thank you

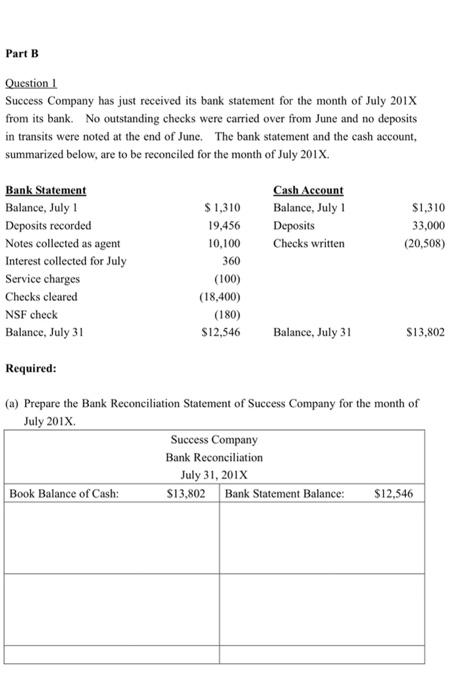

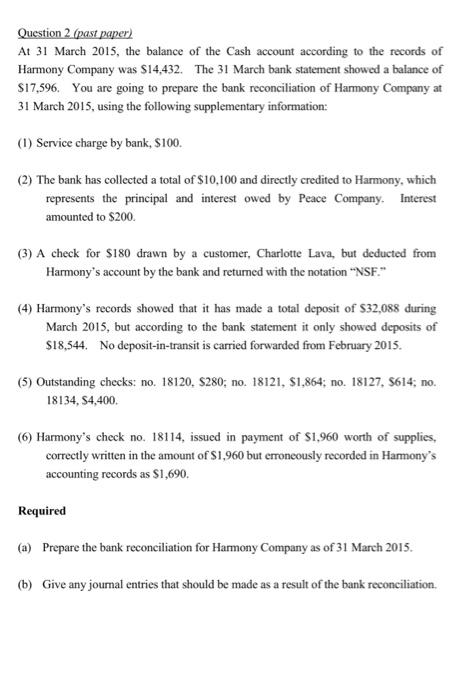

BHMH2101 Financial Accounting Reinforcement exercise - Chapter 71) Part A 1. Which of the following is NOT included in the financial assets? A. Cash B. Investments in securities. C. Inventories. D. Accounts receivable. 2. An NSF check returned by the bank should be entered in the depositor's accounting records by a debit to: A. Accounts Receivable. B. An expense account C. Cash D. Cash Over and Short 3. Which of the following can be considered as an effective control of cash? A. One person handles the receipts and disbursements of cash. B. Cash is deposited monthly into a bank C. There is approval of cash payments. D. A reconciliation of the bank balance with the cash balance is prepared twice a year 4. A bank reconciliation explains the differences between A. cash receipts and cash disbursements for the period B. the balance of cash in the bank and the budgeted expenditures for the upcoming accounting period C. the balance per bank statement and the cash balance per the accounting records of the depositor D. the balance per bank statement and cash expected to be on hand according to the cash forecast 5. When preparing bank reconciliation, deposits in transit will: A. Increase the balance per depositor's records. B. Decrease the balance per depositor's records. C. Increase the balance per the bank statement. D. Decrease the balance per the bank statement. Part B Question 1 Success Company has just received its bank statement for the month of July 2017 from its bank. No outstanding checks were carried over from June and no deposits in transits were noted at the end of June. The bank statement and the cash account, summarized below, are to be reconciled for the month of July 2017 Cash Account Balance, July 1 Deposits Checks written $1,310 33,000 (20,508) Bank Statement Balance, July 1 Deposits recorded Notes collected as agent Interest collected for July Service charges Checks cleared NSF check Balance, July 31 $ 1,310 19,456 10,100 360 (100) (18,400) (180) $12,546 Balance, July 31 $13,802 Required: (a) Prepare the Bank Reconciliation Statement of Success Company for the month of July 2017 Success Company Bank Reconciliation July 31, 2017 Book Balance of Cash $13,802 Bank Statement Balance: $12,546 (b) Prepare the journal entries to adjust the account at 31 July, 201X. Question 2. Grast paper) At 31 March 2015, the balance of the Cash account according to the records of Harmony Company was $14,432. The 31 March bank statement showed a balance of $17,596. You are going to prepare the bank reconciliation of Harmony Company at 31 March 2015, using the following supplementary information: (1) Service charge by bank, $100. (2) The bank has collected a total of $10,100 and directly credited to Harmony, which represents the principal and interest owed by Peace Company. Interest amounted to $200 (3) A check for $180 drawn by a customer, Charlotte Lava, but deducted from Harmony's account by the bank and returned with the notation "NSF." (4) Harmony's records showed that it has made a total deposit of $32,088 during March 2015, but according to the bank statement it only showed deposits of $18,544. No deposit-in-transit is carried forwarded from February 2015. (5) Outstanding checks: no. 18120, $280, no. 18121, $1,864, no. 18127, 5614; no. 18134, S4,400. (6) Harmony's check no. 18114, issued in payment of $1,960 worth of supplies, correctly written in the amount of S1,960 but erroneously recorded in Harmony's accounting records as $1,690. Required (a) Prepare the bank reconciliation for Harmony Company as of 31 March 2015. (b) Give any joumal entries that should be made as a result of the bank reconciliation Question 2 (a) Harmony Company Bank Reconciliation March 31,2015 (b)