Answered step by step

Verified Expert Solution

Question

1 Approved Answer

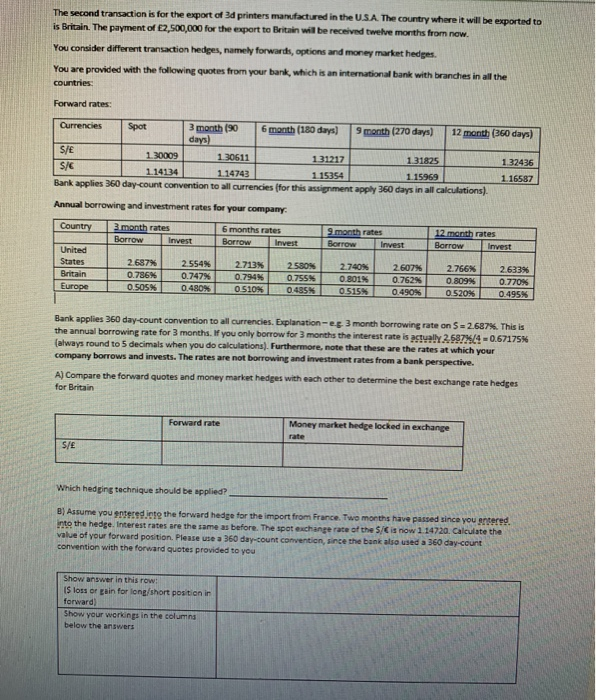

The second transaction is for the export of 3d printers manufactured in the USA The country where it will be exported to is Britain. The

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Practical Guide To Wall Street Equities And Derivatives

Authors: Matthew Tagliani

1st Edition

0470383720, 978-0470383728