Answered step by step

Verified Expert Solution

Question

1 Approved Answer

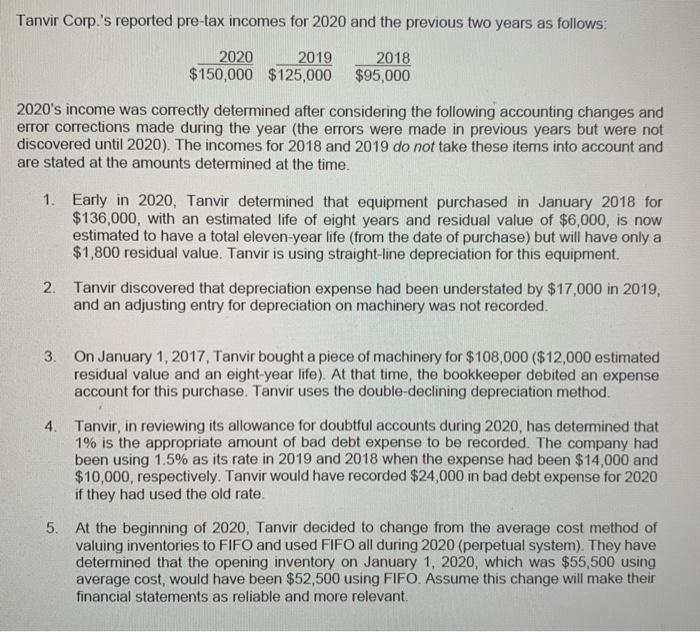

Tanvir Corp.'s reported pre-tax incomes for 2020 and the previous two years as follows: 2020 2019 $150,000 $125,000 2018 $95,000 2020's income was correctly determined

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Construction Contractors AICPA Audit And Accounting Guide

Authors: American Institute Of CPAs

1st Edition

0870519751, 978-0870519758