Answered step by step

Verified Expert Solution

Question

1 Approved Answer

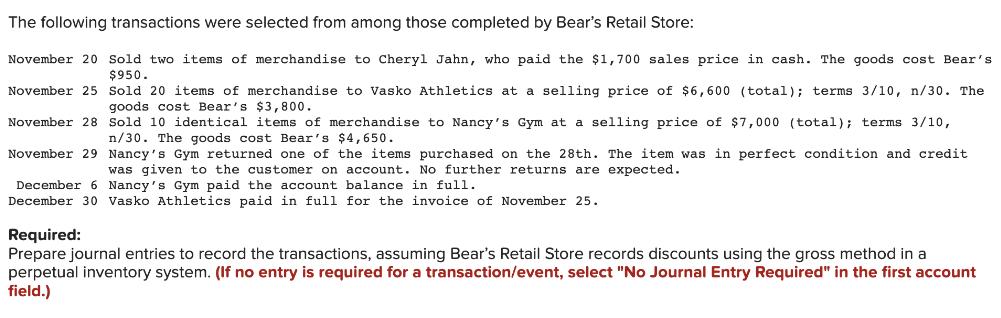

The following transactions were selected from among those completed by Bear's Retail Store: November 20 Sold two items of merchandise to Cheryl Jahn, who

The following transactions were selected from among those completed by Bear's Retail Store: November 20 Sold two items of merchandise to Cheryl Jahn, who paid the $1,700 sales price in cash. The goods cost Bear's $950. November 25 Sold 20 items of merchandise to Vasko Athletics at a selling price of $6,600 (total); terms 3/10, n/30. The goods cost Bear's $3,800. November 28 Sold 10 identical items of merchandise to Nancy's Gym at a selling price of $7,000 (total); terms 3/10, n/30. The goods cost Bear's $4,650. November 29 Nancy's Gym returned one of the items purchased on the 28th. The item was in perfect condition and credit was given to the customer on account. No further returns are expected. December 6 Nancy's Gym paid the account balance in full. December 30 Vasko Athletics paid in full for the invoice of November 25. Required: Prepare journal entries to record the transactions, assuming Bear's Retail Store records discounts using the gross method in a perpetual inventory system. (If no entry is required for a transaction/event, select "No Journal Entry Required" in the first account field.) Journal entry worksheet 2 1 Record the sale of merchandise for $1,700 cash to Cheryl Jahn. 3 4 5 6 7 8 9 10 Note: Enter debits before credits. Date November 20 Record entry General Journal Clear entry Debit Credit View general journal

Step by Step Solution

★★★★★

3.33 Rating (150 Votes )

There are 3 Steps involved in it

Step: 1

Lets prepare the journal entries to record the transactions for Bears Retail Store using the gross m...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Accounting

Authors: Robert Libby, Patricia Libby, Daniel Short, George Kanaan, M

5th Canadian edition

9781259105692, 978-1259103285