Answered step by step

Verified Expert Solution

Question

1 Approved Answer

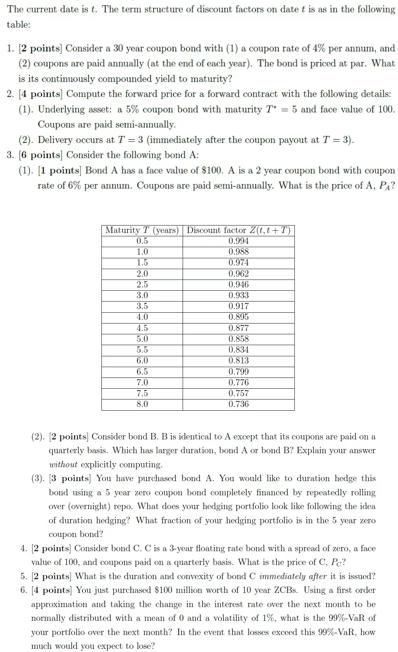

The current date is t. The term structure of discount factors on date t is as in the following table: 1. [2 points] Consider

The current date is t. The term structure of discount factors on date t is as in the following table: 1. [2 points] Consider a 30 year coupon bond with (1) a coupon rate of 4% per annum, and (2) coupons are paid annually (at the end of each year). The bond is priced at par. What is its continuously compounded yield to maturity? 2. [4 points] Compute the forward price for a forward contract with the following details: (1). Underlying asset: a 5% coupon bond with maturity T5 and face value of 100. Coupons are paid semi-annually. (2). Delivery occurs at T = 3 (immediately after the coupon payout at T = 3). 3. (6 points] Consider the following bond A: (1). [1 points] Bond A has a face value of $100. A is a 2 year coupon bond with coupon rate of 6% per annum. Coupons are paid semi-annually. What is the price of A. PA? Maturity T (years) Discount factor 2(t,1+1) 0.5 0.994 1.0 0.988 2.0 2.5 3.0 3.5 4.0 4.5 5.0 5.5 6.5 7.0 7.5 8.0 0,962 0.946 0.933 0.917 0.805 0.877 0.858 0.834 0.813 0.799 0.776 0.757 0.736 (2). 2 PHI Consider bond B. B is identical to A except that its coupons are paid on a quarterly basis. Which has larger duration, bond A or bond B7 Explain your answer without explicitly computing. (3). 3 points) You have purchased bond A. You would like to duration hodge this bond using a 5 year zero coupon bond completely financed by repeatedly rolling over (overnight) repo. What does your bodging portfolio look like following the idea of duration hedging? What fraction of your hedging portfolio is in the 5 year zero coupon bond? 4. [2 points) Consider bond C. C is a 3-year floating rate bond with a spread of zero, a face value of 100, and coupons paid on a quarterly basis. What is the price of C. Pe? 5. [2 points] What is the duration and convexity of bond C immediately after it is issued? 6. [4 points] You just purchased $100 million worth of 10 year ZCBs. Using a first order approximation and taking the change in the interest rate over the next month to be normally distributed with a mean of 0 and a volatility of 1%, what is the 99%-VaR of your portfolio over the next month? In the event that losses exceed this 99%-VaR, how much would you expect to lose?

Step by Step Solution

★★★★★

3.49 Rating (146 Votes )

There are 3 Steps involved in it

Step: 1

Answers 1 Continuously compounded yield to maturity The continuously compounded yield to maturity YTM can be calculated using the following formula P C eYTM T 1 eYTM T where P is the bond price par va...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Income Tax Fundamentals 2013

Authors: Gerald E. Whittenburg, Martha Altus Buller, Steven L Gill

31st Edition

1111972516, 978-1285586618, 1285586611, 978-1285613109, 978-1111972516