Answered step by step

Verified Expert Solution

Question

1 Approved Answer

This question is related to Foreign exchange and international finance. Thanks, and definite thumbs up for answers! Please stick to any rounding instructions provided. Question

This question is related to Foreign exchange and international finance. Thanks, and definite thumbs up for answers! Please stick to any rounding instructions provided.

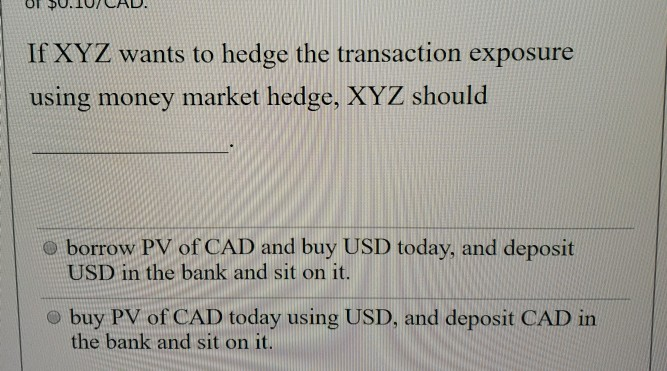

Question 27 2 pts Questions 23-36 are based on the following information Transaction Exposure Problem: (34 points in total) Suppose that you (i.e., company XYZ) are a US-based importer of goods from Canada. You expect the value of the Canada to increase against the US dollar over the next 6 months. You will be making payment on a shipment of imported goods (CAD100,000) in 6 months and want to hedge your currency exposure. The US risk-free rate is 5% and the Canada risk-free rate is 4% per year. The current spot rate is $1.25/CAD, and the 6-month forward rate is $1.3/CAD. You can also buy a 6-month option on Canadian dollars at the strike price of $1.4/CAD for a premium of $0.10/CAD. If XYZ wants to hedge the transaction exposure using money market hedge, XYZ should If XYZ wants to hedge the transaction exposure using money market hedge, XYZ should 9 borrow PV of CAD and buy USD today, and deposit USD in the bank and sit on it. o buy PV of CAD today using USD, and deposit CAD in the bank and sit on it

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Currency And Finance In Time Of War A Lecture

Authors: Francis Ysidro Edgeworth

1st Edition

1178449807, 9781178449808