Answered step by step

Verified Expert Solution

Question

1 Approved Answer

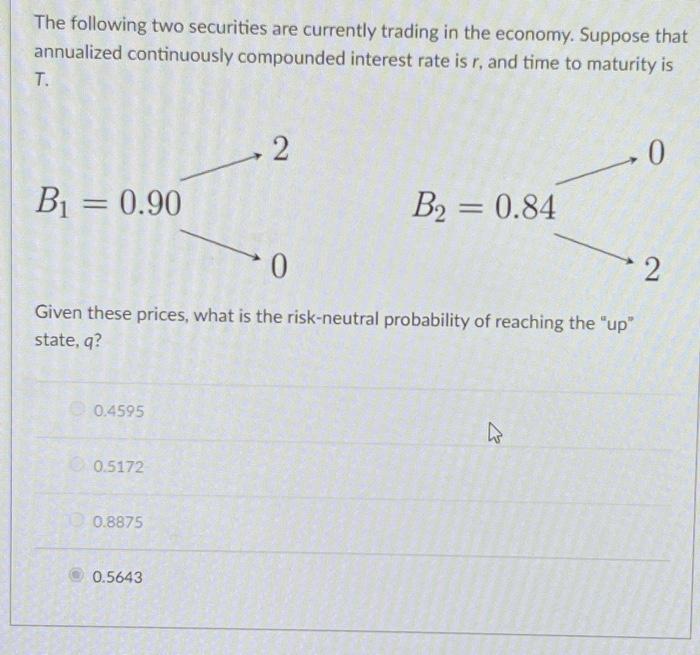

The following two securities are currently trading in the economy. Suppose that annualized continuously compounded interest rate is r, and time to maturity is T.

The following two securities are currently trading in the economy. Suppose that annualized continuously compounded interest rate is r, and time to maturity is T. B = 0.90 0.4595 0.5172 2 0 Given these prices, what is the risk-neutral probability of reaching the "up" state, q? 0.8875 2 0.5643 B = 0.84 0 4

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Risk Sharing Finance

Authors: Bakkali Mirakhor, Saad Abbas

1st Edition

3110590468, 978-3110590463