Answered step by step

Verified Expert Solution

Question

1 Approved Answer

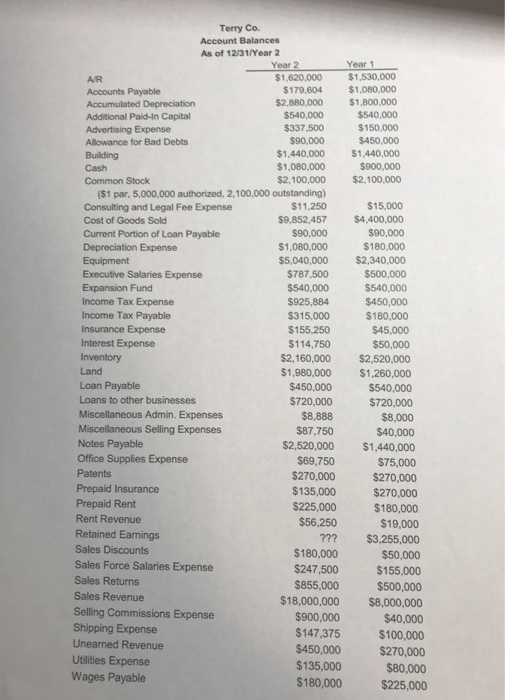

To practice making necessary correcting and adjusting entries and using them to create an adjusted trial balance. (See Topic Guides AC 6, 11, 12, 14.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Quality Management Audits In Nuclear Medicine Practices

Authors: International Atomic Energy Agency (IAEA)

1st Edition

9201121083, 978-9201121080