Answered step by step

Verified Expert Solution

Question

1 Approved Answer

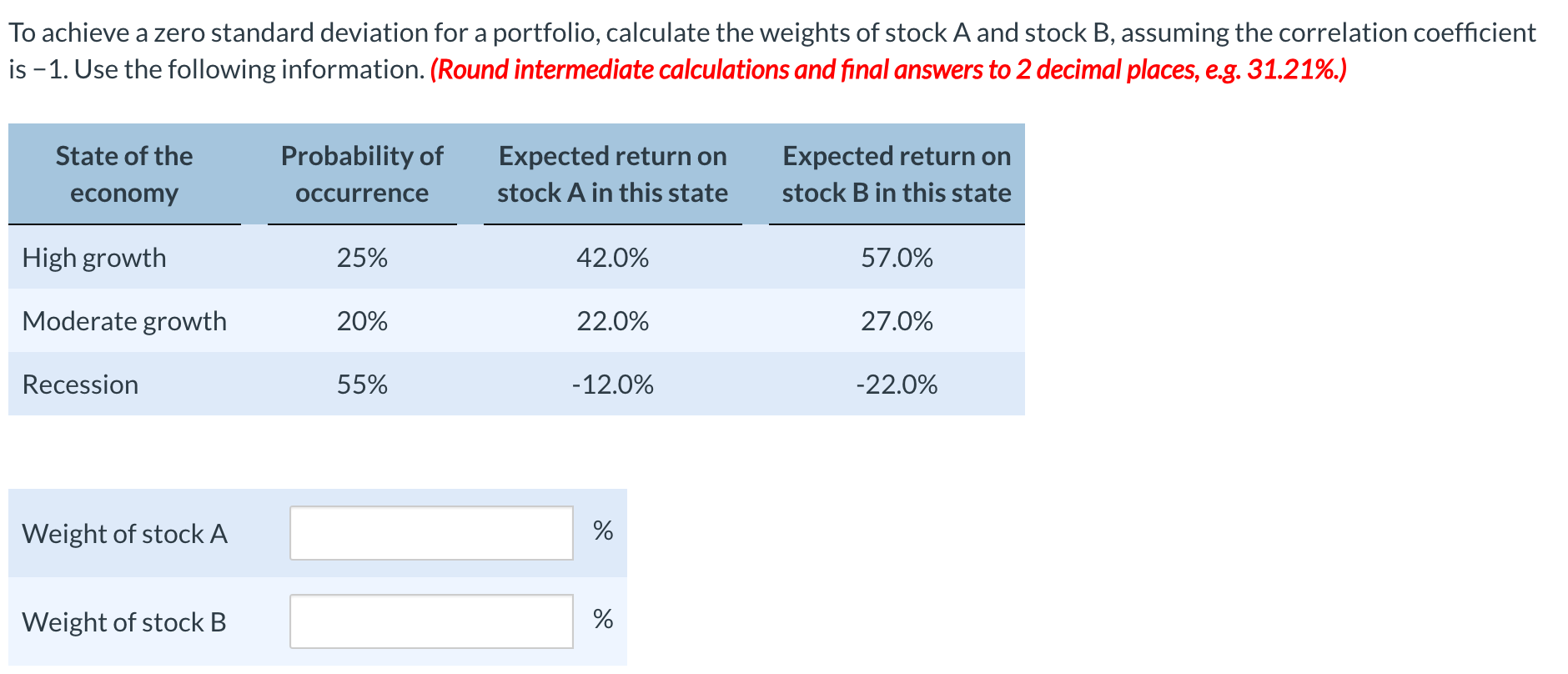

To achieve a zero standard deviation for a portfolio, calculate the weights of stock A and stock B , assuming the correlation coefficient is -

To achieve a zero standard deviation for a portfolio, calculate the weights of stock A and stock B assuming the correlation coefficient

is Use the following information. Round intermediate calculations and final answers to decimal places, eg

Weight of stock

Weight of stock BTo achieve a zero standard deviation for a portfolio, calculate the weights of stock A and stock B assuming the correlation coefficient is Use the following information. Round intermediate calculations and final answers to decimal places, eg

pls show step by step how did you solved for WeightA, because I want to know how is it done thanks

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Benchmarking Islamic Finance

Authors: Mohd Ma'Sum Billah

1st Edition

0367546469, 978-0367546465