Answered step by step

Verified Expert Solution

Question

1 Approved Answer

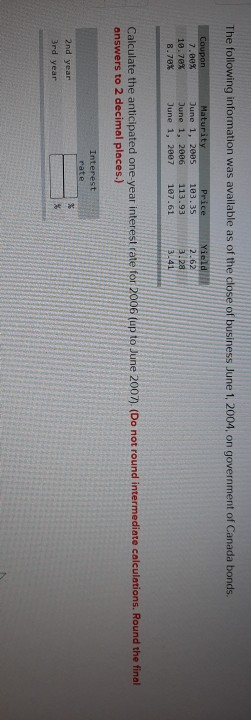

The following information was available as of the close of business June 1, 2004, on government of Canada bonds. Coupon 7.00% 10.70% 8.78% Maturity June

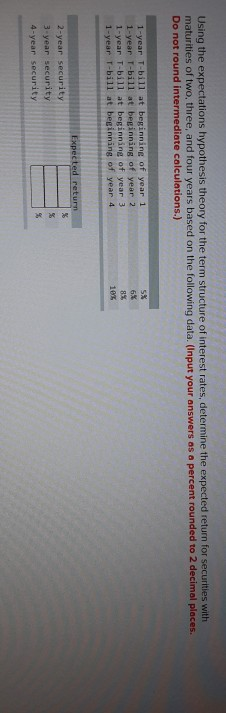

The following information was available as of the close of business June 1, 2004, on government of Canada bonds. Coupon 7.00% 10.70% 8.78% Maturity June 1, 2005 June 1, 2006 June 1, 2007 Price 103.35 113.93 107.61 Yield 2.62 3.28 3.41 Calculate the anticipated one year interest rate for 2006 (up to June 2007). (Do not round intermediate calculations. Round the final answers to 2 decimal places.) Interest rate 2nd year 3rd year Using the expectations hypothesis theory for the term structure of interest rates, determine the expected return for securities with maturities of two, three, and four years based on the following data. (Input your answers as a percent rounded to 2 decimal places. Do not round intermediate calculations.) 1-year T-bill at beginning of year 1 1-year T-bill at beginning of year 2 1-year T-bill at beginning of year 3 1-year T-bill at beginning of year 4 5% 6% 8% 10% Expected return % % 2-year security 3-year security 4-year security

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Understanding Decentralized Finance How DeFi Is Changing The Future Of Money

Authors: Rhian Lewis

1st Edition

1398609390, 978-1398609396