Question: Toys' City Case Assume that no request for acceleration was placed. Bert scheduled activities 16 to start as early as possible, but scheduled activity 8

Toys' City Case

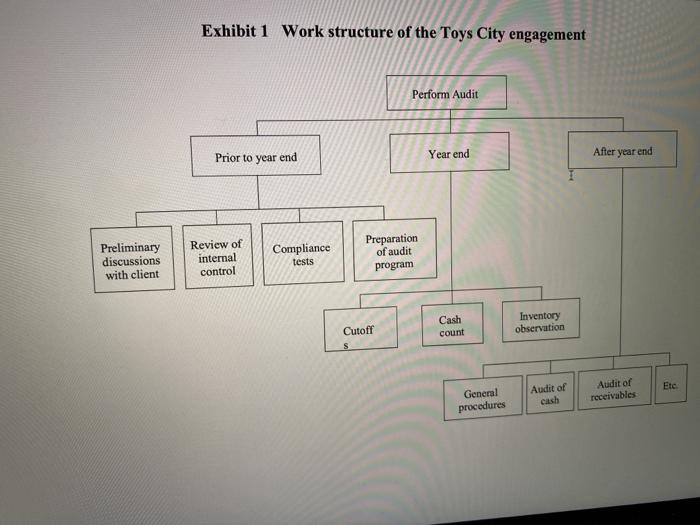

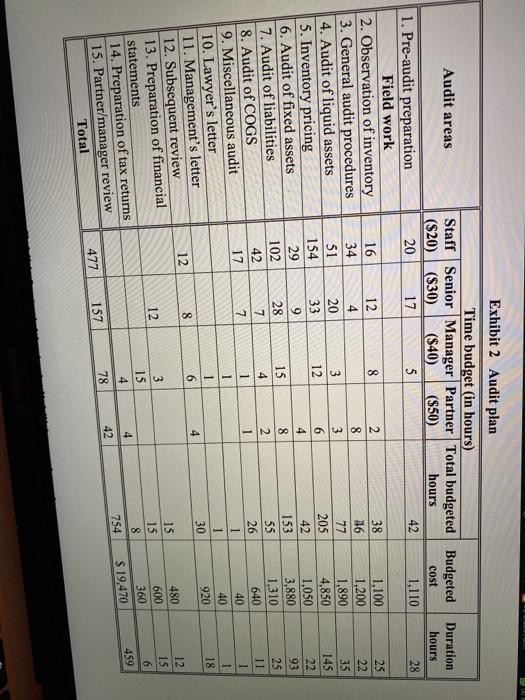

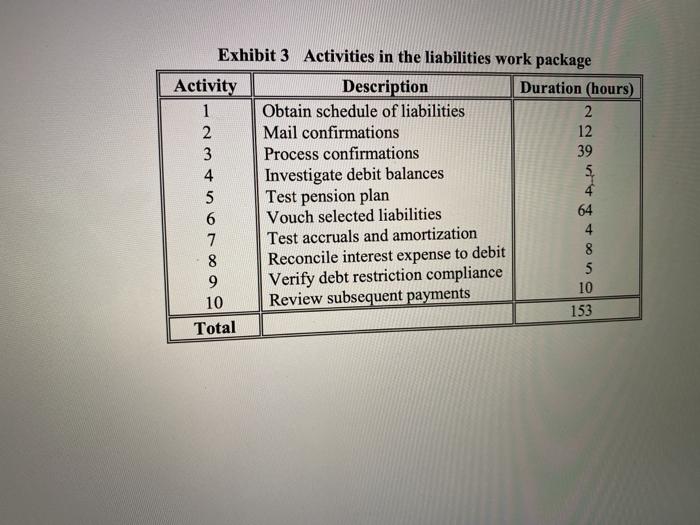

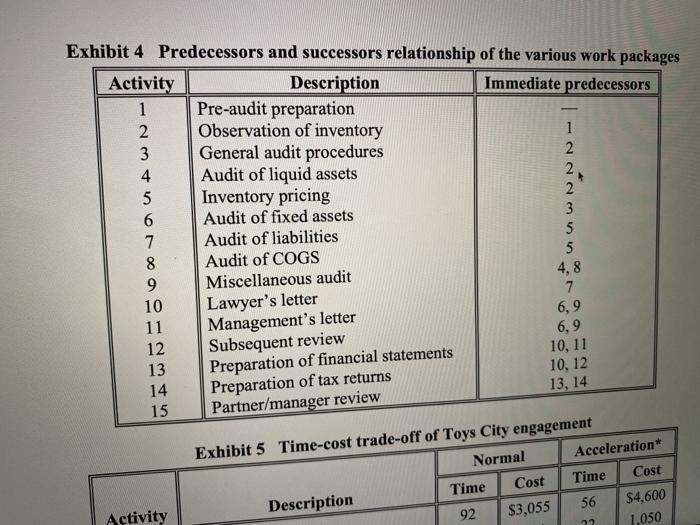

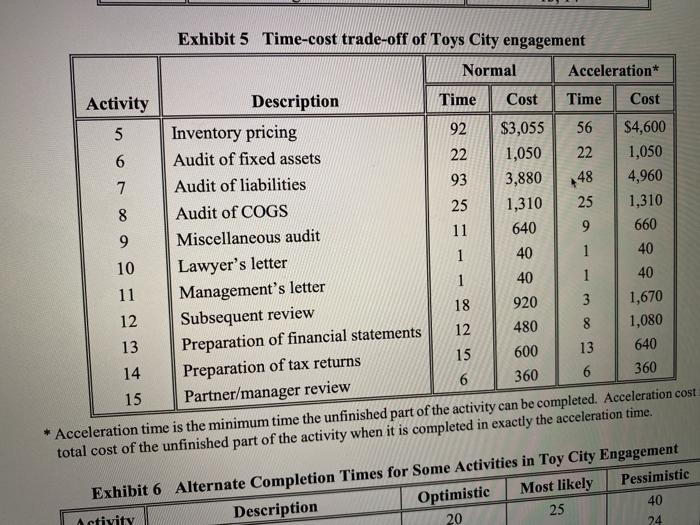

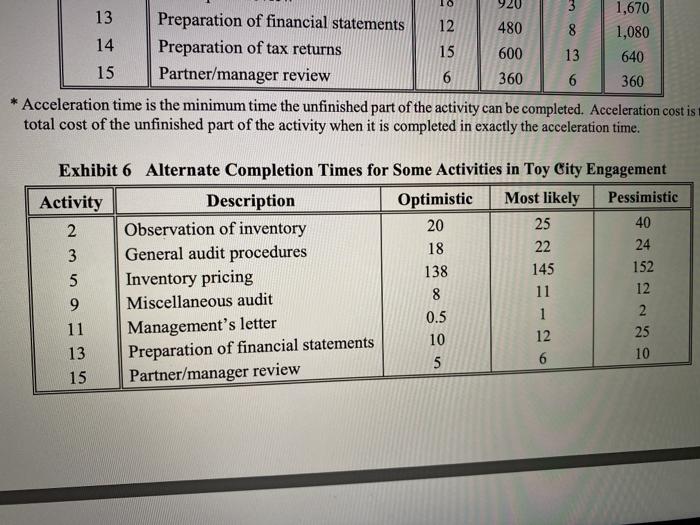

mical C My Order Goodman & Goodman, a CPA firm, has audited Toys City, Inc., for the last three years. Toys City, Inc., is a regional retailer of children's toys and games. Each of the three previous audits resulted in unqualified opinions. Toys City's year end is December 31, and Goodman & Goodman has agreed to provide the audit report on March 2, 2015, ten days before the annual board of directors meeting. Bert, the manager from Goodman & Goodman in charge of the Toys City engagement, recalls that last year there was a 25 percent budget overrun. He attributes one-third of the overrun to unforeseen circumstances and the remaining two-thirds to poor planning. He estimates that poor planning resulted in approximately 130 hours and $3,400 in audit fees that were not billed to Toys City. In an effort to avoid another costly overrun, Bert wisely decided to devote more time to audit planning. By talking to various people, Bert learns that a project management technique known as Critical Path Method (CPM) could assist an auditor in sequencing all audit detail work (including work requested from client personnel), efficiently allocating personnel resources, highlighting potential audit bottlenecks, estimating completion time, determining the probability of meeting a completion deadline, and providing a framework for relevant feedback and control as the audit progresses. Thus, he decides to spend an additional 17 hours planning this year's audit, including computer setup and analysis time, using CPM. Audit planning During the slow month of August 2014, Bert and Craig, the senior-in-charge of the Toys City engagement, analyzed the audit plan for Toys City. Basically the audit work could be divided into three phases: prior to year end, year end, and after year end. Exhibit 1 illustrates the work structure for Toys City's audit. Prior to year end the work is relatively simple and does not require much coordination. The work for the year end and after the year end, on the other hand, is mostly field work and requires much tighter control and coordination. This is the part of the audit that Bert feels the CPM method could help. Basically the audit work could be divided into three phases: prior to year end, year end, and after year end. Exhibit 1 illustrates the work structure for Toys City's audit. Prior to year end the work is relatively simple and does not require much coordination. The work for the year end and after the year end, on the other hand, is mostly field work and requires much tighter control and coordination. This is the part of the audit that Bert feels the CPM method could help. After a careful study, 15 audit areas are identified and budgeted hours for various levels of auditors are estimated (Exhibit 2). Billing rates for each auditor are indicated in parentheses below the various professional levels. Combining these rates with the budgeted hours leads to budgeted costs for the audit areas. The duration hours refer to the net time it takes to complete an audit area. Duration hours are less than total budgeted hours where audit areas permit simultaneous auditing by two or more audit personnel. Thus, to some extent, duration hours are variable depending upon the number of audit personnel available for an engagement and their assignment to various audit areas. An audit project often involves four professional levels: staff, senior, manager and partner. Generally, one manager or/and one partner takes charge of the whole project, while staff and senior auditors rotate between different projects. Different staff and senior auditors can be assigned to different audit areas and they may not stay in the same project for all the duration hours. For instance, when auditing Toys City Inc., after finishing the 'year-end procedures' work package, some of the staff and senior auditors may move to another project, while new auditors join the team to work on the subsequent audit area, 'observation of inventory'. When new auditors join the team, they often need some time to become familiar with the situation. In previous three years, there were no more than three staff auditors in one team at the same time. This year, Bert plans to have four staff auditors, at least for certain tasks. For Toys City Inc. project he intends to select his most experienced staff. Each audit area is analyzed as a separate work package in which detailed audit activities are specified in chronological order. For instance, the liabilities work package is composed of 10 tasks. First it takes 2 hours to obtain a schedule of liabilities. Then confirmations must be mailed out and processed, which take 12 hours and 39 hours respectively. After the confirmations are processed, the debit balances must be investigated, which takes 5 hours. While the confirmations are being mailed out, another staff auditor could first vouch selected liabilities and then test accruals and amortization, which takes 64 hours and 4 hours respectively. Also, after the schedule of liabilities had been obtained, a third staff auditor can spend 4 hours testing the pension plan. Once the pension plan, accruals, and amortization have been tested, the interest expense to debt can then be reconciled. This takes 8 hours. This is then followed by 5 hours of verification of the debt restriction compliance. Once the debit balances are investigated and debt restriction compliance verified, subsequent payments can then be reviewed, which takes 10 hours. Exhibit 3 summarizes the tasks for the liabilities work package and their duration. The engagement network could be depicted at various levels. A relatively detailed schedule is used in assembling time estimates and controlling audit progress while a summary version is useful for an overview. The summary version depicts each work package (such as the liabilities work package) as a simple engagement activity with duration equal to the project completion for that work package. Once the timing and duration of the various work packages have been worked out in detail, they are Once the timing and duration of the various work packages have been worked out in detail, they are linked together in chronological order. The relationship among the various fifteen work packages is summarized in Exhibit 4. Using this information, a network diagram is drawn and all critical activities are identified. The minimum time to perform the entire engagement can also be calculated One benefit that has come out of this audit planning is the cost reduction resulting from more efficient allocation of the audit staffs. For example, last year's inventory pricing required 192 hours of staff time, 30 hours of senior time, 8 hours of manager time, and 6 hours of partner time. Multiplying hours by the billing rates of the four professional levels shows that this personnel scheduling plan resulted in a total cost of $5,360. This year, Bert estimated the relative efficiency per dollar of cost for each professional level in each work package. For the inventory pricing area, it was found that it is more efficient to substitute 4 hours of manager time and 3 hours of senior time for 38 hours of staff time. The manager's and senior's general competence and familiarity with Toys City's inventory enabled them to apply overall tests of reasonableness to a major segment of inventory in lieu of staff performance of more time-consuming detail price vouching. Total cost for the inventory pricing work thereby was reduced to $4,850, resulting in saving $510. Implementation The actual audit began on January 5, 2015, as planned. Soon after the audit began, Bert received a request from John, one of the staff auditors who would be auditing liquid assets. John was getting married and would like to take a week (40 audit hours) off for his honeymoon from January 16 to January 22. There was no other auditor available in the firm to replace him. To ensure that the audit would complete on schedule and on budget, John was advised to delay his honeymoon plan until the entire project was completed. After failing to convince Bert that his plan would not affect the progress of the project, John reluctantly postponed his honeymoon and the audit engagement proceeded without any interruption. After the Toys City audit had progressed 106 duration hours, a need for acceleration arose when Bert was informed by the Toys City controller that merger negotiations had been initiated with a toy manufacturer. The controller urgently requested delivery of the audit report 1% weeks (60 hours) earlier than originally agreed. Toys City seemed to be very interested in these merger negotiations and the controller promised that the company would provide any support to accelerate the auditing process. He also hinted that a qualified report was desired and that a further acceleration request might be coming. Bert assured the Toys City controller that he would attempt to comply with the acceleration request. Since it was an extremely busy period for Goodman & Goodman, no idle auditing personnel were available in the firm for assignment to the Toys City engagement. Thus work package durations (not budgeted hours) could be reduced only by application of personnel at overtime rates, increased use of more experienced professionals (i.e., seniors, managers, and partners), and similar cost-inflating alternatives. Since Bert's CPM knowledge is still rather elementary and it is important to be able to reduce the project completion time by 60 hours at the lowest cost, Bert decided to hire Gary Fay, an external consultant, to advise him on how to proceed. After talking to Bert and various people in personnel, Gary quickly came up with the estimated acceleration times and costs for various activities tabulated in Exhibit 5. Based on these costs, the schedule for the remaining auditing procedures was revised. Bert was happy with the revised schedule as the additional cost was reasonable. The Toys City engagement was finally completed two days earlier than scheduled. After the delivery of the audit report, Bert evaluated the auditing procedures. He realized that the completion time of several work packages in fact could fluctuate depending on the individual staff performing the audit as well as the actual amount of work load. This year they were lucky that the work After the delivery of the audit report, Bert evaluated the auditing procedures. He realized that the completion time of several work packages in fact could fluctuate depending on the individual staff performing the audit as well as the actual amount of work load. This year they were lucky that the work load turned out to be much less (so that they actually completed early). For future planning, he felt that he needs more assurance about the completion time so that undesirable outcomes could be prevented. Again he sought help from Gary Fay. Gary suggested that a procedure similar to CPM called PERT could be applied. First, from the large amounts of prior history on comparable audit activities, and by talking to auditors who are familiar with the condition of Toys City's books, the effectiveness of internal control, and the likely problem areas of the engagement, optimistic and pessimistic time estimates were obtained for the work packages whose completion time may fluctuate. The information is summarized in Exhibit 6. Based on this information and results from previous calculations, the probability that the entire engagement would complete within a certain time could then be calculated. (b) Would a corporate limit on per-hour reduction cost of $70 an hour ever become a problem if further reductions were required? Why? 3. Assume that no request for acceleration was placed. Bert scheduled activities 1-6 to start as early as possible, but scheduled activity 8 (audit of COGS) to start as late as possible without delaying the entire project. On the morning of Monday, February 16 (i.e., 240 duration hours since the project has started), Bert found that the status of the project was as follows: Activities 1-6 were 100% completed, and all the activities except activity 5 (inventory pricing) had incurred exactly the budgeted costs, while inventory pricing cost $250 less than expected. Activity 7 was 55% completed, and had incurred $2650 in costs. Activity 8 was 6% completed, and had incurred $100 in costs. How long do you expect the project to take now? How much do you expect the project to cost? Exhibit 1 Work structure of the Toys City engagement Perform Audit Prior to year end Year end After year end Preliminary discussions with client Review of internal control Compliance tests Preparation of audit program Cash count Inventory observation Cutoff Etc General procedures Audit of cash Audit of receivables Audit areas Exhibit 2 Audit plan Time budget (in hours) Staff Senior Manager Partner Total budgeted Budgeted ($20) ($30) ($40) (550) hours cost 20 17 5 42 1.110 Duration hours 28 8 12 4 3 12 1. Pre-audit preparation Field work 2. Observation of inventory 3. General audit procedures 4. Audit of liquid assets 5. Inventory pricing 6. Audit of fixed assets 7. Audit of liabilities 8. Audit of COGS 9. Miscellaneous audit 10. Lawyer's letter 11. Management's letter 12. Subsequent review 13. Preparation of financial statements 14. Preparation of tax returns 15. Partner/manager review Total 16 34 51 154 29 102 42 17 20 33 9 28 7 7 2 8 3 6 4 8 2 1 38 46 77 205 42 153 55 26 1 1 30 1,100 1,200 1,890 4,850 1,050 3,880 1,310 640 40 40 920 25 22 35 145 22 93 25 11 1 1 18 15 4 1 1 1 4 12 8 3 12 15 6 12 15 4 15 15 8 754 480 600 360 $ 19,470 4 459 78 42 477 157 Exhibit 3 Activities in the liabilities work package Activity Description Duration (hours) 1 Obtain schedule of liabilities 2 2 Mail confirmations 12 3 Process confirmations 39 4 Investigate debit balances 5, 5 Test pension plan 6 Vouch selected liabilities 64 7 4 Test accruals and amortization 8 8 Reconcile interest expense to debit 5 9 Verify debt restriction compliance 10 Review subsequent payments 153 Total 10 Exhibit 4 Predecessors and successors relationship of the various work packages Activity Description Immediate predecessors 1 Pre-audit preparation 2 Observation of inventory 1 3 General audit procedures 2 4 Audit of liquid assets 2 5 Inventory pricing 2 6 Audit of fixed assets 3 5 7 Audit of liabilities 5 8 Audit of COGS 4,8 9 Miscellaneous audit 7 10 11 6,9 12 13 Preparation of financial statements 14 15 6,9 Lawyer's letter Management's letter Subsequent review 10, 11 10, 12 13, 14 Preparation of tax returns Partner/manager review Exhibit 5 Time-cost trade-off of Toys City engagement Normal Acceleration* Time Cost Description Time Cost 92 $3,055 56 $4,600 1,050 Activity 22 48 Exhibit 5 Time-cost trade-off of Toys City engagement Normal Acceleration* Activity Description Time Cost Time Cost 5 Inventory pricing 92 $3,055 56 $4,600 6 Audit of fixed assets 22 1,050 22 1,050 7 Audit of liabilities 93 3,880 4,960 8 Audit of COGS 25 1,310 25 1,310 9 Miscellaneous audit 11 640 9 660 10 1 40 1 40 Lawyer's letter 1 40 1 40 11 Management's letter 18 920 3 1,670 12 Subsequent review 12 480 8 1,080 13 Preparation of financial statements 15 600 13 640 14 Preparation of tax returns 6 360 6 15 Partner/manager review * Acceleration time is the minimum time the unfinished part of the activity can be completed. Acceleration cost total cost of the unfinished part of the activity when it is completed in exactly the acceleration time. Exhibit 6 Alternate Completion Times for Some Activities in Toy City Engagement Pessimistic Most likely Optimistic 40 Description Activity 25 20 24 360 920 3 1,670 13 Preparation of financial statements 12 480 8 1,080 14 Preparation of tax returns 15 600 13 640 Partner/manager review 6 360 6 360 Acceleration time is the minimum time the unfinished part of the activity can be completed. Acceleration cost is total cost of the unfinished part of the activity when it is completed in exactly the acceleration time. 15 * Exhibit 6 Alternate Completion T'imes for Some Activities in Toy City Engagement Activity Description Optimistic Most likely Pessimistic 2 Observation of inventory 20 25 40 3 General audit procedures 18 22 24 5 Inventory pricing 138 145 152 9 8 12 Miscellaneous audit 11 0.5 1 2 11 Management's letter 12 25 13 Preparation of financial statements 5 6 10 15 Partner/manager review mical C My Order Goodman & Goodman, a CPA firm, has audited Toys City, Inc., for the last three years. Toys City, Inc., is a regional retailer of children's toys and games. Each of the three previous audits resulted in unqualified opinions. Toys City's year end is December 31, and Goodman & Goodman has agreed to provide the audit report on March 2, 2015, ten days before the annual board of directors meeting. Bert, the manager from Goodman & Goodman in charge of the Toys City engagement, recalls that last year there was a 25 percent budget overrun. He attributes one-third of the overrun to unforeseen circumstances and the remaining two-thirds to poor planning. He estimates that poor planning resulted in approximately 130 hours and $3,400 in audit fees that were not billed to Toys City. In an effort to avoid another costly overrun, Bert wisely decided to devote more time to audit planning. By talking to various people, Bert learns that a project management technique known as Critical Path Method (CPM) could assist an auditor in sequencing all audit detail work (including work requested from client personnel), efficiently allocating personnel resources, highlighting potential audit bottlenecks, estimating completion time, determining the probability of meeting a completion deadline, and providing a framework for relevant feedback and control as the audit progresses. Thus, he decides to spend an additional 17 hours planning this year's audit, including computer setup and analysis time, using CPM. Audit planning During the slow month of August 2014, Bert and Craig, the senior-in-charge of the Toys City engagement, analyzed the audit plan for Toys City. Basically the audit work could be divided into three phases: prior to year end, year end, and after year end. Exhibit 1 illustrates the work structure for Toys City's audit. Prior to year end the work is relatively simple and does not require much coordination. The work for the year end and after the year end, on the other hand, is mostly field work and requires much tighter control and coordination. This is the part of the audit that Bert feels the CPM method could help. Basically the audit work could be divided into three phases: prior to year end, year end, and after year end. Exhibit 1 illustrates the work structure for Toys City's audit. Prior to year end the work is relatively simple and does not require much coordination. The work for the year end and after the year end, on the other hand, is mostly field work and requires much tighter control and coordination. This is the part of the audit that Bert feels the CPM method could help. After a careful study, 15 audit areas are identified and budgeted hours for various levels of auditors are estimated (Exhibit 2). Billing rates for each auditor are indicated in parentheses below the various professional levels. Combining these rates with the budgeted hours leads to budgeted costs for the audit areas. The duration hours refer to the net time it takes to complete an audit area. Duration hours are less than total budgeted hours where audit areas permit simultaneous auditing by two or more audit personnel. Thus, to some extent, duration hours are variable depending upon the number of audit personnel available for an engagement and their assignment to various audit areas. An audit project often involves four professional levels: staff, senior, manager and partner. Generally, one manager or/and one partner takes charge of the whole project, while staff and senior auditors rotate between different projects. Different staff and senior auditors can be assigned to different audit areas and they may not stay in the same project for all the duration hours. For instance, when auditing Toys City Inc., after finishing the 'year-end procedures' work package, some of the staff and senior auditors may move to another project, while new auditors join the team to work on the subsequent audit area, 'observation of inventory'. When new auditors join the team, they often need some time to become familiar with the situation. In previous three years, there were no more than three staff auditors in one team at the same time. This year, Bert plans to have four staff auditors, at least for certain tasks. For Toys City Inc. project he intends to select his most experienced staff. Each audit area is analyzed as a separate work package in which detailed audit activities are specified in chronological order. For instance, the liabilities work package is composed of 10 tasks. First it takes 2 hours to obtain a schedule of liabilities. Then confirmations must be mailed out and processed, which take 12 hours and 39 hours respectively. After the confirmations are processed, the debit balances must be investigated, which takes 5 hours. While the confirmations are being mailed out, another staff auditor could first vouch selected liabilities and then test accruals and amortization, which takes 64 hours and 4 hours respectively. Also, after the schedule of liabilities had been obtained, a third staff auditor can spend 4 hours testing the pension plan. Once the pension plan, accruals, and amortization have been tested, the interest expense to debt can then be reconciled. This takes 8 hours. This is then followed by 5 hours of verification of the debt restriction compliance. Once the debit balances are investigated and debt restriction compliance verified, subsequent payments can then be reviewed, which takes 10 hours. Exhibit 3 summarizes the tasks for the liabilities work package and their duration. The engagement network could be depicted at various levels. A relatively detailed schedule is used in assembling time estimates and controlling audit progress while a summary version is useful for an overview. The summary version depicts each work package (such as the liabilities work package) as a simple engagement activity with duration equal to the project completion for that work package. Once the timing and duration of the various work packages have been worked out in detail, they are Once the timing and duration of the various work packages have been worked out in detail, they are linked together in chronological order. The relationship among the various fifteen work packages is summarized in Exhibit 4. Using this information, a network diagram is drawn and all critical activities are identified. The minimum time to perform the entire engagement can also be calculated One benefit that has come out of this audit planning is the cost reduction resulting from more efficient allocation of the audit staffs. For example, last year's inventory pricing required 192 hours of staff time, 30 hours of senior time, 8 hours of manager time, and 6 hours of partner time. Multiplying hours by the billing rates of the four professional levels shows that this personnel scheduling plan resulted in a total cost of $5,360. This year, Bert estimated the relative efficiency per dollar of cost for each professional level in each work package. For the inventory pricing area, it was found that it is more efficient to substitute 4 hours of manager time and 3 hours of senior time for 38 hours of staff time. The manager's and senior's general competence and familiarity with Toys City's inventory enabled them to apply overall tests of reasonableness to a major segment of inventory in lieu of staff performance of more time-consuming detail price vouching. Total cost for the inventory pricing work thereby was reduced to $4,850, resulting in saving $510. Implementation The actual audit began on January 5, 2015, as planned. Soon after the audit began, Bert received a request from John, one of the staff auditors who would be auditing liquid assets. John was getting married and would like to take a week (40 audit hours) off for his honeymoon from January 16 to January 22. There was no other auditor available in the firm to replace him. To ensure that the audit would complete on schedule and on budget, John was advised to delay his honeymoon plan until the entire project was completed. After failing to convince Bert that his plan would not affect the progress of the project, John reluctantly postponed his honeymoon and the audit engagement proceeded without any interruption. After the Toys City audit had progressed 106 duration hours, a need for acceleration arose when Bert was informed by the Toys City controller that merger negotiations had been initiated with a toy manufacturer. The controller urgently requested delivery of the audit report 1% weeks (60 hours) earlier than originally agreed. Toys City seemed to be very interested in these merger negotiations and the controller promised that the company would provide any support to accelerate the auditing process. He also hinted that a qualified report was desired and that a further acceleration request might be coming. Bert assured the Toys City controller that he would attempt to comply with the acceleration request. Since it was an extremely busy period for Goodman & Goodman, no idle auditing personnel were available in the firm for assignment to the Toys City engagement. Thus work package durations (not budgeted hours) could be reduced only by application of personnel at overtime rates, increased use of more experienced professionals (i.e., seniors, managers, and partners), and similar cost-inflating alternatives. Since Bert's CPM knowledge is still rather elementary and it is important to be able to reduce the project completion time by 60 hours at the lowest cost, Bert decided to hire Gary Fay, an external consultant, to advise him on how to proceed. After talking to Bert and various people in personnel, Gary quickly came up with the estimated acceleration times and costs for various activities tabulated in Exhibit 5. Based on these costs, the schedule for the remaining auditing procedures was revised. Bert was happy with the revised schedule as the additional cost was reasonable. The Toys City engagement was finally completed two days earlier than scheduled. After the delivery of the audit report, Bert evaluated the auditing procedures. He realized that the completion time of several work packages in fact could fluctuate depending on the individual staff performing the audit as well as the actual amount of work load. This year they were lucky that the work After the delivery of the audit report, Bert evaluated the auditing procedures. He realized that the completion time of several work packages in fact could fluctuate depending on the individual staff performing the audit as well as the actual amount of work load. This year they were lucky that the work load turned out to be much less (so that they actually completed early). For future planning, he felt that he needs more assurance about the completion time so that undesirable outcomes could be prevented. Again he sought help from Gary Fay. Gary suggested that a procedure similar to CPM called PERT could be applied. First, from the large amounts of prior history on comparable audit activities, and by talking to auditors who are familiar with the condition of Toys City's books, the effectiveness of internal control, and the likely problem areas of the engagement, optimistic and pessimistic time estimates were obtained for the work packages whose completion time may fluctuate. The information is summarized in Exhibit 6. Based on this information and results from previous calculations, the probability that the entire engagement would complete within a certain time could then be calculated. (b) Would a corporate limit on per-hour reduction cost of $70 an hour ever become a problem if further reductions were required? Why? 3. Assume that no request for acceleration was placed. Bert scheduled activities 1-6 to start as early as possible, but scheduled activity 8 (audit of COGS) to start as late as possible without delaying the entire project. On the morning of Monday, February 16 (i.e., 240 duration hours since the project has started), Bert found that the status of the project was as follows: Activities 1-6 were 100% completed, and all the activities except activity 5 (inventory pricing) had incurred exactly the budgeted costs, while inventory pricing cost $250 less than expected. Activity 7 was 55% completed, and had incurred $2650 in costs. Activity 8 was 6% completed, and had incurred $100 in costs. How long do you expect the project to take now? How much do you expect the project to cost? Exhibit 1 Work structure of the Toys City engagement Perform Audit Prior to year end Year end After year end Preliminary discussions with client Review of internal control Compliance tests Preparation of audit program Cash count Inventory observation Cutoff Etc General procedures Audit of cash Audit of receivables Audit areas Exhibit 2 Audit plan Time budget (in hours) Staff Senior Manager Partner Total budgeted Budgeted ($20) ($30) ($40) (550) hours cost 20 17 5 42 1.110 Duration hours 28 8 12 4 3 12 1. Pre-audit preparation Field work 2. Observation of inventory 3. General audit procedures 4. Audit of liquid assets 5. Inventory pricing 6. Audit of fixed assets 7. Audit of liabilities 8. Audit of COGS 9. Miscellaneous audit 10. Lawyer's letter 11. Management's letter 12. Subsequent review 13. Preparation of financial statements 14. Preparation of tax returns 15. Partner/manager review Total 16 34 51 154 29 102 42 17 20 33 9 28 7 7 2 8 3 6 4 8 2 1 38 46 77 205 42 153 55 26 1 1 30 1,100 1,200 1,890 4,850 1,050 3,880 1,310 640 40 40 920 25 22 35 145 22 93 25 11 1 1 18 15 4 1 1 1 4 12 8 3 12 15 6 12 15 4 15 15 8 754 480 600 360 $ 19,470 4 459 78 42 477 157 Exhibit 3 Activities in the liabilities work package Activity Description Duration (hours) 1 Obtain schedule of liabilities 2 2 Mail confirmations 12 3 Process confirmations 39 4 Investigate debit balances 5, 5 Test pension plan 6 Vouch selected liabilities 64 7 4 Test accruals and amortization 8 8 Reconcile interest expense to debit 5 9 Verify debt restriction compliance 10 Review subsequent payments 153 Total 10 Exhibit 4 Predecessors and successors relationship of the various work packages Activity Description Immediate predecessors 1 Pre-audit preparation 2 Observation of inventory 1 3 General audit procedures 2 4 Audit of liquid assets 2 5 Inventory pricing 2 6 Audit of fixed assets 3 5 7 Audit of liabilities 5 8 Audit of COGS 4,8 9 Miscellaneous audit 7 10 11 6,9 12 13 Preparation of financial statements 14 15 6,9 Lawyer's letter Management's letter Subsequent review 10, 11 10, 12 13, 14 Preparation of tax returns Partner/manager review Exhibit 5 Time-cost trade-off of Toys City engagement Normal Acceleration* Time Cost Description Time Cost 92 $3,055 56 $4,600 1,050 Activity 22 48 Exhibit 5 Time-cost trade-off of Toys City engagement Normal Acceleration* Activity Description Time Cost Time Cost 5 Inventory pricing 92 $3,055 56 $4,600 6 Audit of fixed assets 22 1,050 22 1,050 7 Audit of liabilities 93 3,880 4,960 8 Audit of COGS 25 1,310 25 1,310 9 Miscellaneous audit 11 640 9 660 10 1 40 1 40 Lawyer's letter 1 40 1 40 11 Management's letter 18 920 3 1,670 12 Subsequent review 12 480 8 1,080 13 Preparation of financial statements 15 600 13 640 14 Preparation of tax returns 6 360 6 15 Partner/manager review * Acceleration time is the minimum time the unfinished part of the activity can be completed. Acceleration cost total cost of the unfinished part of the activity when it is completed in exactly the acceleration time. Exhibit 6 Alternate Completion Times for Some Activities in Toy City Engagement Pessimistic Most likely Optimistic 40 Description Activity 25 20 24 360 920 3 1,670 13 Preparation of financial statements 12 480 8 1,080 14 Preparation of tax returns 15 600 13 640 Partner/manager review 6 360 6 360 Acceleration time is the minimum time the unfinished part of the activity can be completed. Acceleration cost is total cost of the unfinished part of the activity when it is completed in exactly the acceleration time. 15 * Exhibit 6 Alternate Completion T'imes for Some Activities in Toy City Engagement Activity Description Optimistic Most likely Pessimistic 2 Observation of inventory 20 25 40 3 General audit procedures 18 22 24 5 Inventory pricing 138 145 152 9 8 12 Miscellaneous audit 11 0.5 1 2 11 Management's letter 12 25 13 Preparation of financial statements 5 6 10 15 Partner/manager review

Assume that no request for acceleration was placed. Bert scheduled activities 16 to start as early as possible, but scheduled activity 8 (audit of COGS) to start as late as possible without delaying the entire project. On the morning of Monday, February 16 (i.e., 240 duration hours since the project has started), Bert found that the status of the project was as follows:

Activities 1-6 were 100% completed, and all the activities except activity 5 (inventory pricing) had incurred exactly the budgeted costs, while inventory pricing cost $250 less than expected.

Activity 7 was 55% completed, and had incurred $2650 in costs.

Activity 8 was 6% completed, and had incurred $100 in costs.

How long do you expect the project to take now? How much do you expect the project to cost?

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock