Answered step by step

Verified Expert Solution

Question

1 Approved Answer

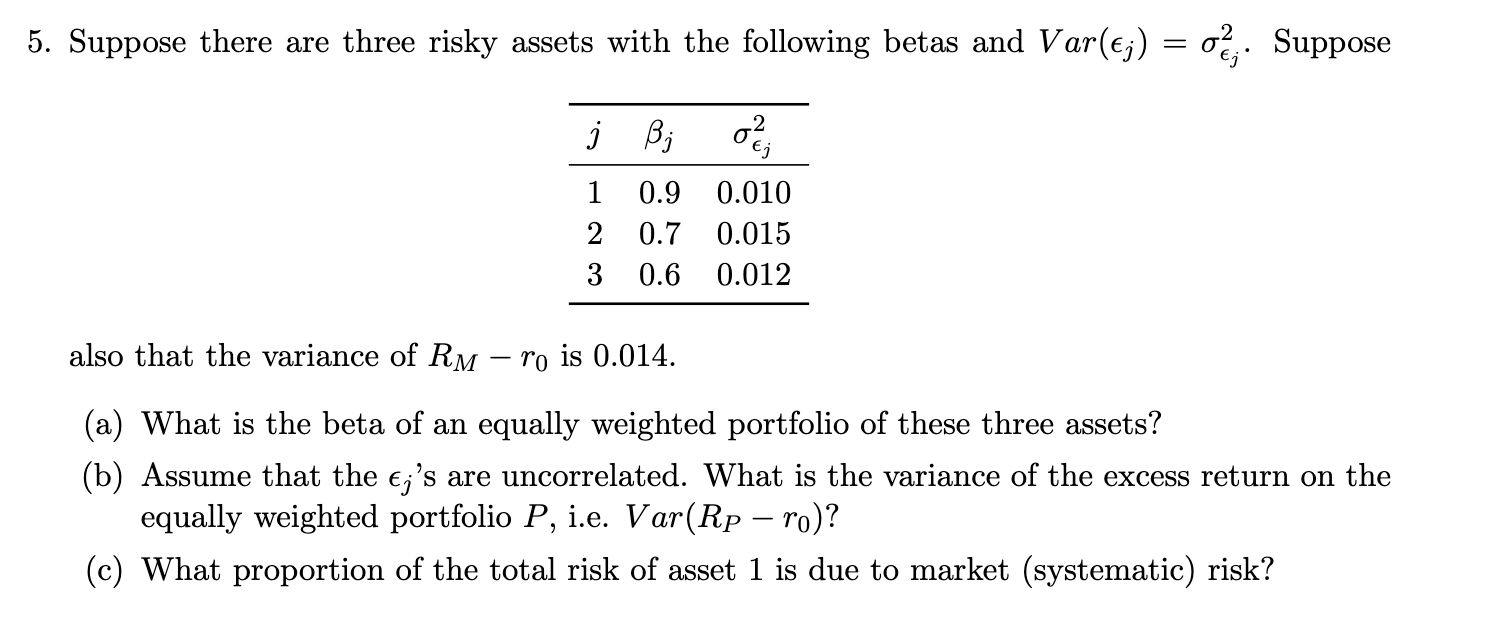

Suppose there are three risky assets with the following betas and Var ( l o n j ) = l o n j 2 .

Suppose there are three risky assets with the following betas and Var Suppose also that the variance of is a What is the beta of an equally weighted portfolio of these three assets? b Assume that the s are uncorrelated. What is the variance of the excess return on the equally weighted portfolio ie Var c What proportion of the total risk of asset is due to market systematic risk?

Suppose there are three risky assets with the following betas and Var Suppose

also that the variance of is

a What is the beta of an equally weighted portfolio of these three assets?

b Assume that the s are uncorrelated. What is the variance of the excess return on the

equally weighted portfolio ie Var

c What proportion of the total risk of asset is due to market systematic risk?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Banking And Finance Managing The Moral Dimension

Authors: James Lynch

1st Edition

1855731762, 978-1855731769