Answered step by step

Verified Expert Solution

Question

1 Approved Answer

The appendix at the end contains the prices of a set of Google Call options. They have 59 days to maturity (T=58 days). Suppose

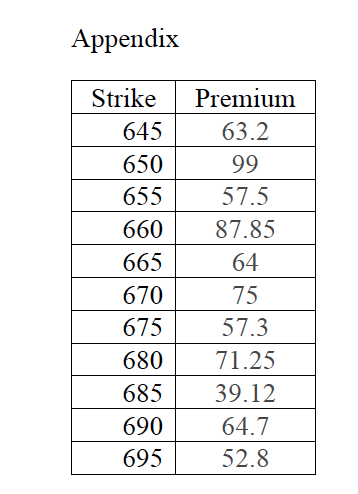

The appendix at the end contains the prices of a set of Google Call options. They have 59 days to maturity (T=58 days). Suppose the risk-free rate is 0% per annum. The stock price of Google was 738.06. Assume all the options are European Options. a. Find two options for which the low boundary condition DOES NOT Hold and thus arbitrage opportunities exist. Calculate the minimum arbitrage profit. Option 1: Strike Option 2: Strike In general, if a call option does not satisfy the low boundary condition, we ; Profit per Contract ; Profit Contract per _(buy/sell) the option, _(long/short) the stock, and (lend/Borrow) to realize arbitrage profit. b. Find three pairs of options for which the relationship C(K1) > C(K2) for K2 > K1 DOES NOT HOLD and thus arbitrage opportunities exist. Calculate the minimum arbitrage profit. ; Minimum Profit ; Minimum Profit ; Minimum Profit Pair 1: Strikes and Pair 2: Strikes and Pair 3: Strikes and In general, if the relationship does not hold, we _(buy/sell) the option with _(buy/sell) the option with low strike price, and high strike price, (lend/Borrow) to realize arbitrage profit. c. Find three pairs of options for which the relationship C(K,) C(K2) < K2 K1 for K2 > K, DOES NOT HOLD and thus arbitrage opportunities exist. Calculate the minimum arbitrage profit. Pair 1: Strikes and ; Minimum Profit Pair 2: Strikes and Minimum Profit Pair 3: Strikes and ; Minimum Profit In general, if the relationship does not hold, we high strike price, _(buy/sell) the option with _(buy/sell) the option with low strike price, and (lend/Borrow) to realize arbitrage profit. Appendix Strike Premium 645 63.2 650 99 655 57.5 660 87.85 665 64 670 75 675 57.3 680 71.25 685 39.12 690 64.7 695 52.8

Step by Step Solution

★★★★★

3.45 Rating (148 Votes )

There are 3 Steps involved in it

Step: 1

For call options boundary condition is Where Co is call option price So is underlying price and X is ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Personal Finance An Integrated Planning Approach

Authors: Ralph R Frasca

8th edition

136063039, 978-0136063032