Answered step by step

Verified Expert Solution

Question

1 Approved Answer

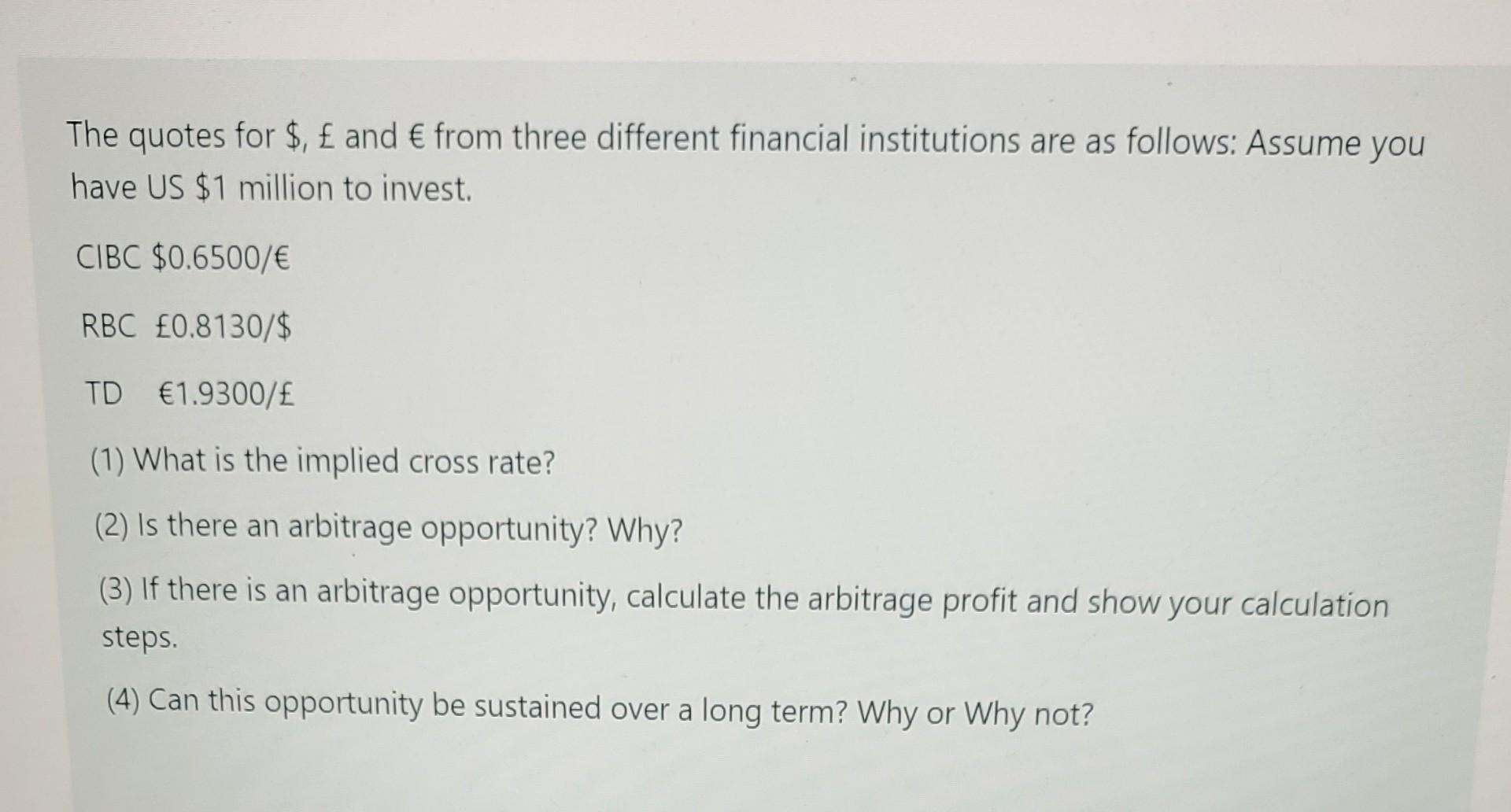

The quotes for $, and from three different financial institutions are as follows: Assume you have US $1 million to invest. CIBC$0.6500/ RBC 0.8130/$ TD

The quotes for $, and from three different financial institutions are as follows: Assume you have US $1 million to invest. CIBC$0.6500/ RBC 0.8130/$ TD 1.9300/ (1) What is the implied cross rate? (2) Is there an arbitrage opportunity? Why? (3) If there is an arbitrage opportunity, calculate the arbitrage profit and show your calculation steps. (4) Can this opportunity be sustained over a long term? Why or Why not

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance And Sustainability

Authors: Karolina Daszyńska-Żygadło, Agnieszka Bem, Bożena Ryszawska, Erika Jáki, Taťána Hajdíková

1st Edition

3030344037, 978-3030344030