Answered step by step

Verified Expert Solution

Question

1 Approved Answer

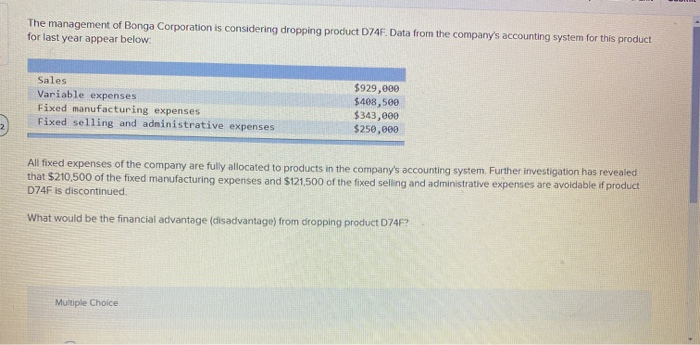

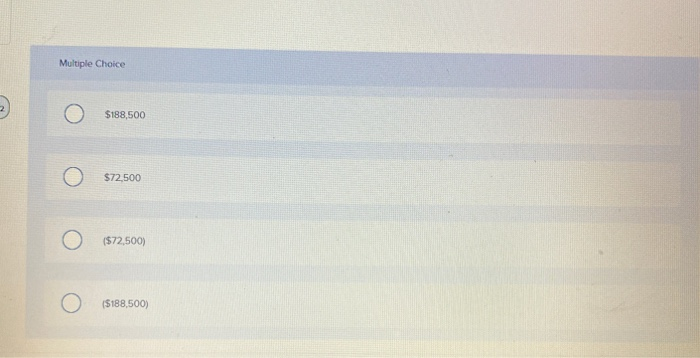

The management of Bonga Corporation is considering dropping product D74F. Data from the company's accounting system for this product for last year appear below: Sales

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Information Systems Audit In Banking Sector A Study Of SBI And ICICI Banks

Authors: C. Mallesha, M. Sulochana

1st Edition

6200254397, 978-6200254399