Answered step by step

Verified Expert Solution

Question

1 Approved Answer

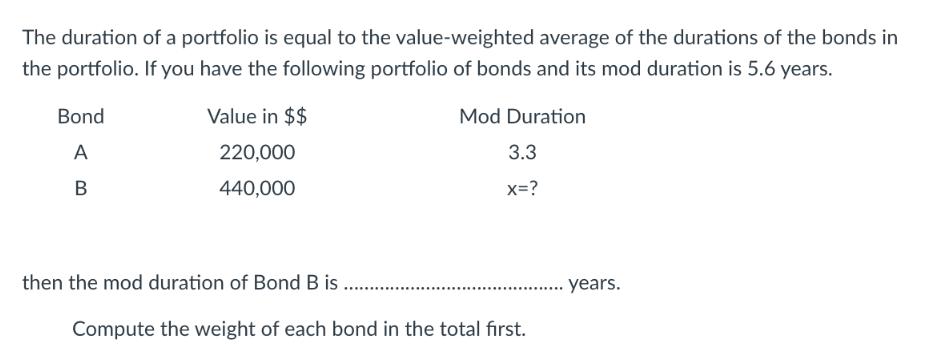

The duration of a portfolio is equal to the value-weighted average of the durations of the bonds in the portfolio. If you have the

The duration of a portfolio is equal to the value-weighted average of the durations of the bonds in the portfolio. If you have the following portfolio of bonds and its mod duration is 5.6 years. Mod Duration 3.3 X=? Bond A B Value in $$ 220,000 440,000 then the mod duration of Bond B is Compute the weight of each bond in the total first. years.

Step by Step Solution

★★★★★

3.47 Rating (163 Votes )

There are 3 Steps involved in it

Step: 1

To compute the weight of each bond in the portfolio we need to divide the value of each bond by the ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Principles of Corporate Finance

Authors: Richard Brealey, Stewart Myers, Franklin Allen

13th edition

1260013901, 1260565553, 978-1260013900