Answered step by step

Verified Expert Solution

Question

1 Approved Answer

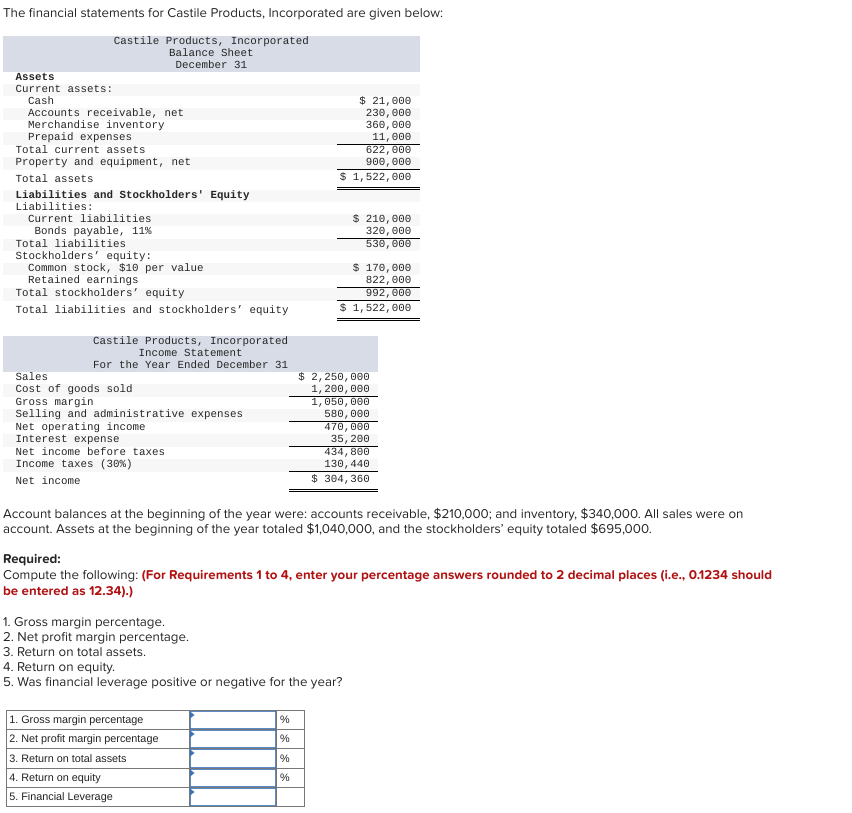

The financial statements for Castile Products, Incorporated are given below: Account balances at the beginning of the year were: accounts receivable, $210,000; and inventory, $340,000.

The financial statements for Castile Products, Incorporated are given below: Account balances at the beginning of the year were: accounts receivable, $210,000; and inventory, $340,000. All sales were on account. Assets at the beginning of the year totaled $1,040,000, and the stockholders' equity totaled $695,000. Required: Compute the following: (For Requirements 1 to 4, enter your percentage answers rounded to 2 decimal places (i.e., 0.1234 should be entered as 12.34).) 1. Gross margin percentage. 2. Net profit margin percentage. 3. Return on total assets. 4. Return on equity. 5. Was financial leverage positive or negative for the year

The financial statements for Castile Products, Incorporated are given below: Account balances at the beginning of the year were: accounts receivable, $210,000; and inventory, $340,000. All sales were on account. Assets at the beginning of the year totaled $1,040,000, and the stockholders' equity totaled $695,000. Required: Compute the following: (For Requirements 1 to 4, enter your percentage answers rounded to 2 decimal places (i.e., 0.1234 should be entered as 12.34).) 1. Gross margin percentage. 2. Net profit margin percentage. 3. Return on total assets. 4. Return on equity. 5. Was financial leverage positive or negative for the year Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Horngren S Financial And Managerial Accounting The Managerial Chapters

Authors: Tracie L. Miller-Nobles ,Brenda L. Mattison ,Ella Mae Matsumura

4th Edition

0133255433, 978-0133255430