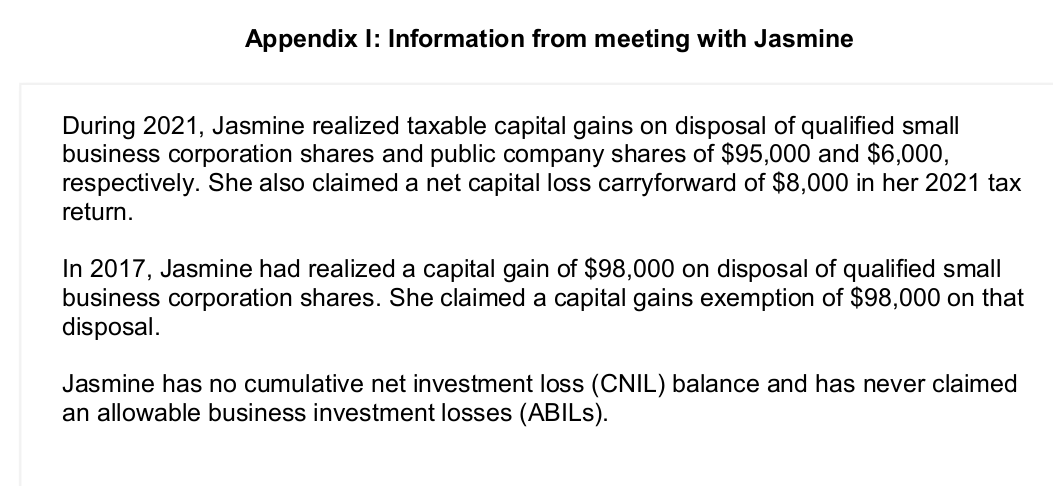

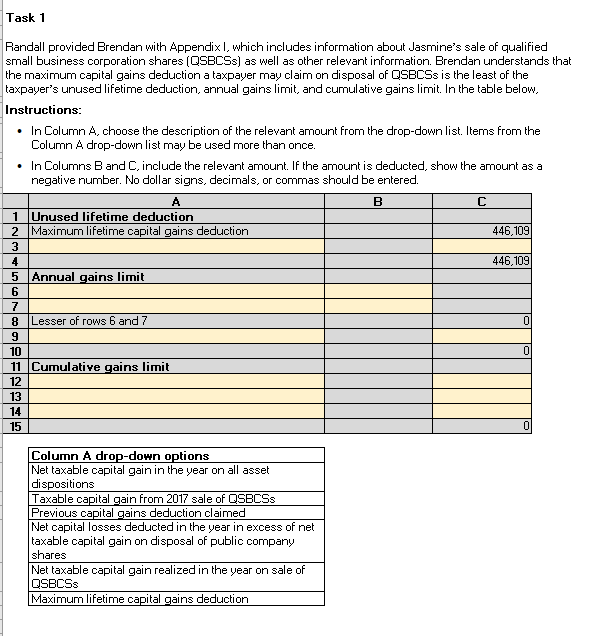

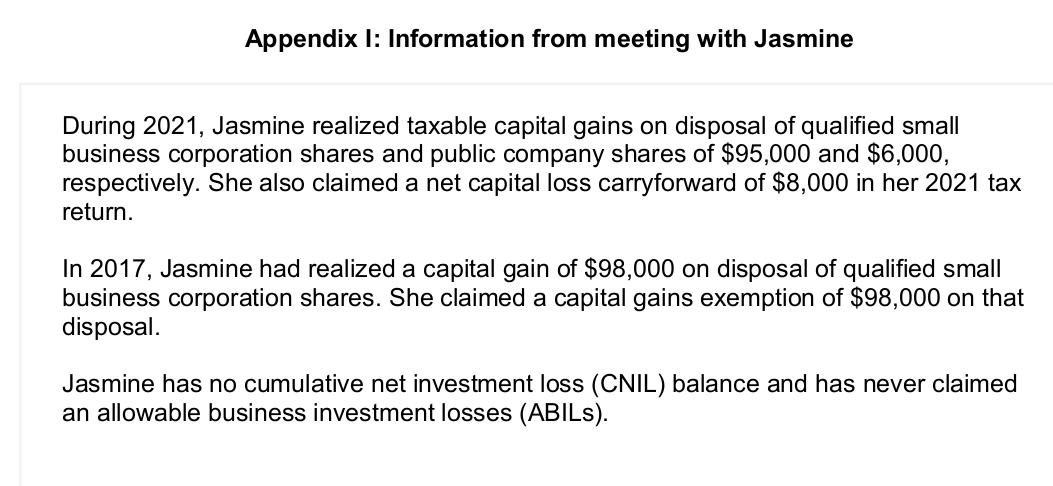

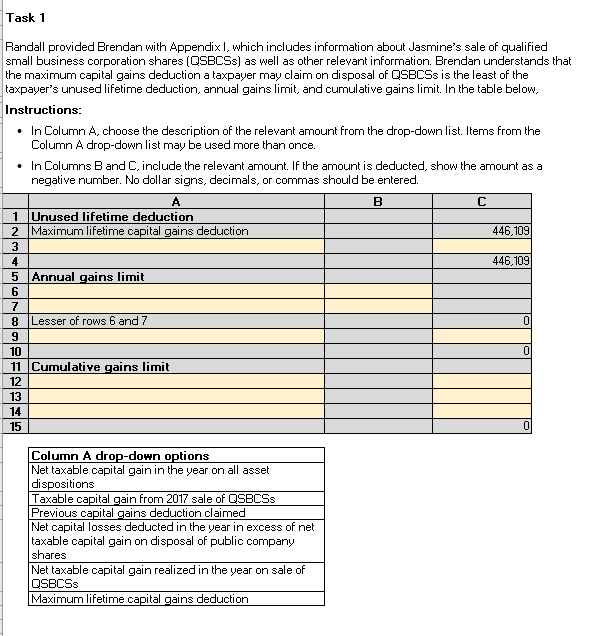

Brendan Palate recently started working for Paulson Slater LLP (PSL) in the tax department. The tax partner, Randall Slater, has asked Brendan to assist one of the clients that he recently met with. The following documents are attached: Appendix 1: Information from meeting with Jasmine Appendix 1: Information from meeting with Jasmine During 2021, Jasmine realized taxable capital gains on disposal of qualified small business corporation shares and public company shares of $95,000 and $6,000, respectively. She also claimed a net capital loss carryforward of $8,000 in her 2021 tax return. In 2017, Jasmine had realized a capital gain of $98,000 on disposal of qualified small business corporation shares. She claimed a capital gains exemption of $98,000 on that disposal. Jasmine has no cumulative net investment loss (CNIL) balance and has never claimed an allowable business investment losses (ABILs). Task 1 Randall provided Brendan with Appendix I, which includes information about Jasmine's sale of qualified small business corporation shares (QSBCSS) as well as other relevant information. Brendan understands that the maximum capital gains deduction a taxpayer may claim on disposal of QSBCSS is the least of the taxpayer's unused lifetime deduction, annual gains limit, and cumulative gains limit. In the table below, Instructions: In Column A, choose the description of the relevant amount from the drop-down list. Items from the Column A drop-down list may be used more than once. In Columns B and C, include the relevant amount. If the amount is deducted, show the amount as a negative number. No dollar signs, decimals, or commas should be entered. A B C 1 Unused lifetime deduction 2 Maximum lifetime capital gains deduction 446,109 3 4 446,109 5 Annual gains limit 6 7 8 Lesser of rows 6 and 7 0 ol 11 Cumulative gains limit 12 |89mne1314 15 10 Column A drop-down options Net taxable capital gain in the year on all asset dispositions Taxable capital gain from 2017 sale of QSBCSs Previous capital gains deduction claimed Net capital losses deducted in the year in excess of net taxable capital gain on disposal of public company shares Net taxable capital gain realized in the year on sale of QSBCSs Maximum lifetime capital gains deduction Brendan Palate recently started working for Paulson Slater LLP (PSL) in the tax department. The tax partner, Randall Slater, has asked Brendan to assist one of the clients that he recently met with. The following documents are attached: Appendix 1: Information from meeting with Jasmine Appendix 1: Information from meeting with Jasmine During 2021, Jasmine realized taxable capital gains on disposal of qualified small business corporation shares and public company shares of $95,000 and $6,000, respectively. She also claimed a net capital loss carryforward of $8,000 in her 2021 tax return. In 2017, Jasmine had realized a capital gain of $98,000 on disposal of qualified small business corporation shares. She claimed a capital gains exemption of $98,000 on that disposal. Jasmine has no cumulative net investment loss (CNIL) balance and has never claimed an allowable business investment losses (ABILs). Task 1 Randall provided Brendan with Appendix I, which includes information about Jasmine's sale of qualified small business corporation shares (QSBCSS) as well as other relevant information. Brendan understands that the maximum capital gains deduction a taxpayer may claim on disposal of QSBCSS is the least of the taxpayer's unused lifetime deduction, annual gains limit, and cumulative gains limit. In the table below, Instructions: In Column A, choose the description of the relevant amount from the drop-down list. Items from the Column A drop-down list may be used more than once. In Columns B and C, include the relevant amount. If the amount is deducted, show the amount as a negative number. No dollar signs, decimals, or commas should be entered. A B C 1 Unused lifetime deduction 2 Maximum lifetime capital gains deduction 446,109 3 4 446,109 5 Annual gains limit 6 7 8 Lesser of rows 6 and 7 0 ol 11 Cumulative gains limit 12 |89mne1314 15 10 Column A drop-down options Net taxable capital gain in the year on all asset dispositions Taxable capital gain from 2017 sale of QSBCSs Previous capital gains deduction claimed Net capital losses deducted in the year in excess of net taxable capital gain on disposal of public company shares Net taxable capital gain realized in the year on sale of QSBCSs Maximum lifetime capital gains deduction