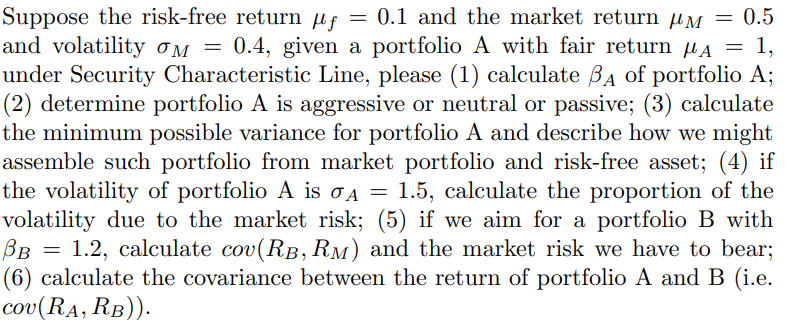

Suppose the risk-free return f=0.1 and the market return M=0.5 and volatility M=0.4, given a portfolio A with fair return A=1, under Security Characteristic Line,

Suppose the risk-free return f=0.1 and the market return M=0.5 and volatility M=0.4, given a portfolio A with fair return A=1, under Security Characteristic Line, please (1) calculate A of portfolio A; (2) determine portfolio A is aggressive or neutral or passive; (3) calculate the minimum possible variance for portfolio A and describe how we might assemble such portfolio from market portfolio and risk-free asset; (4) if the volatility of portfolio A is A=1.5, calculate the proportion of the volatility due to the market risk; (5) if we aim for a portfolio B with B=1.2, calculate cov(RB,RM) and the market risk we have to bear; (6) calculate the covariance between the return of portfolio A and B (i.e. cov(RA,RB))

Suppose the risk-free return f=0.1 and the market return M=0.5 and volatility M=0.4, given a portfolio A with fair return A=1, under Security Characteristic Line, please (1) calculate A of portfolio A; (2) determine portfolio A is aggressive or neutral or passive; (3) calculate the minimum possible variance for portfolio A and describe how we might assemble such portfolio from market portfolio and risk-free asset; (4) if the volatility of portfolio A is A=1.5, calculate the proportion of the volatility due to the market risk; (5) if we aim for a portfolio B with B=1.2, calculate cov(RB,RM) and the market risk we have to bear; (6) calculate the covariance between the return of portfolio A and B (i.e. cov(RA,RB)) Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Bankers Handbook On Credit Management

Authors: Indian Institute Of Banking & Finance

1st Edition

9387957853, 978-9387957855