Suppose the spot exchange rates among some important currencies are as follows: /$ : 0.6584-0.6592 /$ : 105.720-105.780 / : 0.00482-0.00487 /: 0.7979-0.7999 /$: 0.5095-0.5105

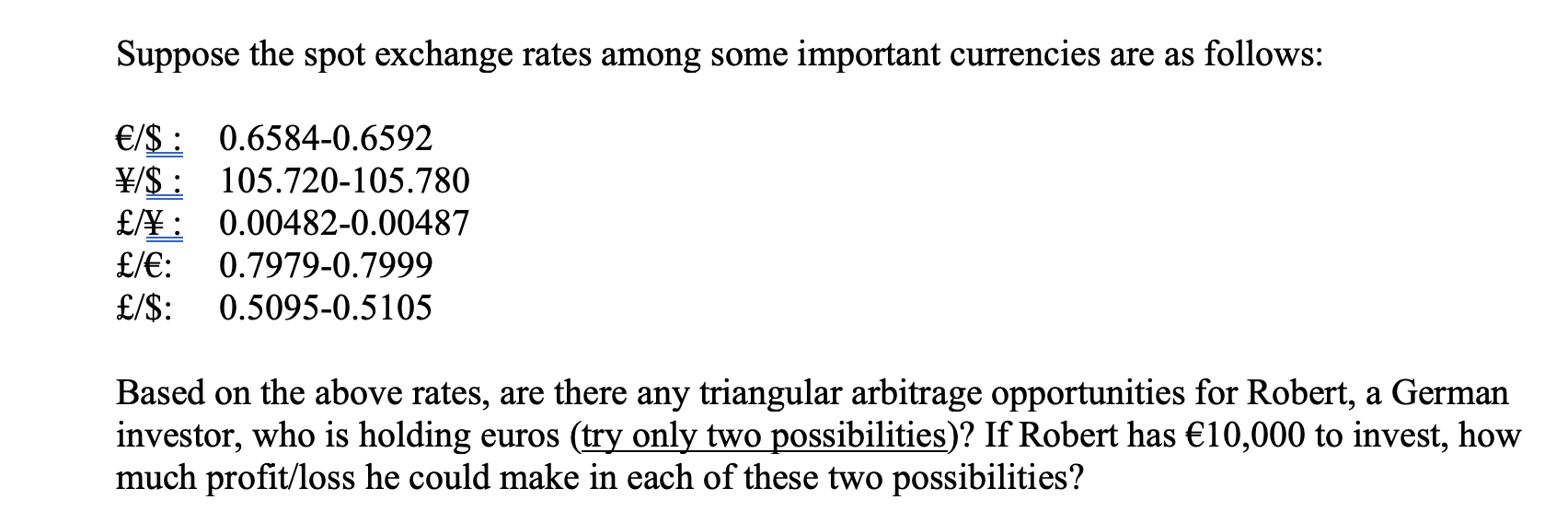

Suppose the spot exchange rates among some important currencies are as follows:

/$ : 0.6584-0.6592

/$ : 105.720-105.780

/ : 0.00482-0.00487

/: 0.7979-0.7999

/$: 0.5095-0.5105

Based on the above rates, are there any triangular arbitrage opportunities for Robert, a German investor, who is holding euros (try only two possibilities)? If Robert has 10,000 to invest, how much profit/loss he could make in each of these two possibilities?

Suppose the spot exchange rates among some important currencies are as follows: /$: 0.6584-0.6592 \/$ : 105.720-105.780 /: 0.00482-0.00487 /: 0.7979-0.7999 /$: 0.5095-0.5105 Based on the above rates, are there any triangular arbitrage opportunities for Robert, a German investor, who is holding euros (try only two possibilities)? If Robert has 10,000 to invest, how much profit/loss he could make in each of these two possibilities

Step by Step Solution

There are 3 Steps involved in it

Step: 1

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Authors: Anthony Saunders, Marcia Cornett

6th edition

9780077641849, 77861663, 77641841, 978-0077861667