Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Suppose you have a current portfolio of $250,000 composed of two assets: 30% is invested in the risk-free asset RF and 70% in an

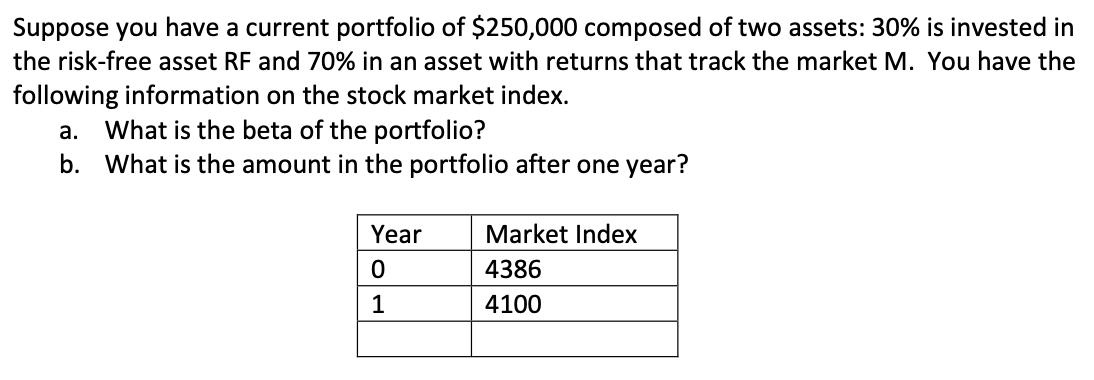

Suppose you have a current portfolio of $250,000 composed of two assets: 30% is invested in the risk-free asset RF and 70% in an asset with returns that track the market M. You have the following information on the stock market index. a. What is the beta of the portfolio? b. What is the amount in the portfolio after one year? Year Market Index 0 4386 1 4100

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Corporate Finance A Focused Approach

Authors: Michael C. Ehrhardt, Eugene F. Brigham

6th edition

1305637100, 978-1305637108