Answered step by step

Verified Expert Solution

Question

1 Approved Answer

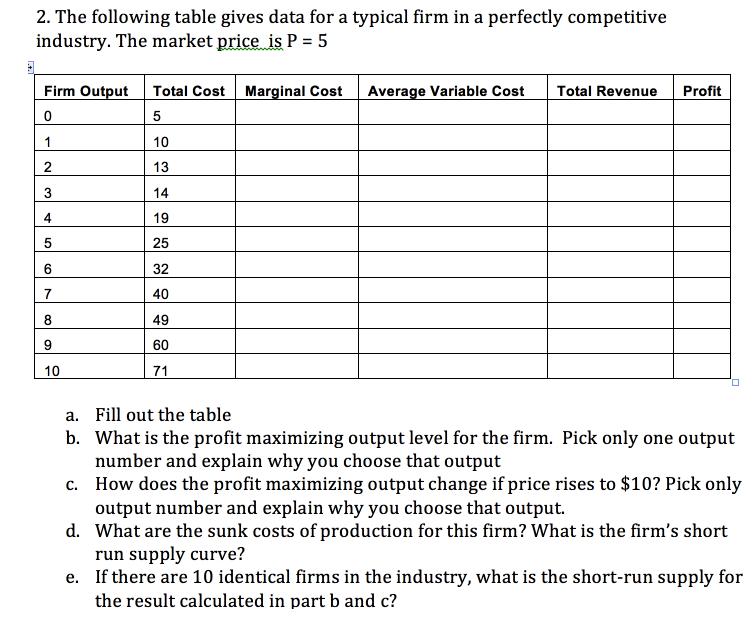

The following table gives data for a typical firm in a perfectly competitive industry. The market price is P = 5 Firm Output Total

The following table gives data for a typical firm in a perfectly competitive industry. The market price is P = 5 Firm Output Total Cost Marginal Cost 0 5 1 2 3 4 5 6 7 8 9 10 10 13 14 19 25 32 40 49 60 71 a. Fill out the table b. Average Variable Cost Total Revenue Profit What is the profit maximizing output level for the firm. Pick only one output number and explain why you choose that output c. How does the profit maximizing output change if price rises to $10? Pick only output number and explain why you choose that output. d. What are the sunk costs of production for this firm? What is the firm's short run supply curve? e. If there are 10 identical firms in the industry, what is the short-run supply for the result calculated in part b and c?

Step by Step Solution

★★★★★

3.38 Rating (160 Votes )

There are 3 Steps involved in it

Step: 1

The detailed ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Statistics

Authors: Robert S. Witte, John S. Witte

11th Edition

1119254515, 978-1119254515