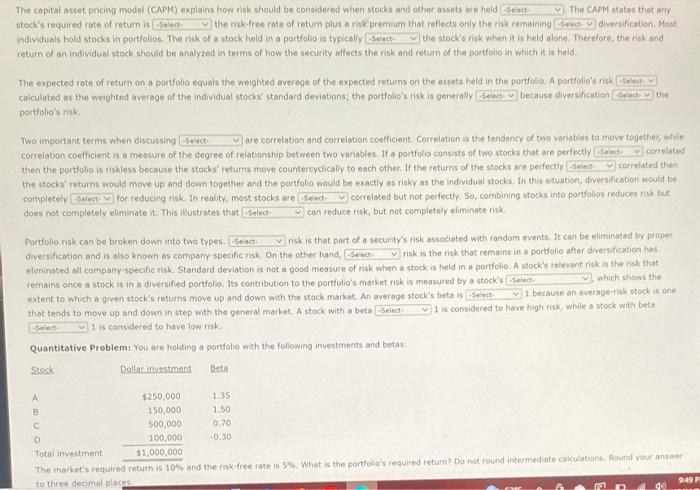

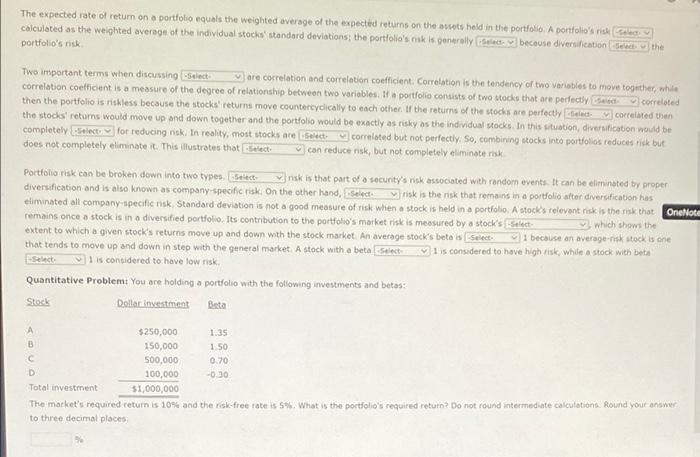

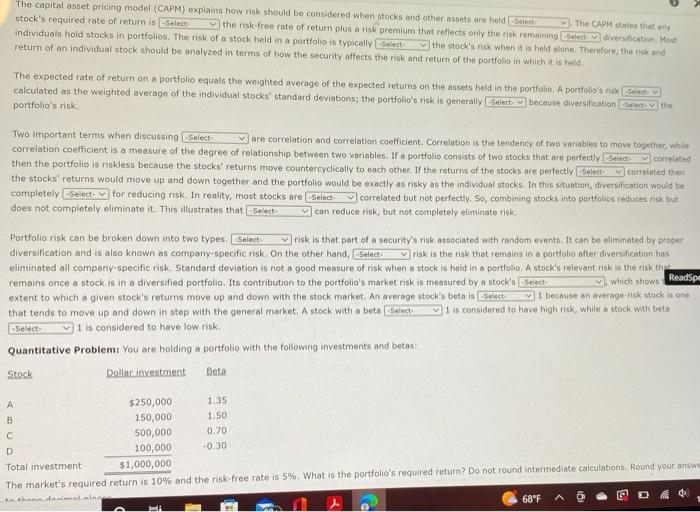

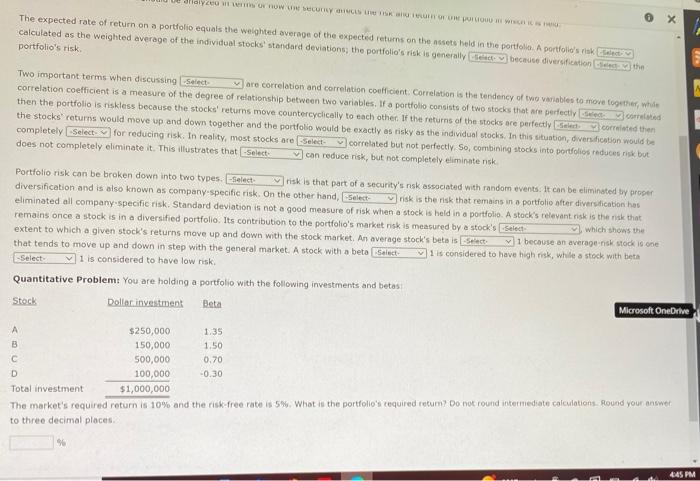

The copital astet pricing model (CAPM) explains how riok should be considered when stocks and other assets ace held stock's required rate of return is states that any _ the risk-free rate of return plus o fisk premium that reflects only the risk remaining stock's required rate of return is diversification. M. individuals hold stocks in portfolios. The risk of a stock held in a porfolio is typically return of an individual stock should be aralyzed in terms of how the security atfects the risk and return of the portfolio in which it is held. The expected rate of return on a portfolio equals the weighted average of the expected returns on the astets held in the portfoso. A portfolig's risk calculated as the weighted average of the individual stocks' standard deviations; the portfolio's tisk is generally because diversification portfolia's risk. Two impoctant terms when discussing are correlation and correlation coefficient Correlation is the tendency of two variables to moye together, while correlation coefficient is a measure of the degree of relationship between two variables. If a portfolio consists of two stocks that are perfectiy then the portiolio is riskless becouse the stocks' returns move countercyclically to eech other. If the returns of the stocks are perfectly the stocks' returns would move up and down together and the portfolio would be exactiy as risky as the ind widual stocks. In this situation, diversification would be the stocks' returns would move up and down together and the portfolio would be exactiy as risky as the ind vidual stocks. In this mituation, diverisfication would bei completely for reducing risk. In reality, most stocks are does not completely eliminate it. This illustrates thot con reduce risk, but not completely eliminate risk. Portfolio nigk can be broken down unto two types. risk is that part of a security's risk associated with random events. It can be eliminoted by propec diversificotion and is aleo known as company-specific risk. On the other hand, risk is the risk thet remains in a portifio after diversification has eliminated all company-specific risk. Standard deviaton is not a good measure of risk when a stock is held in a portfolio. A stock't relievont risk is the risk that remains once a stock is in a diversified portiolio. Its contribution to the portfolio's matket risk is meawured by a stock's Which shows the ragerrisk stock is one? extent to which a given stock's returne move up and down with the stock market. An average stock's beta is 1 because an averagerrisk stock is high rick, while o stock with bete that tends to move up and down in step with the general market. A stock. with a beta 1 is considered to have high rick, while a stock with beto 1 is considered to have low risk. Quantitative Problem: You are holding o portfolio with the following investments and betas: The expected rate of return on a portfolio equals the weighted average of the expected teturns on the ascots held in the portfolio. A portiolio's risk calculated as the weighted average of the individual stocks' standard deviations; the portfolio's riak is generelly portfolio's risk Two important terms when discussing are correlation and correlation coefficient, Correlation is the tendency of two variabies to mave tagither, white correlabon coefficent is a measure of the degree of relationship between two voriables. If a portfolio consists of two stocks that are perfectly completely for reducing niski In reality, mo does not completely eliminate it. This illustrotes that can reduce risk, but not completely eliminate risk Portfolio risk can be broken down into two types. nsk is that part of a socurity's risk associated with random events. It can be eliminsted ty proper diversification and is also known as company-specific risk On the other hand, risk is the nsk that remains in a portfolio after diversfication has eliminated all company-specific risk, Standard deviation is not a good measure of risk when a stock is held in a portfolso, A stocks reievant rick is the risk that, remains once a stock is in a diversified portfolvo. Its contribution to the portfolo's market risk is meacured by a stock's which shows the extent to which a given stock's returns move up and down with the stock market. An average stock's bete's that tends to move up and down in step with the general market. A stock with a beta 1 is considered to have high risk, while a stock with beta 1 is considered to have low risk. Quantitative Problemy You are holding a portfolio with the following investments and betas: The market's required return is 10% and the risk-free rate is 5%. What is the portiolig's required return? Do not round intermediate calculationa. Roind your answer to three decimal places; stock's required rate of return is return of an individual stock should be analyzed in terms of how the security affects the risk and return of the portfolio in which it is held. The expected rate of return an a portfolio equals the weighted average of the expected returns on the assets held in the portfolio, A portfolio's risk calculated as the weighted average of the individual stocks' standard deviations; the portfolio's risk is getierally portfolio's riski. Two important terms when discussing are correlation and correlation coefficient, Correlation is the tendency of two vanables to move together, while correlation coefficient is a measure of the degree of relationship between two variables. If a portfolio consists of two stocks that are perfectly then the portfolio is riskless because the stocks' returns move countercyclically to each other. If the returns of the stocks are perfectiy ' correloted then the stocks' returns would move up and down together and the portfolio would be exactly as risky as the individual stocks. In this situation, diversification would be completely for reducing risk. In reality, most stocks are can reduce risk, but not completely eliminate riok, does not completely eliminate it. This illustrates that Portfolio risk can be broken down into two types. risk is that part of a security's risk associated with randorn events. it cari be eliminated by proper diversification and is also known as company-specific risk. On the other hand, risk is the risk that remains in a portfolio after diversication has eliminated all company-specific risk. Standard deviation is not a good measure of risk when a stock is held in a portfolio. A stock's relevant risk is the risk th-. remains once a stock is in a diversified portfolio. Its contribution to the portfolio's market risk is measured by a stock's which shows 1 extent to which a given stock's returns move up and down with the stock market. An average stock's beta is that tends to move up and down in step with the general market. A stock with a beta 1 is considered to have high fisk, while a stock with beta 1 is considered to have low risk. Ouantitative Problem: You are holding a portfolio with the foliowing investments and betas: The expected rate of return on a portiolio equals the welghted average of the axpected returns on the nssets held in the dortiolita. A portfolio's riak calculated as the weighted average of the individual stocks' standard deviations, the portfolio's risk is qenerally portfolio's risk. correlation coefficient is a measure of the degree of relationship between two variables, If a portfolio consists of two stocks that are perfectiy Portfolio risk can be broken down into two types. _risk is that part of a security's nisk assaciated with random events. it can be eliminated by proper diversification and is also known as company-specific risk. On the other hand, risk is the risk that remains in a pattfolic after diversication has eliminated all company-specific risk. Standard deviation is not a good measure of risk when a stock is held in o portfolio. A stock's releyant risk is the nisk that remains once a stock is in a diversified portfolio. Its contribution to the portfolio's market nisk is measured by a stock's Which shons the extent to which a given stock's returns mave up and down with the stock market. An average stock's beta is that tends to move up and down in step with the general market. A stock with a beto 1 is considered to have high risk, while s steck, with beta 1 is considered to have low risk. Quantitative Problem: You are holding a portfolio with the following investments and betas: The market's required return is 10% and the risk-free rate is 5%. What is the portfolio's cequired retum? Do noc round intermediate calculations. gound your answer: to three decimal places