Answered step by step

Verified Expert Solution

Question

1 Approved Answer

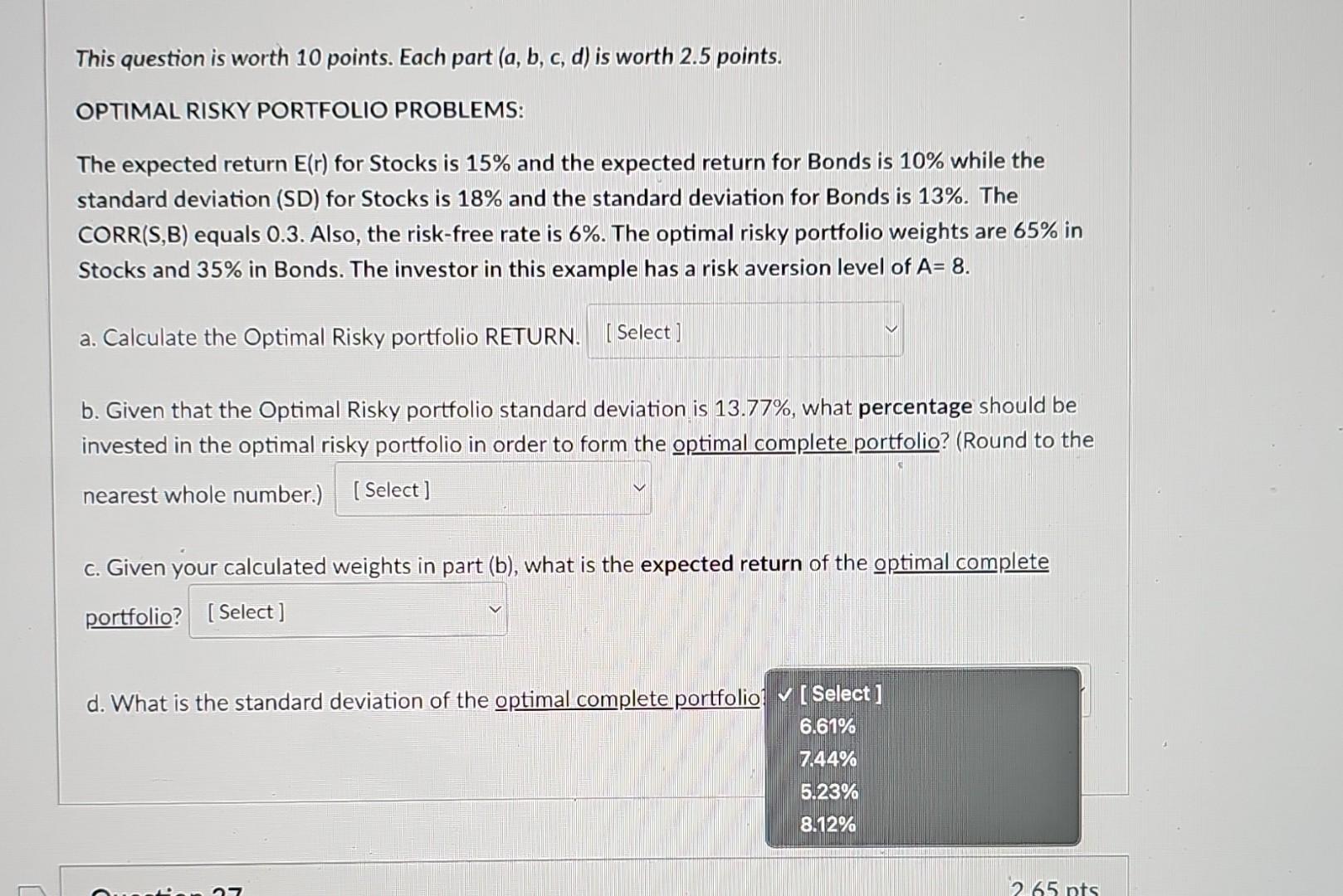

This question is worth 10 points. Each part (a,b,c,d) is worth 2.5 points. OPTIMAL RISKY PORTFOLIO PROBLEMS: The expected return E(r) for Stocks is 15%

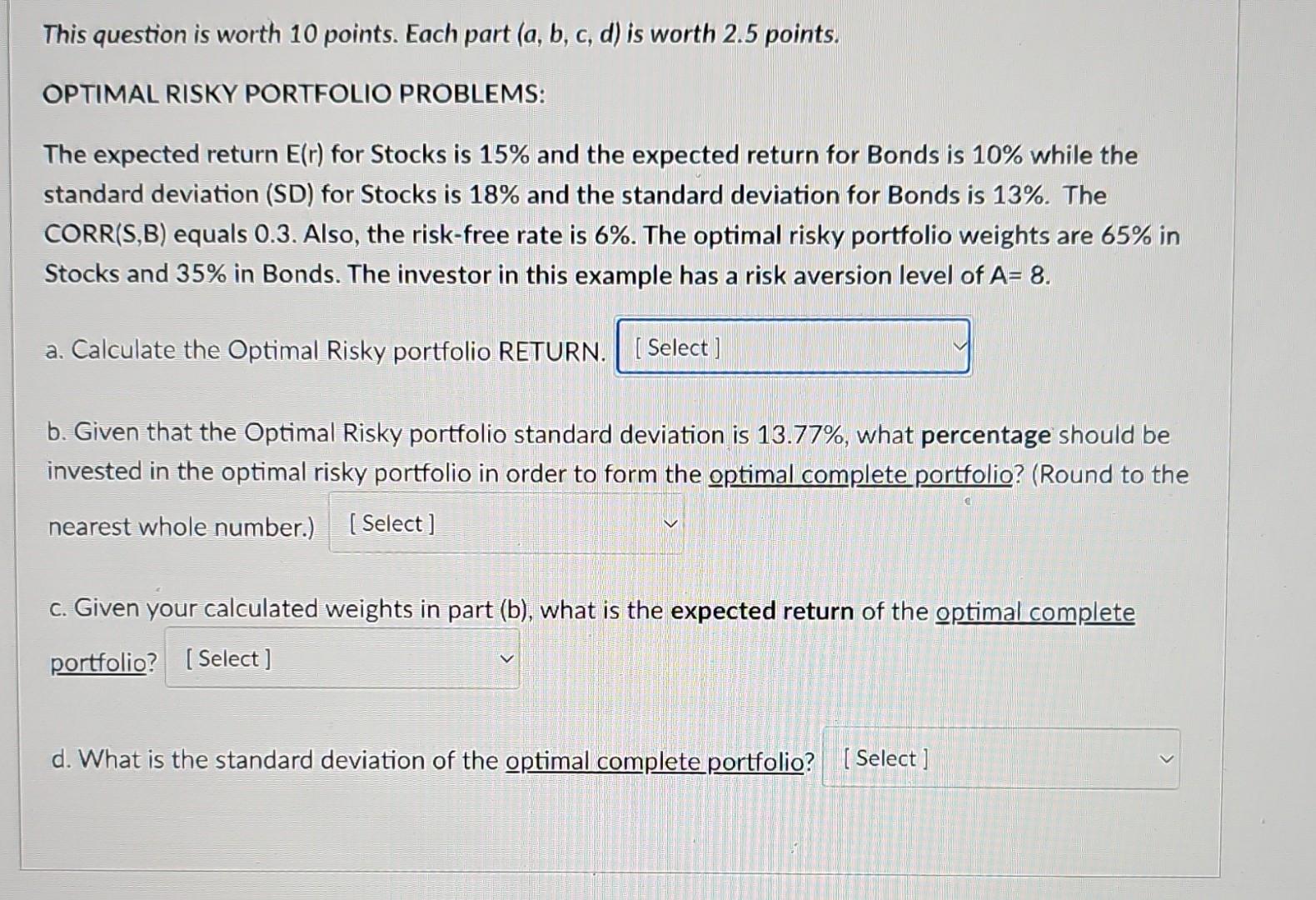

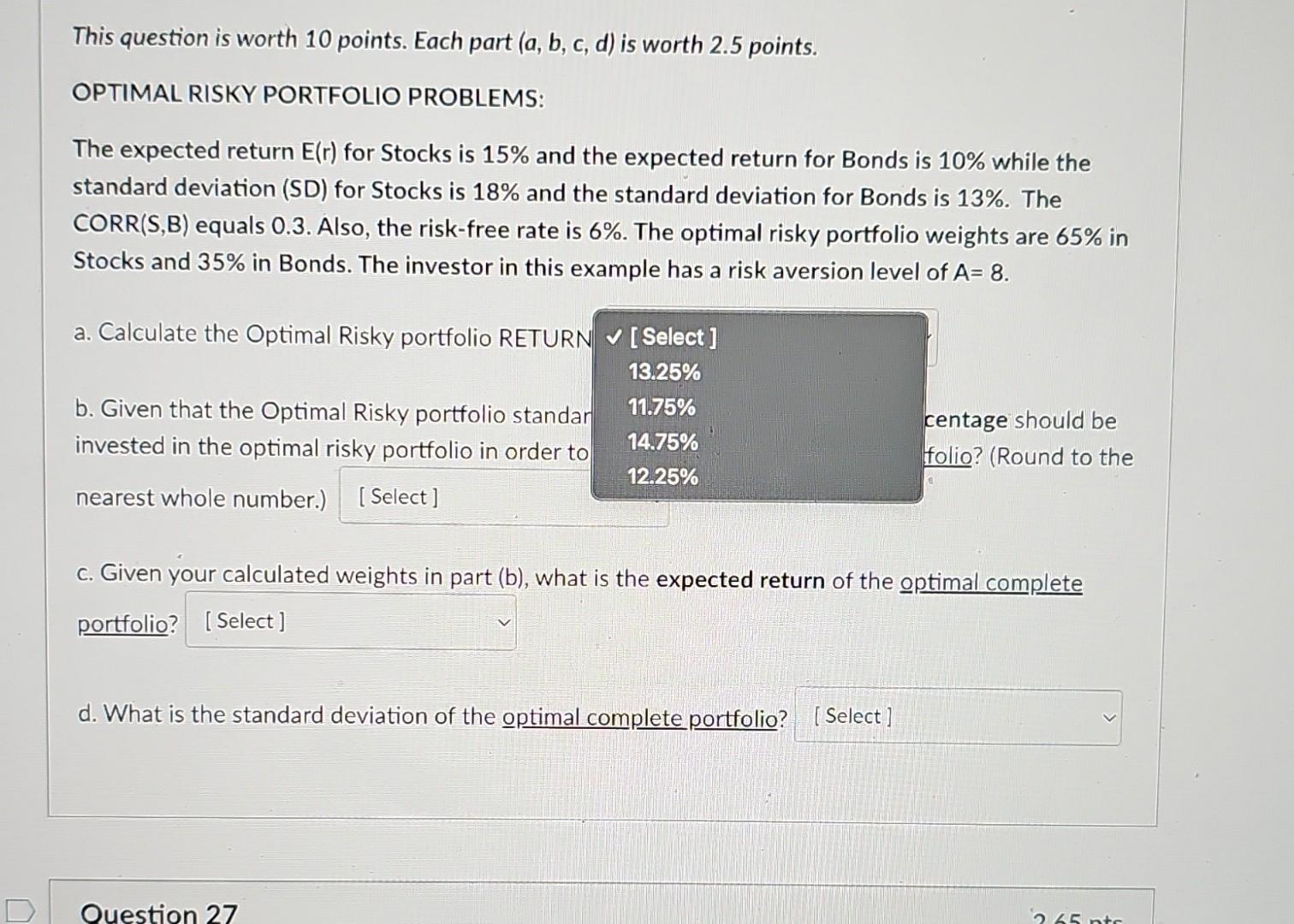

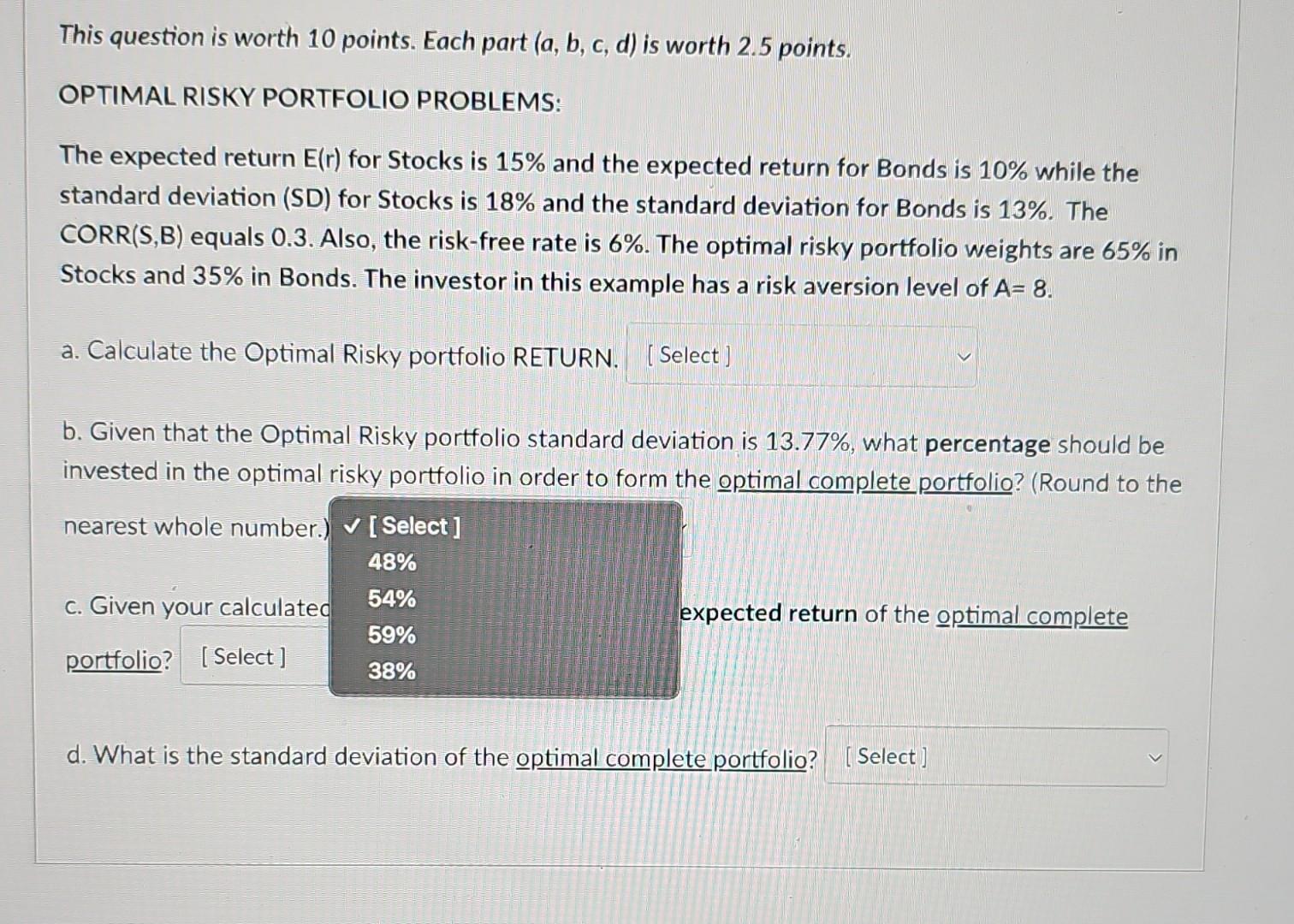

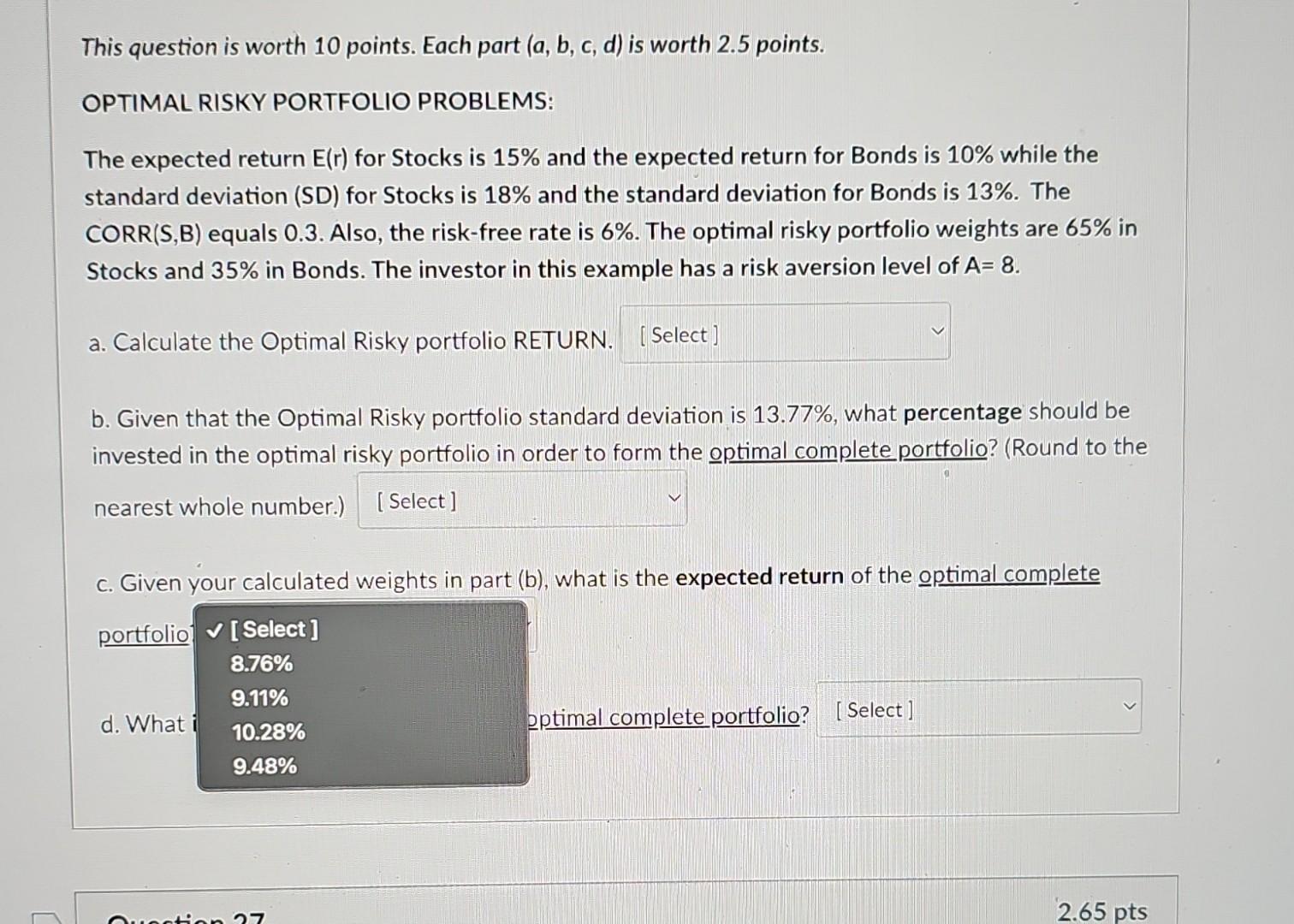

This question is worth 10 points. Each part (a,b,c,d) is worth 2.5 points. OPTIMAL RISKY PORTFOLIO PROBLEMS: The expected return E(r) for Stocks is 15% and the expected return for Bonds is 10% while the standard deviation (SD) for Stocks is 18% and the standard deviation for Bonds is 13%. The CORR(S,B) equals 0.3 . Also, the risk-free rate is 6%. The optimal risky portfolio weights are 65% in Stocks and 35% in Bonds. The investor in this example has a risk aversion level of A=8. a. Calculate the Optimal Risky portfolio RETURN. b. Given that the Optimal Risky portfolio standard deviation is 13.77%, what percentage should be invested in the optimal risky portfolio in order to form the optimal complete portfolio? (Round to the nearest whole number.) c. Given your calculated weights in part (b), what is the expected return of the optimal complete portfoliof d. What eptimal complete portfolio? This question is worth 10 points. Each part (a,b,c,d) is worth 2.5 points. OPTIMAL RISKY PORTFOLIO PROBLEMS: The expected return E(r) for Stocks is 15% and the expected return for Bonds is 10% while the standard deviation (SD) for Stocks is 18% and the standard deviation for Bonds is 13%. The CORR(S,B) equals 0.3 . Also, the risk-free rate is 6%. The optimal risky portfolio weights are 65% in Stocks and 35% in Bonds. The investor in this example has a risk aversion level of A=8. a. Calculate the Optimal Risky portfolio RETURN. b. Given that the Optimal Risky portfolio standard deviation is 13.77%, what percentage should be invested in the optimal risky portfolio in order to form the optimal complete portfolio? (Round to the nearest whole number.) c. Given your calculated :xpected return of the optimal complete portfolio? d. What is the standard deviation of the optimal complete portfolio? This question is worth 10 points. Each part (a,b,c,d) is worth 2.5 points. OPTIMAL RISKY PORTFOLIO PROBLEMS: The expected return E(r) for Stocks is 15% and the expected return for Bonds is 10% while the standard deviation (SD) for Stocks is 18% and the standard deviation for Bonds is 13%. The CORR(S,B) equals 0.3 . Also, the risk-free rate is 6%. The optimal risky portfolio weights are 65% in Stocks and 35% in Bonds. The investor in this example has a risk aversion level of A=8. a. Calculate the Optimal Risky portfolio RETURN. b. Given that the Optimal Risky portfolio standard deviation is 13.77%, what percentage should be invested in the optimal risky portfolio in order to form the optimal completeportfolio? (Round to the nearest whole number.) c. Given your calculated weights in part (b), what is the expected return of the optimal complete portfolio? d. What is the standard deviation of the optimal complete portfolio This question is worth 10 points. Each part (a,b,c,d) is worth 2.5 points. OPTIMAL RISKY PORTFOLIO PROBLEMS: The expected return E(r) for Stocks is 15% and the expected return for Bonds is 10% while the standard deviation (SD) for Stocks is 18% and the standard deviation for Bonds is 13%. The CORR(S,B) equals 0.3 . Also, the risk-free rate is 6%. The optimal risky portfolio weights are 65% in Stocks and 35% in Bonds. The investor in this example has a risk aversion level of A=8. a. Calculate the Optimal Risky portfolio RETURA b. Given that the Optimal Risky portfolio standar :entage should be invested in the optimal risky portfolio in order to folio? (Round to the nearest whole number.) c. Given your calculated weights in part (b), what is the expected return of the optimal complete portfolio? d. What is the standard deviation of the optimal complete portfolio? This question is worth 10 points. Each part (a,b,c,d) is worth 2.5 points. OPTIMAL RISKY PORTFOLIO PROBLEMS: The expected return E(r) for Stocks is 15% and the expected return for Bonds is 10% while the standard deviation (SD) for Stocks is 18% and the standard deviation for Bonds is 13%. The CORR(S,B) equals 0.3 . Also, the risk-free rate is 6%. The optimal risky portfolio weights are 65% in Stocks and 35% in Bonds. The investor in this example has a risk aversion level of A=8. a. Calculate the Optimal Risky portfolio RETURN. b. Given that the Optimal Risky portfolio standard deviation is 13.77%, what percentage should be invested in the optimal risky portfolio in order to form the optimal complete portfolio? (Round to the nearest whole number.) c. Given your calculated weights in part (b), what is the expected return of the optimal complete portfolio? d. What is the standard deviation of the optimal completeportfolio

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Numerical Techniques In Finance

Authors: Simon Benninga

1st Edition

0262022869, 978-0262022866