Answered step by step

Verified Expert Solution

Question

1 Approved Answer

The answer must be 0.89207% Please answer without Excel or Chat GPT! Isaac entered into a two-year swap with semiannual settlements and level notional amount

The answer must be 0.89207%

Please answer without Excel or Chat GPT!

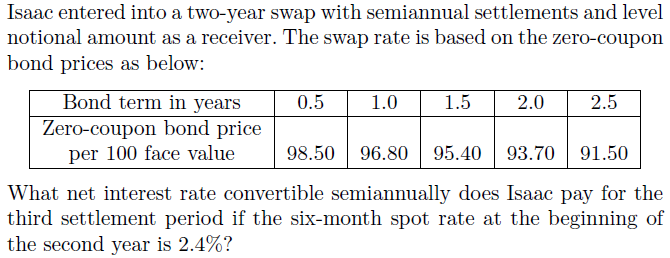

Isaac entered into a two-year swap with semiannual settlements and level notional amount as a receiver. The swap rate is based on the zero-coupon bond prices as below: What net interest rate convertible semiannually does Isaac pay for the third settlement period if the six-month spot rate at the beginning of the second year is 2.4% ? Isaac entered into a two-year swap with semiannual settlements and level notional amount as a receiver. The swap rate is based on the zero-coupon bond prices as below: What net interest rate convertible semiannually does Isaac pay for the third settlement period if the six-month spot rate at the beginning of the second year is 2.4%Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Cryptocurrency Trading A Beginner S Guide To Cryptocurrency Trading Strategies

Authors: Hollis Slough

1st Edition

979-8354901968