Question

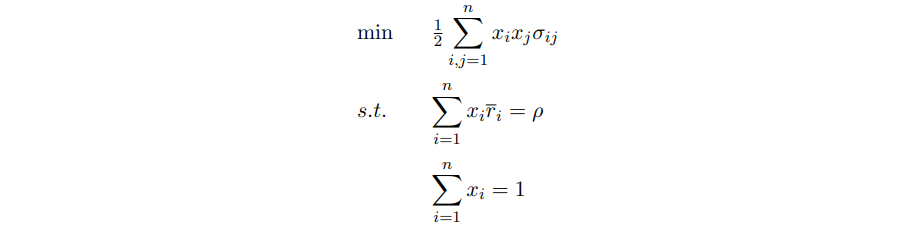

The Markowitz model, which describes portfolio optimisation in finance, is given as: (a) When n = 2, write out the Markowitz model in full, and

The Markowitz model, which describes portfolio optimisation in finance, is given as:

(a) When n = 2, write out the Markowitz model in full, and determine the Lagrangian stationary-point solution.

(b) Generalise this to determine the Lagrangian stationary-point solution when n 3.

min titj; i,j=1 s.t. i = i=1 n = 1 1=1 min titj; i,j=1 s.t. i = i=1 n = 1 1=1Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Aubrey Wilsons Marketing Audit Check Lists A Guide To Effective Marketing Resource Realization

Authors: Aubrey Wilson

1st Edition

0070845743, 978-0070845749