Answered step by step

Verified Expert Solution

Question

1 Approved Answer

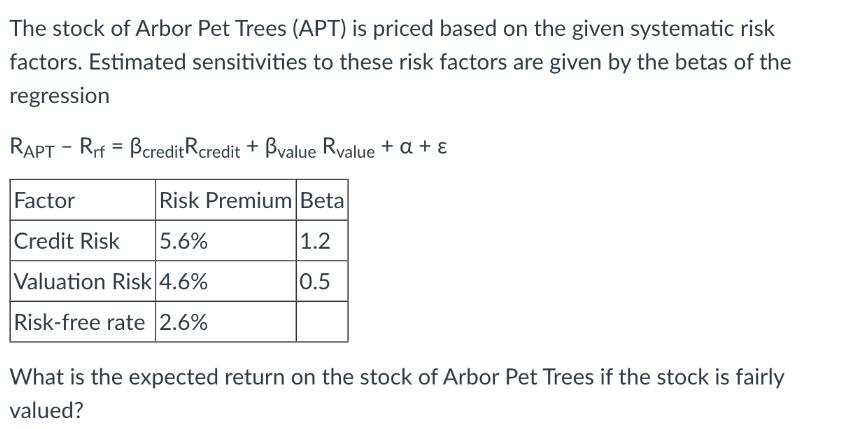

The stock of Arbor Pet Trees (APT) is priced based on the given systematic risk factors. Estimated sensitivities to these risk factors are given

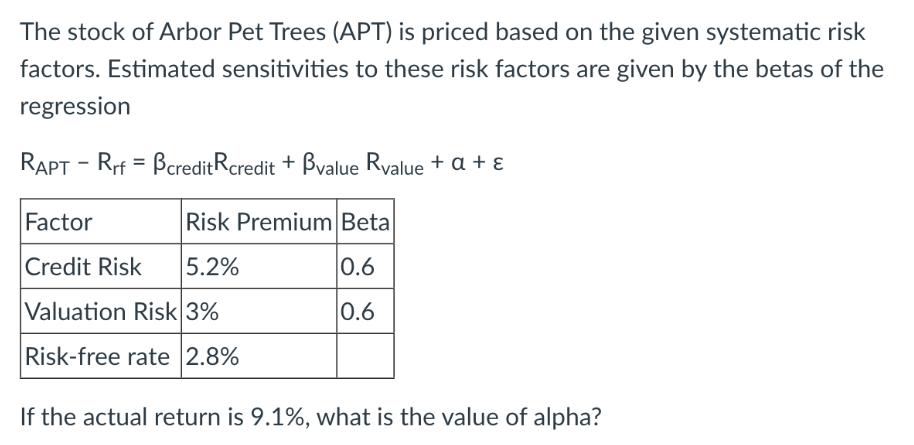

The stock of Arbor Pet Trees (APT) is priced based on the given systematic risk factors. Estimated sensitivities to these risk factors are given by the betas of the regression RAPT - Rrf = Bcredit Rcredit + value Rvalue + a + Factor Risk Premium Beta Credit Risk 5.6% 1.2 Valuation Risk 4.6% 0.5 Risk-free rate 2.6% What is the expected return on the stock of Arbor Pet Trees if the stock is fairly valued? The stock of Arbor Pet Trees (APT) is priced based on the given systematic risk factors. Estimated sensitivities to these risk factors are given by the betas of the regression RAPT - Rrf = Bcredit Rcredit + Bvalue Rvalue + a + Factor Credit Risk 5.2% Valuation Risk 3% Risk-free rate 2.8% If the actual return is 9.1%, what is the value of alpha? Risk Premium Beta 0.6 0.6

Step by Step Solution

★★★★★

3.38 Rating (148 Votes )

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Investments

Authors: Zvi Bodie, Alex Kane, Alan J. Marcus

9th Edition

73530700, 978-0073530703