Answered step by step

Verified Expert Solution

Question

1 Approved Answer

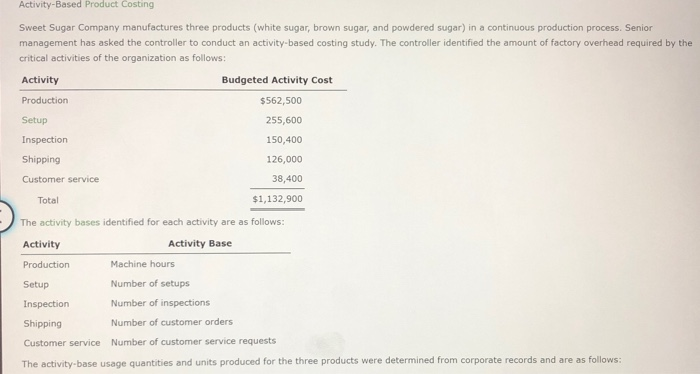

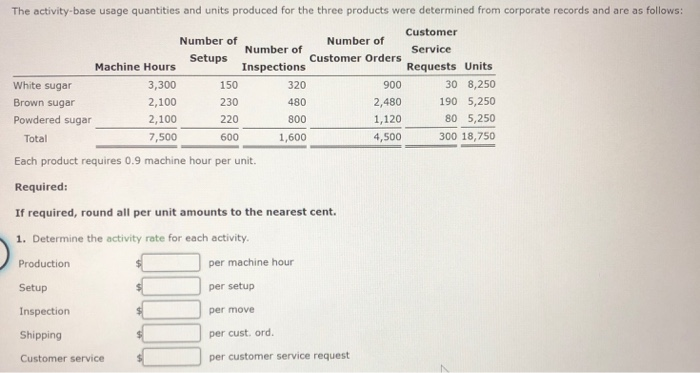

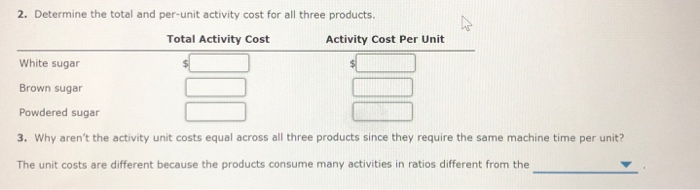

sweet sugar company Activity-Based Product Costing Sweet Sugar Company manufactures three products (white sugar, brown sugar, and powdered sugar) in a continuous production process. Senior

sweet sugar company

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Social Media Audits Achieving Deep Impact Without Sacrificing The Bottom Line

Authors: Urs E Gattiker

1st Edition

1843347458, 978-1843347453