Answered step by step

Verified Expert Solution

Question

1 Approved Answer

This case addresses many issues that affect insourcing/outsourcing decisions. A complex and important topic facing businesses today is whether to produce a component, assembly,

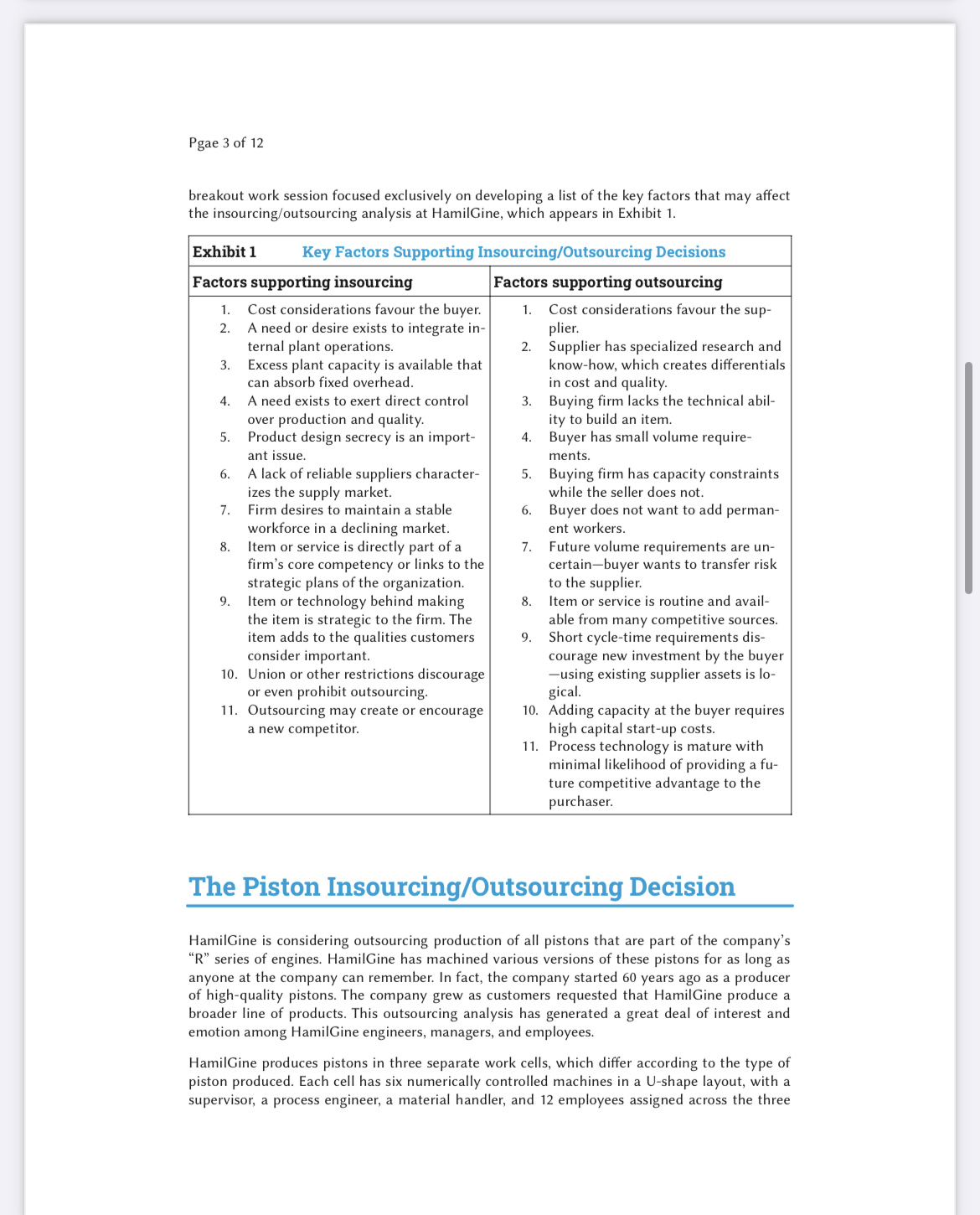

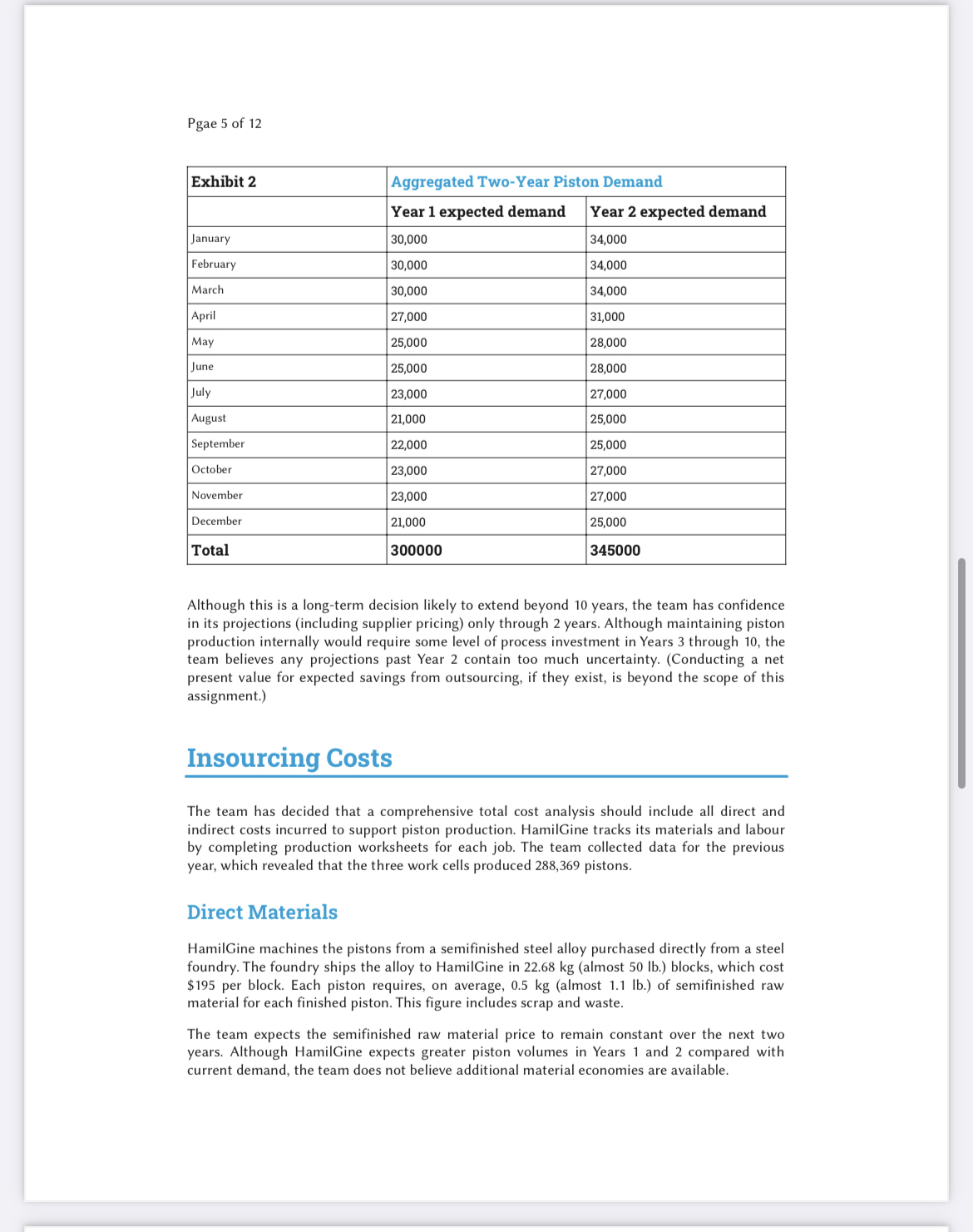

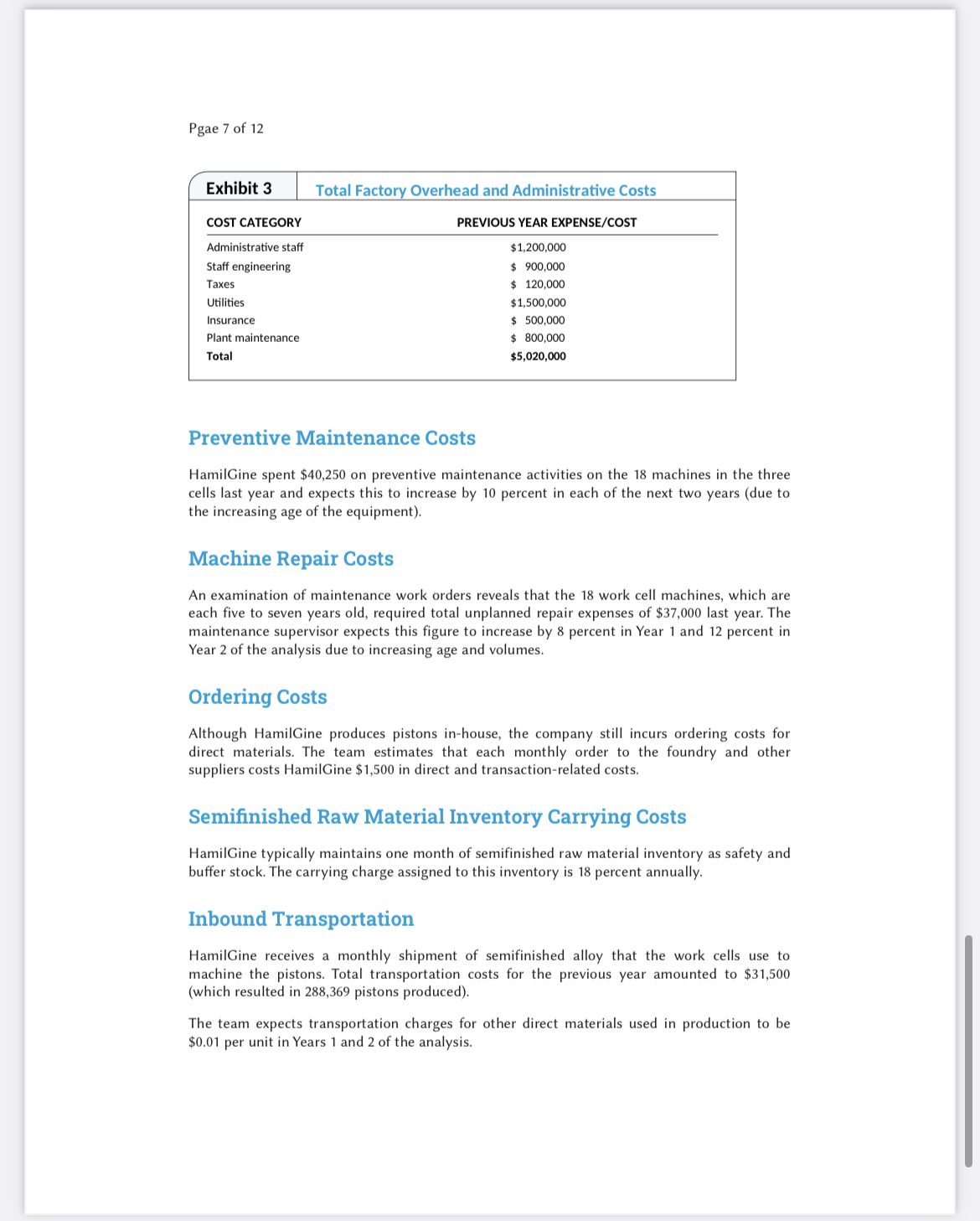

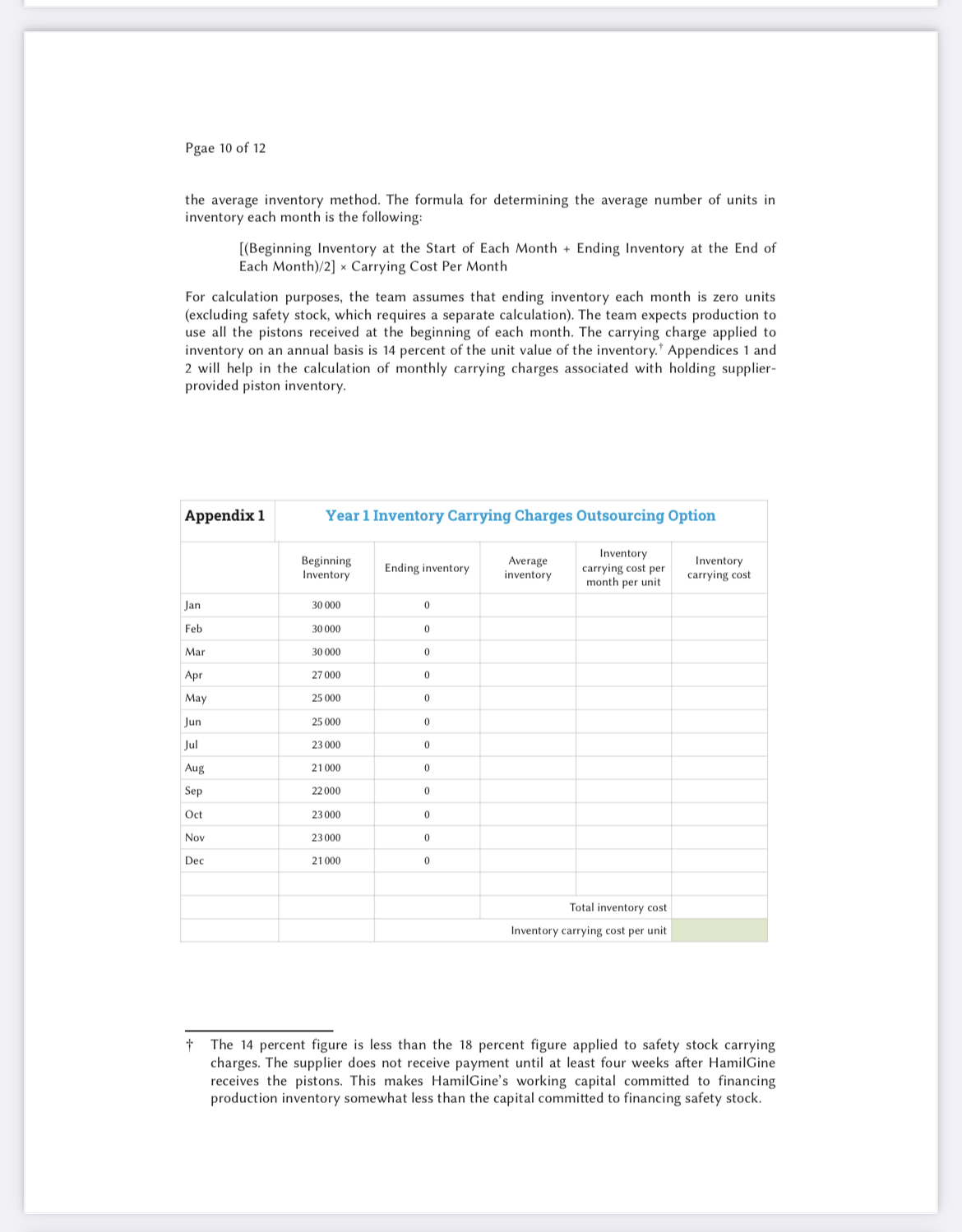

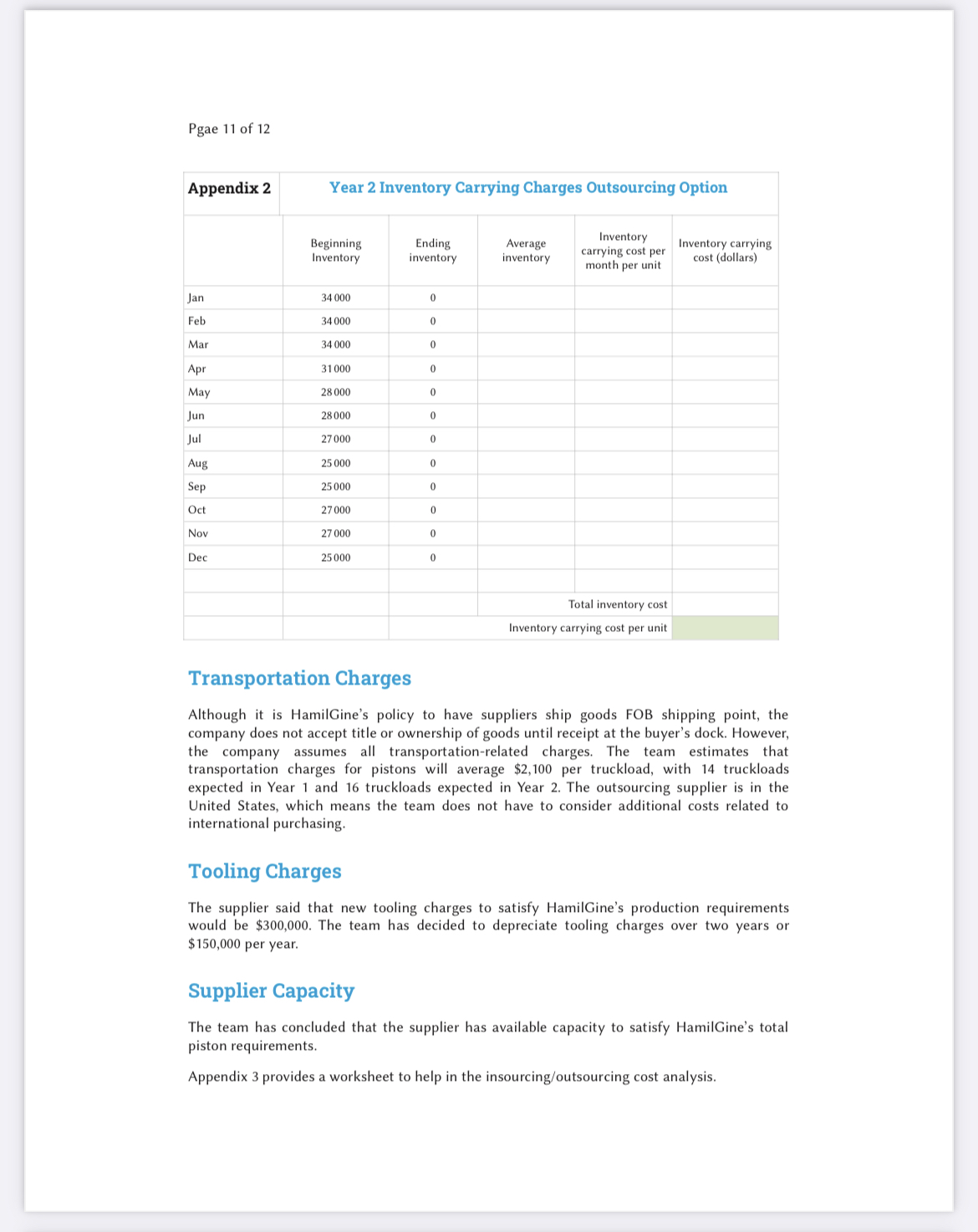

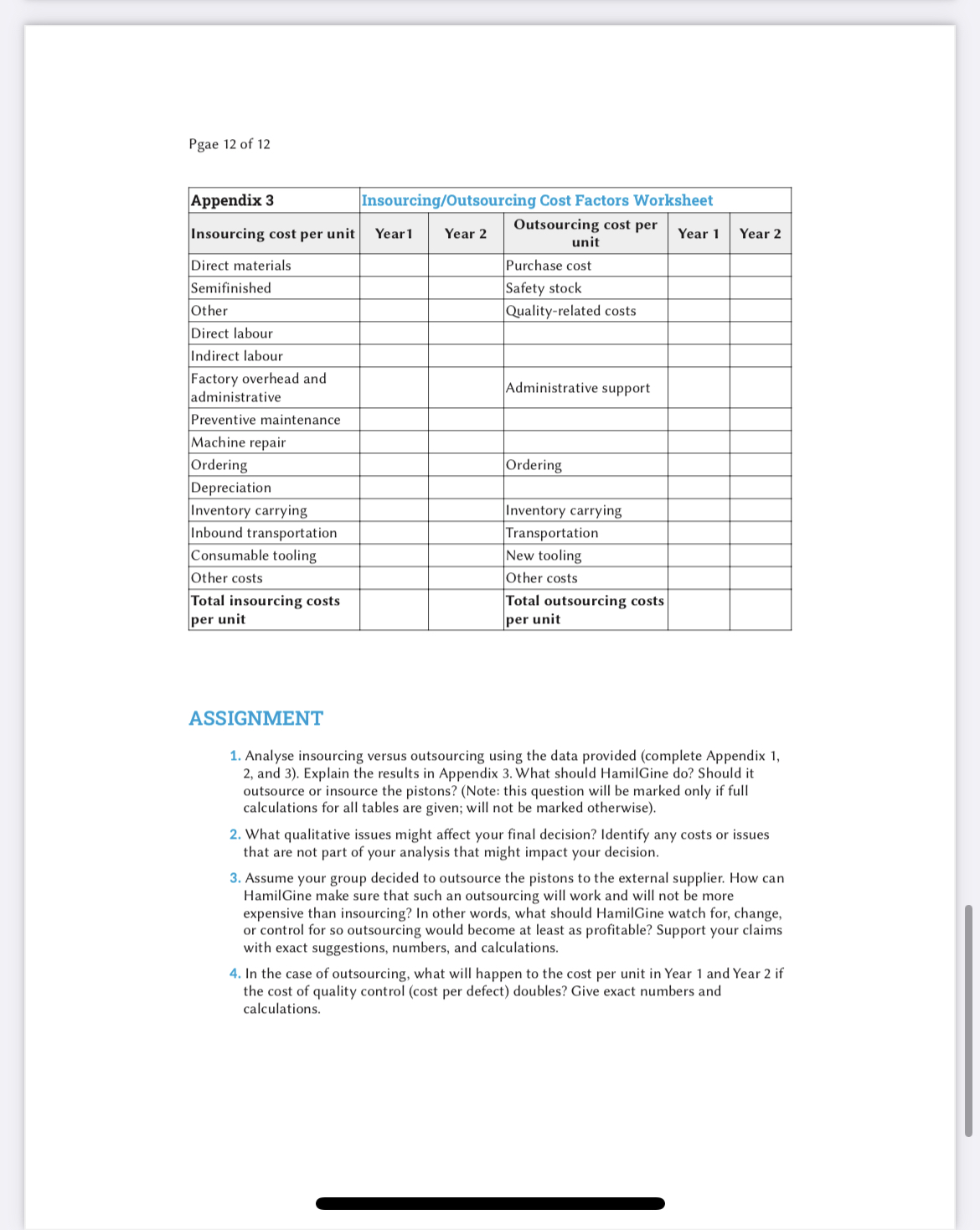

This case addresses many issues that affect insourcing/outsourcing decisions. A complex and important topic facing businesses today is whether to produce a component, assembly, or service internally (insourcing) or purchase that same component, assembly, or service from an external supplier (outsourcing). Because of the important relationship between insourcing/outsourcing and competitiveness, organizations must consider many variables when considering an insourcing/outsourcing decision. This may include a detailed examination of a firm's competency and costs, along with quality, delivery, technology, responsiveness, and continuous improvement requirements. Because of the critical nature of many insourcing/outsourcing decisions, cross-functional teams often assume responsibility for managing the decision-making process. A single functional group usually does not have the data, insight, or knowledge required to make effective strategic insourcing/outsourcing decisions. HamilGine's Insourcing/Outsourcing of Pistons HamilGine, a $3 billion maker of small industrial engines, is undergoing a major internal review to decide where the company should focus its product development efforts and strategic investment. Executive management is arguing that too much capacity and talent are being committed to producing simple, commodity-type items that provide small differentiation within the marketplace. HamilGine concluded that in its attempts to preserve jobs, it has insourced parts that are easy to manufacture, while outsourcing those that are complex or challenging. Producing commodity-like components with mature technologies is adding little to what HamilGine's customers consider important. The company has become increasingly dependent on suppliers for critical components and subassemblies that make a major difference in the performance and cost of finished products. Part of HamilGine's effort at redefining itself involves creating an understanding of insourcing/outsourcing among managers and employees. The company has sponsored workshops and presentations to convey executive management's vision and goals, including educating those who are directly involved in making detailed insourcing/outsourcing recommendations. One presentation given by an expert in strategic sourcing focused on the changes in the marketplace that are encouraging outsourcing. The expert noted six key trends and changes that influence insourcing/outsourcing decisions: 1. The pressure for cost reduction is severe and will continue to increase. Cost reduction pressures are forcing organizations to use their production resources more efficiently. A 2018 Hackett Group Study found that enterprise cost reduction was one of the top three strategic priorities in 69% of companies surveyed. As a result, executive management will increasingly rely on insourcing/outsourcing decisions as a way to manage costs. Pgae 2 of 12 2. Firms continue to become more specialized in product and process technology. Increased specialization implies focused investment in a process or technology, which contributes to greater cost differentials between firms. 3. 4. 5. 6. 1. Firms will increasingly focus on what they excel at while outsourcing areas of non- expertise. Some organizations are formally defining their core competencies to help guide the insourcing/outsourcing effort. This affects decisions concerning what businesses the firm should focus on. The need for responsiveness in the marketplace is increasingly affecting insourcing/outsourcing decisions. Shorter cycle times, for example, encourage greater outsourcing with less vertical integration. The time to develop a production capability or capacity may exceed the window available to enter a new market. 3. Wall Street recognizes and rewards firms with higher ROI/ROA. Because insourcing usually requires an assumption of fixed assets (and increased human capital), financial pressures are causing managers to closely examine sourcing decisions. Avoidance of fixed costs and assets is motivating many firms to rely on supplier assets. One topic that interested HamilGine managers was a discussion of how core competencies relate to outsourcing decisions. HamilGine management commonly accepted that a core competency was something the company "was good at." This view, however, is not correct. A core competency refers to skills, processes, or resources that distinguish a company, are hard to duplicate, and make that firm unique compared to other firms. Core competencies begin to define a firm's long-run, strategic ability to build a dominant set of technologies or skills. These skills enable the firm to adapt quickly to changing market opportunities. The presenter argued that three key points relate to the idea of core competence and its relationship to insourcing/outsourcing decisions. A firm should do the following: Improved computer simulation tools and forecasting software enable firms to perform insourcing/outsourcing comparisons with greater precision. These tools allow the user to perform sensitivity analysis (what-if analysis) that permits comparison of different sourcing possibilities. Concentrate internally on those components, assemblies, systems, or services that are critical to the finished product and where the firm possesses a distinctive (i.e., unique) advantage valued by the customer. 2. Consider outsourcing components, assemblies, systems, or services when suppliers have an advantage. Supplier advantages may occur because of economies of scale, process-specific investment, higher quality, familiarity with a technology, or a favourable cost structure. Recognize that once a firm outsources an item or service, it usually loses the ability to bring that production capability or technology in-house without committing a significant investment. The manager or team responsible for making an insourcing/outsourcing decision must develop a true sense of what the core competency of the organization is and whether the product or service under consideration is an integral part of that core competency. The workshops and presentations have given most participants a greater appreciation of the need to consider factors besides cost when assessing insourcing/outsourcing opportunities. One Pgae 3 of 12 breakout work session focused exclusively on developing a list of the key factors that may affect the insourcing/outsourcing analysis at HamilGine, which appears in Exhibit 1. Exhibit 1 Key Factors Supporting Insourcing/Outsourcing Decisions Factors supporting insourcing Factors supporting outsourcing 1. 1. Cost considerations favour the sup- plier. 2. 2. Supplier has specialized research and know-how, which creates differentials in cost and quality. 3. Buying firm lacks the technical abil- ity to build an item. 4. Buyer has small volume require- ments. 5. Buying firm has capacity constraints while the seller does not. 6. Buyer does not want to add perman- ent workers. Cost considerations favour the buyer. A need or desire exists to integrate in- ternal plant operations. Excess plant capacity is available that can absorb fixed overhead. A need exists to exert direct control over production and quality. Product design secrecy is an import- ant issue. A lack of reliable suppliers character- izes the supply market. Firm desires to maintain a stable workforce in a declining market. Item or service is directly part of a firm's core competency or links to the strategic plans of the organization. 9. Item or technology behind making the item is strategic to the firm. The item adds to the qualities customers consider important. 10. Union or other restrictions discourage or even prohibit outsourcing. 11. Outsourcing may create or encourage a new competitor. 3. 4. 5. 6. 7. 8. Future volume requirements are un- certain-buyer wants to transfer risk to the supplier. Item or service is routine and avail- able from many competitive sources. 9. Short cycle-time requirements dis- 7. 8. courage new investment by the buyer -using existing supplier assets is lo- gical. 10. Adding capacity at the buyer requires high capital start-up costs. 11. Process technology is mature with minimal likelihood of providing a fu- ture competitive advantage to the purchaser. The Piston Insourcing/Outsourcing Decision HamilGine is considering outsourcing production of all pistons that are part of the company's "R" series of engines. HamilGine has machined various versions of these pistons for as long as anyone at the company can remember. In fact, the company started 60 years ago as a producer of high-quality pistons. The company grew as customers requested that HamilGine produce a broader line of products. This outsourcing analysis has generated a great deal of interest and emotion among HamilGine engineers, managers, and employees. HamilGine produces pistons in three separate work cells, which differ according to the type of piston produced. Each cell has six numerically controlled machines in a U-shape layout, with a supervisor, a process engineer, a material handler, and 12 employees assigned across the three Pgae 4 of 12 cells. Employees, who are cross-trained to perform each job within their cell, work in teams of four. Hamil Gine experienced a 30 percent gain in quality and a 20 percent gain in productivity after shifting from a process layout, where equipment was grouped by similar capabilities, to work cells, where equipment was grouped to support a specific family of products. If HamilGine decides to outsource the pistons, the company will likely dedicate the floor space currently occupied by the work cells to a new product or expansion of an existing product. HamilGine will apply the work cell equipment for other applications, so the outsourcing analysis will not consider equipment write-offs beyond normal depreciation. Although there are different opinions regarding outsourcing the pistons, HamilGine engineers agreed that the process technology used to produce this family of components is mature. Gaining future competitive advantages from new technology was probably not as great as other process applications within HamilGine's production process. This did not mean, however, that HamilGine could avoid making new investments in process technology if the pistons remained in-house or that some level of process innovation is not possible. Differences over outsourcing a component that is critical to the performance of Hamil Gine's final product threatens to affect the insourcing/outsourcing decision. One engineer threatened to quit if HamilGine outsourced a component that could "bring down" the entire engine in case of quality failure. He also maintained, "Our pistons are known in the industry as first-rate." Another engineer suggested that HamilGine's supply management group, if given support from the engineers, could adequately manage any risk of poor supplier quality. However, a third engineer noted, "Opportunistic suppliers will exploit HamilGine if given the chance-we've seen it before!" This engineer warned the group about suppliers "buying in" to the piston business only to coercively raise prices. Several experienced engineers voiced the opinion that they could not imagine HamilGine outsourcing a component that was responsible for making HamilGine the company it is today. Several newer members of the engineering group suggested they should wait until the outsourcing cost analysis was complete before rendering final judgment. Management has created a cross-functional team composed of a process engineer, a cost analyst, a quality engineer, a procurement specialist, a supervisor, and a machine cell employee to conduct the outsourcing analysis. A major issue confronting this team involves determining which internal costs to apply to the analysis. Including total variable costs is straightforward because these costs are readily identifiable and vary directly with production levels. Examples of variable costs include materials, direct labour, and transportation. The team is struggling with whether (or at what level) to include total factory and administrative costs (i.e., fixed costs and the fixed portion of semi-variable costs). Factory and administrative costs include utilities, indirect labour, process engineering support, depreciation, corporate office administration, maintenance, and product design charges. Proper allocation of overhead is a difficult, and sometimes subjective, task. The assumptions the team makes about how to allocate total factory and operating costs can dramatically alter the results of the analysis. The aggregated volume for pistons over the next several years is critical to this analysis. Exhibit 2 provides a monthly forecast of expected piston volumes over the next two years. Total forecasted volume is 300,000 units in Year 1 and 345,000 units in Year 2. The team arrived at the forecast by determining the forecast for HamilGine "R" series engines, which is an independent demand item. Pistons are a dependent demand item (i.e., dependent on the demand for the final product). Pgae 5 of 12 Exhibit 2 January February March April May June July August September October November December Total Aggregated Two-Year Piston Demand Year 1 expected demand 30,000 30,000 30,000 27,000 25,000 25,000 23,000 21,000 22,000 23,000 23,000 21,000 300000 Year 2 expected demand 34,000 34,000 34,000 31,000 28,000 28,000 27,000 25,000 25,000 27,000 27,000 25,000 345000 Although this is a long-term decision likely to extend beyond 10 years, the team has confidence in its projections (including supplier pricing) only through 2 years. Although maintaining piston production internally would require some level of process investment in Years 3 through 10, the team believes any projections past Year 2 contain too much uncertainty. (Conducting a net present value for expected savings from outsourcing, if they exist, is beyond the scope of this assignment.) Insourcing Costs The team has decided that a comprehensive total cost analysis should include all direct and indirect costs incurred to support piston production. HamilGine tracks its materials and labour by completing production worksheets for each job. The team collected data for the previous year, which revealed that the three work cells produced 288,369 pistons. Direct Materials HamilGine machines the pistons from a semifinished steel alloy purchased directly from a steel foundry. The foundry ships the alloy to HamilGine in 22.68 kg (almost 50 lb.) blocks, which cost $195 per block. Each piston requires, on average, 0.5 kg (almost 1.1 lb.) of semifinished raw material for each finished piston. This figure includes scrap and waste. The team expects the semifinished raw material price to remain constant over the next two years. Although HamilGine expects greater piston volumes in Years 1 and 2 compared with current demand, the am does not believe additional material economies are available. Pgae 6 of 12 Hamil Gine spent $365,000 last year on other miscellaneous direct materials required to produce the pistons. The team expects to use this figure as a basis for calculating expected Year 1 and 2 costs for miscellaneous direct material requirements. Direct Work Cell labour The direct labour in the three work cells worked a total of 27,000 hours last year. Total payroll for direct labour was $472,500, which includes overtime pay. The average direct labour rate is $17.50 per hour ($472,500/27,000 total hours $17.50 per hour). As a rule of thumb, the team expects to add 40 percent to direct labour costs to account for benefits (health, dental, pension, etc.). The team also expects direct labour rates to increase 3 percent a year for the next two years. The team does not expect per-hour production rates to change significantly. The process is well established, and HamilGine has already captured any learning curve benefits. Work cell employees are responsible for machine setup, so the team decided not to include machine setup as a separate cost category. Indirect Work Cell Labour HamilGine assigns a full-time supervisor, material handler, and engineer to the three work cells. Last year, the supervisor earned $52,000, the material handler earned $37,000, and the engineer earned $63,000 in salary. Again, the team expects to apply an additional 40 percent to these figures to reflect fringe benefits. The team expects these salaries to increase 3 percent each year. Factory Overhead and Administrative Costs This category of costs is, without doubt, the most difficult category of cost to allocate. For example, should the team prorate part of the plant manager's salary to the piston work cells? One team member argued that these costs are present with or without piston production and, therefore, should not be part of the insourcing calculation. Another member maintained that factory overhead supports the factory, and the three work cells are a major part of the factory. Not including these costs would distort the insourcing calculation. She noted that the supplier is most assuredly considering these costs when quoting the piston contract. Another member suggested performing two analyses of insourcing costs. One would include factory overhead and administrative costs, and the other would exclude these costs. The team divided the factory into six "zones" based on the functions performed throughout the plant. The piston work cells account for 25 percent of the factory's floor space, 28 percent of total direct labour hours, and 23 percent of plant volume. From this analysis, the team has decided to allocate 25 percent of the factory's overhead and administrative costs to the piston work cells for the analysis that includes these costs. Exhibit 3 presents relevant cost data for the previous year. The team expects these costs to increase 3 percent each year. Pgae 7 of 12 Exhibit 3 COST CATEGORY Administrative staff Staff engineering Taxes Utilities Insurance Plant maintenance. Total Total Factory Overhead and Administrative Costs PREVIOUS YEAR EXPENSE/COST $1,200,000 $900,000 $ 120,000 $1,500,000 $500,000 $ 800,000 $5,020,000 Preventive Maintenance Costs HamilGine spent $40,250 on preventive maintenance activities on the 18 machines in the three cells last year and expects this to increase by 10 percent in each of the next two years (due to the increasing age of the equipment). Machine Repair Costs An examination of maintenance work orders reveals that the 18 work cell machines, which are each five to seven years old, required total unplanned repair expenses of $37,000 last year. The maintenance supervisor expects this figure to increase by 8 percent in Year 1 and 12 percent in Year 2 of the analysis due to increasing age and volumes. Ordering Costs Although HamilGine produces pistons in-house, the company still incurs ordering costs for direct materials. The team estimates that each monthly order to the foundry and other suppliers costs Hamil Gine $1,500 in direct and transaction-related costs. Semifinished Raw Material Inventory Carrying Costs HamilGine typically maintains one month of semifinished raw material inventory as safety and buffer stock. The carrying charge assigned to this inventory is 18 percent annually. Inbound Transportation HamilGine receives a monthly shipment of semifinished alloy that the work cells use to machine the pistons. Total transportation costs for the previous year amounted to $31,500 (which resulted in 288,369 pistons produced). The team expects transportation charges for other direct materials used in production to be $0.01 per unit in Years 1 and 2 of the analysis. Pgae 8 of 12 Consumable Tooling Costs The machines in the work cell are notorious for "going through tooling." Given the consumable tooling costs realized during the previous year, the team estimates additional tooling expenses of $56,000 in Year 1 and $65,000 in Year 2. Depreciation The team has decided to include in its cost calculation normal depreciation expenses for the 18 work cell machines. The depreciation expense for the equipment is $150,000 per year. Finished Piston Carrying Costs Because HamilGine coordinates the production of pistons with the production of "R"- series engines, any inventory carrying charges for finished pistons are part of the cost of the finished engine and are not considered relevant to this calculation. Opportunity Costs The team recognizes that opportunities may exist for achieving a better return on the space and equipment committed to piston production. Unfortunately, the team does not know with any certainty what management's plans may be for the floor space or equipment if HamilGine outsources piston production. The team is confident, however, that management will find a use for the space. If the facility no longer engages in piston production, then HamilGine must allocate fixed factory and overhead costs across a lower base of production. This will increase the average costs of the remaining items produced in the plant, possibly making them uncompetitive compared with external suppliers. Outsourcing Costs The following provides relevant information collected by the team as it relates to outsourcing the family of pistons to an external supplier. Although it is beyond the scope of this case, the team has already performed a rigorous assessment of the supply market and has reached consensus on the external supplier in the event the team recommends outsourcing. This was necessary to obtain reliable outsourcing cost data. Unit Price The most obvious cost in an outsourcing analysis is the unit price quoted by the supplier. In many respects, outsourcing is an exercise in supplier evaluation and selection. Insourcing/outsourcing requires the evaluation of several suppliers in depth-the internal supplier (HamilGine) and external suppliers (in the marketplace). The supplier that the team favours if HamilGine outsources the pistons quoted an average unit price of $12.45 per piston (recall that this outsourcing decision involves different piston part numbers). The team believes that negotiation will occur if HamilGine elects to outsource, perhaps resulting in a lower quoted price. Because the team does not yet know the final negotiated price, some members argued Pgae 9 of 12 that several outsourcing analyses are required to reflect different possible unit prices. Quoted terms are 2/10, net 30. The supplier says it will maintain the negotiated price over the next two years. Safety Stock Requirements If the team decides to outsource, HamilGine will hold physical stock from the supplier equivalent to one month's average demand. This results in an inventory carrying charge, which the team must calculate and include in the total cost analysis. Although HamilGine likely will rely on or draw down safety stock levels during the next two years, for purposes of costing the inventory, the team has decided not to estimate when this might occur. Inventory carrying charges include working capital committed to financing the inventory, plus charges for material handling, warehousing, insurance and taxes, and risk of obsolescence and damage. Hamil Gine's inventory carrying charge is 18 percent annually. Administrative Support Costs Hamil Gine expects to commit the equivalent of one-third of a buyer's total time to supporting the commercial issues related to the outsourced family of pistons. The team estimates the buyer's salary at $54,000, with 40 percent for fringe benefits. The team expects the buyer's compensation to increase by 3 percent each year. Ordering Costs The team expects that HamilGine will order monthly, or 12 material releases a year. Unfortunately, suppliers in this industry have not been responsive to shipping on a just-in-time basis or using electronic data interchange. Although HamilGine would like to pursue a JIT purchasing model, the team feels that assuming lower volume shipments on a frequently scheduled basis is not appropriate. The company expects the supplier to deliver one month of inventory at the beginning of each month. The team estimates the cost to release and receive an order to be $1,500 per order. Quality-Related Costs The team has decided to include quality-related costs in its outsourcing calculations. During the investigation of the supplier, a team member collected data on the process that would likely produce HamilGine's pistons. The team estimates that the supplier's defect level, based on process measurement data, will be 1,500 parts per million. HamilGine's quality assurance department estimates that each supplier defect will cost the company an average $250 in non-conformance costs. Inventory Carrying Charges HamilGine must assume inventory carrying charges for pistons received at the start of each month and then consumed at a steady rate during the month. For purposes of calculating inventory carrying costs for finished pistons provided by the supplier, the team expects to use Pgae 10 of 12 the average inventory method. The formula for determining the average number of units in inventory each month is the following: For calculation purposes, the team assumes that ending inventory each month is zero units (excluding safety stock, which requires a separate calculation). The team expects production to use all the pistons received at the beginning of each month. The carrying charge applied to inventory on an annual basis is 14 percent of the unit value of the inventory. Appendices 1 and 2 will help in the calculation of monthly carrying charges associated with holding supplier- provided piston inventory. Appendix 1 Jan Feb Mar Apr May Jun Jul Aug Sep Oct [(Beginning Inventory at the Start of Each Month + Ending Inventory at the End of Each Month)/2] x Carrying Cost Per Month Nov Dec Year 1 Inventory Carrying Charges Outsourcing Option Inventory carrying cost per month per unit Beginning Inventory 30 000 30 000 30 000 27 000 25 000 25 000 23 000 21000 22 000 23000 23000 21000 Ending inventory 0 0 0 0 0 0 0 0 0 0 0 0 Average inventory Total inventory cost Inventory carrying cost per unit Inventory carrying cost + The 14 percent figure is less than the 18 percent figure applied to safety stock carrying charges. The supplier does not receive payment until at least four weeks after HamilGine receives the pistons. This makes HamilGine's working capital committed to financing production inventory somewhat less than the capital committed to financing safety stock. Pgae 11 of 12 Appendix 2 Jan Feb Mari Apr May Jun Jul Aug Sep Oct Nov Dec Year 2 Inventory Carrying Charges Outsourcing Option Beginning Inventory. 34 000 34 000 34 000 31000 28 000 28000 27000 25 000 25 000 27000 27 000 25 000 Ending inventory 0 0 0 0 0 0 0 0 0 0 0 0 Average inventory. Inventory carrying cost per month per unit Total inventory cost Inventory carrying cost per unit. Inventory carrying cost (dollars) Transportation Charges Although it is HamilGine's policy to have suppliers ship goods FOB shipping point, the company does not accept title ownership of goods until receipt at the buyer's dock. However, the company assumes all transportation-related charges. The team estimates that transportation charges for pistons will average $2,100 per truckload, with 14 truckloads expected in Year 1 and 16 truckloads expected in Year 2. The outsourcing supplier is in the United States, which means the team does not have to consider additional costs related to international purchasing. Tooling Charges The supplier said that new tooling charges to satisfy HamilGine's production requirements would be $300,000. The team has decided to depreciate tooling charges over two years or $150,000 per year. Supplier Capacity The team has concluded that the supplier has available capacity to satisfy HamilGine's total piston requirements. Appendix 3 provides a worksheet to help in the insourcing/outsourcing cost analysis. Pgae 12 of 12 Appendix 3 Insourcing cost per unit Direct materials Semifinished Other Direct labour Indirect labour Factory overhead and administrative Preventive maintenance. Machine repair Ordering Depreciation Inventory carrying Inbound transportation Consumable tooling Other costs Total insourcing costs per unit Insourcing/Outsourcing Cost Factors Worksheet Year 2 Outsourcing cost per unit Purchase cost Safety stock Quality-related costs Year 1 Administra Ordering support Inventory carrying Transportation New tooling Other costs Total outsourcing costs per unit Year 1 Year 2 ASSIGNMENT 1. Analyse insourcing versus outsourcing using the data provided (complete Appendix 1, 2, and 3). Explain the results in Appendix 3. What should HamilGine do? Should it outsource or insource the pistons? (Note: this question will be marked only if full calculations for all tables are given; will not be marked otherwise). 2. What qualitative issues might affect your final decision? Identify any costs or issues that are not part of your analysis that might impact your decision. 3. Assume your group decided to outsource the pistons to the external supplier. How can HamilGine make sure that such an outsourcing will work and will not be more expensive than insourcing? In other words, what should HamilGine watch for, change, or control for so outsourcing would become at least as profitable? Support your claims with exact suggestions, numbers, and calculations. 4. In the case of outsourcing, what will happen to the cost per unit in Year 1 and Year 2 if the cost of quality control (cost per defect) doubles? Give exact numbers and calculations.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Botany An Introduction To Plant Biology

Authors: James D. Mauseth

6th Edition

1284077535, 978-1284077537