Answered step by step

Verified Expert Solution

Question

1 Approved Answer

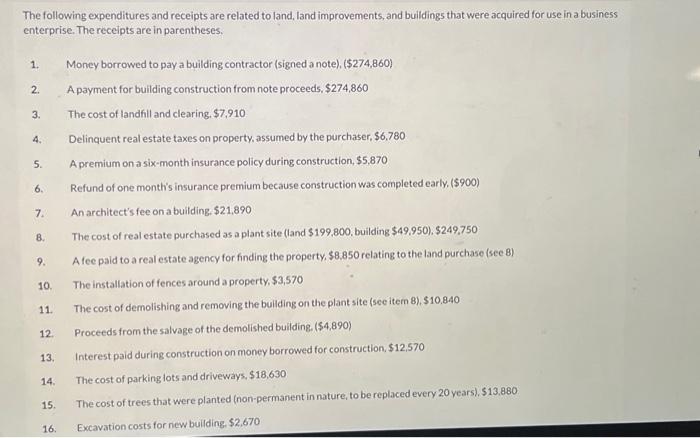

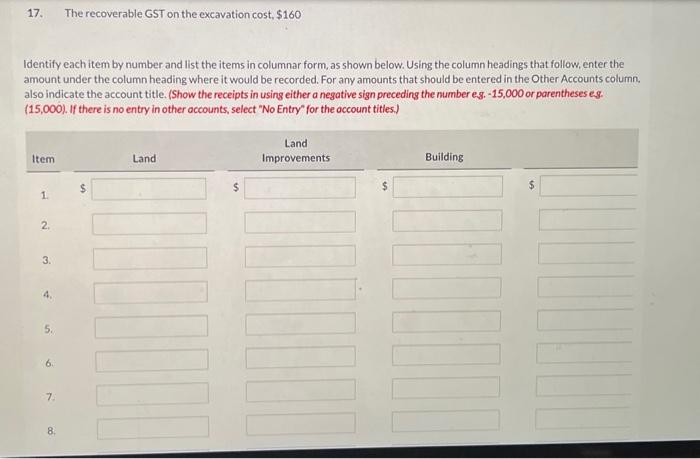

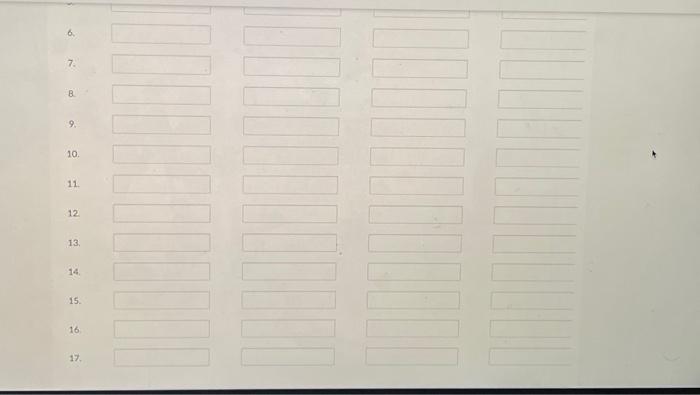

The following expenditures and receipts are related to land, land improvements, and buildings that were acquired for use in a business enterprise. The receipts are

The following expenditures and receipts are related to land, land improvements, and buildings that were acquired for use in a business enterprise. The receipts are in parentheses. 1. Money borrowed to pay a building contractor (signed a note), ($274,860) 2. A payment for building construction from note proceeds, $274,860 3. The cost of landfill and clearing, $7,910 4. Delinquent real estate taxes on property, assumed by the purchaser, $6,780 5. A premium on a six-month insurance policy during construction, $5,870 6. Refund of one month's insurance premium because construction was completed early. ($900) 7. An architect's fee on a building. $21,890 8. The cost of real estate purchased as a plant site (land $199,800, building $49,950),$249,750 9. A fee paid to a real estate agency for finding the property, $8,850 relating to the land purchase (see 8 ) 10. The installation of fences around a property, $3,570 11. The cost of demolishing and removing the buliding on the plant site (see item 8 ), $10,840 12. Proceeds from the salvage of the demolished building. ($4,890) 13. Interest paid during construction on money borrowed for construction, $12,570 14. The cost of parking lots and driveways, $18,630 15. The cost of trees that were planted (non-permanent in nature, to be replaced every 20 years), $13.880 16. Excavation costs for new building $2,670 17. The recoverable GST on the excavation cost, $160 Identify each item by number and list the items in columnar form, as shown below. Using the column headings that follow, enter the amount under the column heading where it would be recorded. For any amounts that should be entered in the Other Accounts column, also indicate the account title. (Show the receipts in using either a negative sign preceding the number es. 15,000 or parentheses es. (15,000). If there is no entry in other occounts, select "No Entry" for the occount titles.)

The following expenditures and receipts are related to land, land improvements, and buildings that were acquired for use in a business enterprise. The receipts are in parentheses. 1. Money borrowed to pay a building contractor (signed a note), ($274,860) 2. A payment for building construction from note proceeds, $274,860 3. The cost of landfill and clearing, $7,910 4. Delinquent real estate taxes on property, assumed by the purchaser, $6,780 5. A premium on a six-month insurance policy during construction, $5,870 6. Refund of one month's insurance premium because construction was completed early. ($900) 7. An architect's fee on a building. $21,890 8. The cost of real estate purchased as a plant site (land $199,800, building $49,950),$249,750 9. A fee paid to a real estate agency for finding the property, $8,850 relating to the land purchase (see 8 ) 10. The installation of fences around a property, $3,570 11. The cost of demolishing and removing the buliding on the plant site (see item 8 ), $10,840 12. Proceeds from the salvage of the demolished building. ($4,890) 13. Interest paid during construction on money borrowed for construction, $12,570 14. The cost of parking lots and driveways, $18,630 15. The cost of trees that were planted (non-permanent in nature, to be replaced every 20 years), $13.880 16. Excavation costs for new building $2,670 17. The recoverable GST on the excavation cost, $160 Identify each item by number and list the items in columnar form, as shown below. Using the column headings that follow, enter the amount under the column heading where it would be recorded. For any amounts that should be entered in the Other Accounts column, also indicate the account title. (Show the receipts in using either a negative sign preceding the number es. 15,000 or parentheses es. (15,000). If there is no entry in other occounts, select "No Entry" for the occount titles.)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Management And Compliance Audit A Complete Guide

Authors: Gerardus Blokdyk

2020 Edition

0655927727, 978-0655927723