Answered step by step

Verified Expert Solution

Question

1 Approved Answer

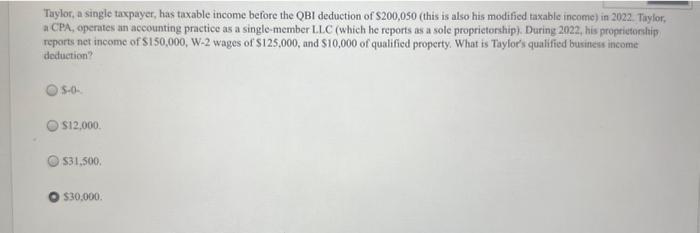

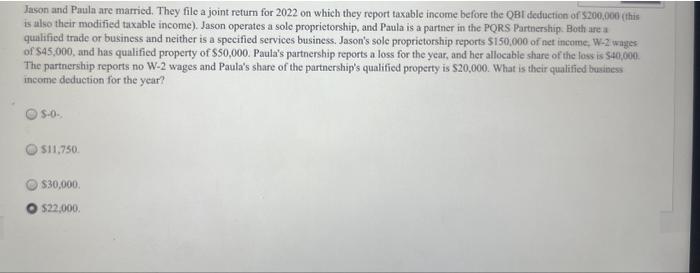

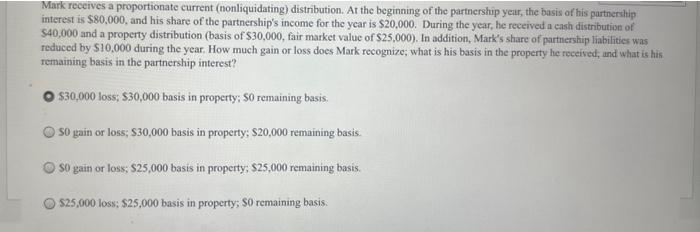

Taylor, a single taxpayer, has taxable income before the QB1 deduction of $200,050 (this is also his modified taxable income) in 2022 . Tiylor, a

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Understanding And Auditing Corporate Culture A Maturity Model Approach

Authors: Angelina K. Y. Chin, CIA, CRMA, CPA

1st Edition

1634540719, 978-1634540711