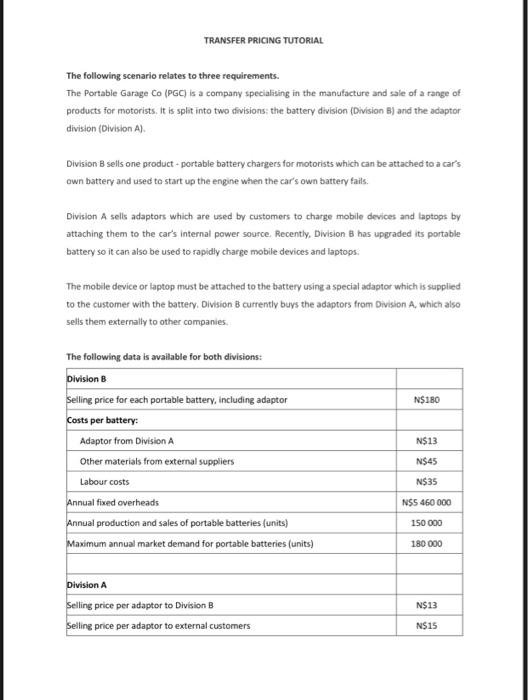

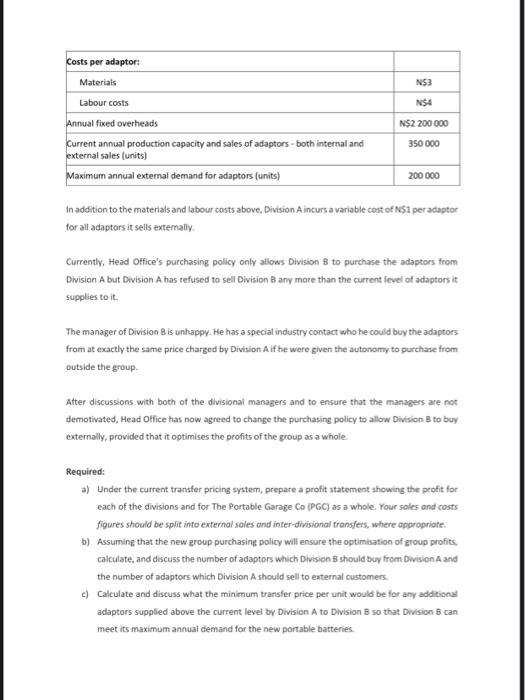

The following scenario relates to three requirements. The Portable Garage Co (PGC) is a company specialising in the manufacture and sale of a range of products for motorists. It is split into two divisions: the battery division (Division B) and the adaptor division (Oivision A ). Division B sells one product - portable battery chargers for motorists which can be attached to a car's own battery and used to start up the engine when the car's own battery fails: Division A sells adaptors which are used by customers to charge mobile devices and laptops by attaching them to the car's internal power source. Recently, Division B has upgraded its portable battery so it can also be used to rapidly charge mobile devices and laptops. The mobile device or laptop must be attached to the battery using a special adaptor which is supplied to the customer with the battery. Division B currently buys the adaptors from Division A, which also sells them externally to other companies. The following data is available for both divisions: In addition to the materials and labour costs above. Division A incurs a variable cost of NS1 per adaptor for all adaptors it sells extemally. Currently, Head Office's purchasing policy only allows Division B to purchase the adaptors from Division A but Division A has refused to sell Division B any more than the current level of adaptors it supplies to it. The manager of Division 8 is unhappy. He has a special industry contact who he could buy the adaptors from at exactly the same price charged by Division A if he were given the autonomy to purchase from outside the group. After discussions with both of the divisional managers and to ensure that the managers are nor demotivated, Head Office has now agreed to change the purchasing policy to allow Division 8 to buy externally, provided that it optimises the profits of the group as a whole. Required: a) Under the current transfer pricing system, prepare a profit statement showing the peofit for each of the divisions and for The Portable Garage Ce(PGC) as a whole. Your sales and costs figures should be spit into external sales and inter-divisional transfers, where oppropriote. b) Assuming that the new group purchasing policy will ensure the optimisation of group profits, calculate, and discuss the number of adaptors which Division B should boy from Division A and the number of adaptors which Division A should sell to external customers. c) Calculate and discuss what the minimum transfer price per unit would be for any additional adaptors suppsied above the current level by Division A to Division B so that Division B can meet its maximum annual demand for the new portable batteries