Question

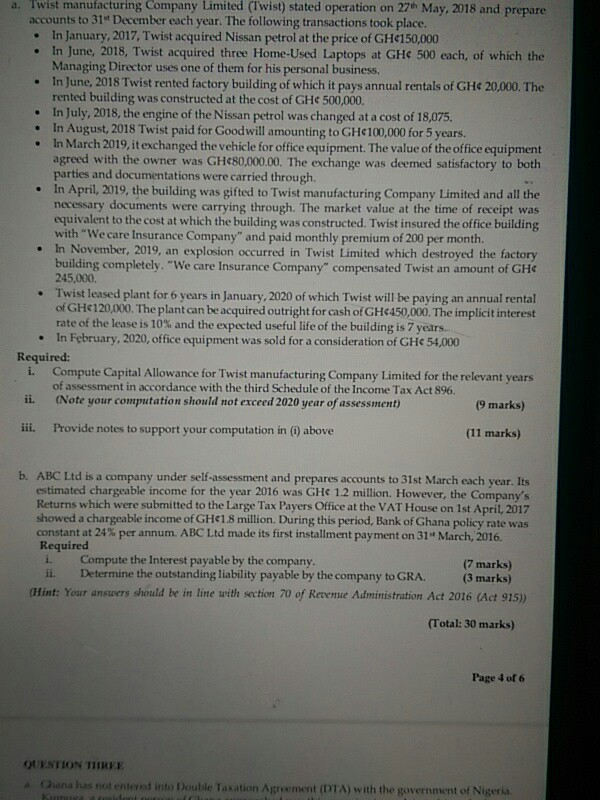

Twist manufacturing Company Limited (Twist) stated operation on 27th May, 2018 and prepare accounts to 31st December each year. The following transactions took place. In

Twist manufacturing Company Limited (Twist) stated operation on 27th May, 2018 and prepare accounts to 31st December each year. The following transactions took place. In January, 2017, Twist acquired Nissan petrol at the price of GH150,000 In June, 2018, Twist acquired three Home-Used Laptops at GH 500 each, of which the Managing Director uses one of them for his personal business. In June, 2018 Twist rented factory building of which it pays annual rentals of GH 20,000. The rented building was constructed at the cost of GH 500,000. In July, 2018, the engine of the Nissan petrol was changed at a cost of 18,075. In August, 2018 Twist paid for Goodwill amounting to GH100,000 for 5 years. In March 2019, it exchanged the vehicle for office equipment. The value of the office equipment agreed with the owner was GH80,000.00. The exchange was deemed satisfactory to both parties and documentations were carried through. In April, 2019, the building was gifted to Twist manufacturing Company Limited and all the necessary documents were carrying through. The market value at the time of receipt was equivalent to the cost at which the building was constructed. Twist insured the office building with We care Insurance Company and paid monthly premium of 200 per month. In November, 2019, an explosion occurred in Twist Limited which destroyed the factory building completely. We care Insurance Company compensated Twist an amount of GH 245,000. Twist leased plant for 6 years in January, 2020 of which Twist will be paying an annual rental of GH120,000. The plant can be acquired outright for cash of GH450,000. The implicit interest rate of the lease is 10% and the expected useful life of the building is 7 years. In February, 2020, office equipment was sold for a consideration of GH 54,000

Required:

i. Compute Capital Allowance for Twist manufacturing Company Limited for the relevant years of assessment in accordance with the third Schedule of the Income Tax Act 896.

ii. (Note your computation should not exceed 2020 year of assessment) (9 marks)

iii. Provide notes to support your computation in (i) above (11 marks)

b. ABC Ltd is a company under self-assessment and prepares accounts to 31st March each year. Its estimated chargeable income for the year 2016 was GH 1.2 million. However, the Companys Returns which were submitted to the Large Tax Payers Office at the VAT House on 1st April, 2017 showed a chargeable income of GH1.8 million. During this period, Bank of Ghana policy rate was constant at 24% per annum. ABC Ltd made its first installment payment on 31st March, 2016. Required i. Compute the Interest payable by the company. (7 marks) ii. Determine the outstanding liability payable by the company to GRA. (3 marks) (Hint: Your answers should be in line with section 70 of Revenue Administration Act 2016 (Act 915))

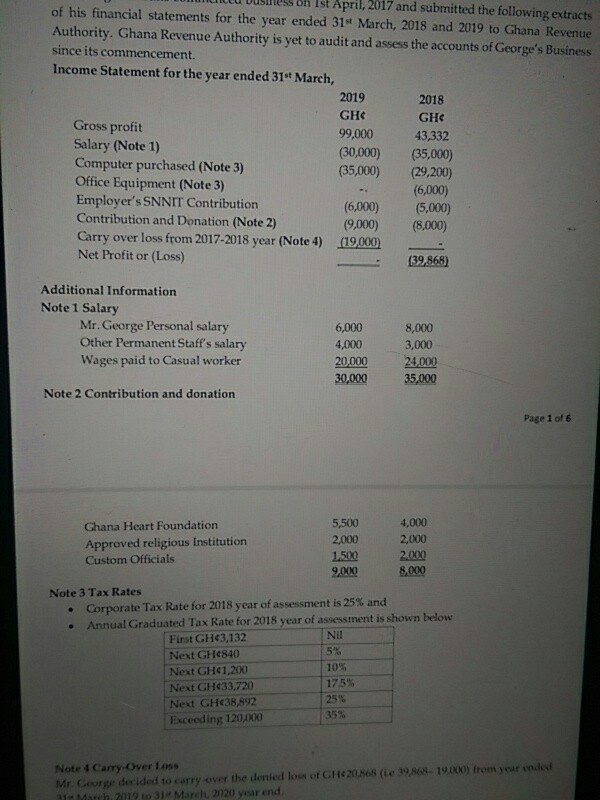

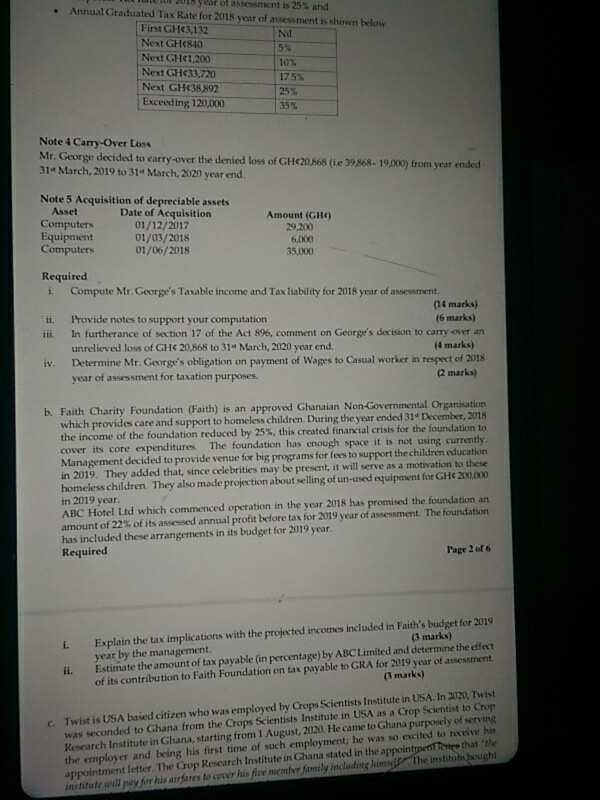

. . . a. Twist manufacturing Company Limited (Twist) stated operation on 27th May, 2018 and prepare accounts to 31 December each year. The following transactions took place. In January, 2017, Twist acquired Nissan petrol at the price of GH150,000 In June, 2018, Twist acquired three Home-Used Laptops at GH 500 each, of which the Managing Director uses one of them for his personal business. In June, 2018 Twist rented factory building of which it pays annual rentals of GH 20,000. The rented building was constructed at the cost of GH 500,000. In July, 2018, the engine of the Nissan petrol was changed at a cost of 18,075. In August, 2018 Twist paid for Goodwill amounting to GH100,000 for 5 years. In March 2019, it exchanged the vehicle for office equipment. The value of the office equipment agreed with the owner was GH80,000.00. The exchange was deemed satisfactory to both parties and documentations were carried through. In April, 2019, the building was gifted to Twist manufacturing Company Limited and all the necessary documents were carrying through. The market value at the time of receipt was equivalent to the cost at which the building was constructed. Twist insured the office building with "We care Insurance Company" and paid monthly premium of 200 per month In November, 2019, an explosion occurred in Twist Limited which destroyed the factory building completely. "We care Insurance Company" compensated Twist an amount of GH 245,000 Twist leased plant for 6 years in January, 2020 of which Twist will be paying an annual rental of GH120,000. The plant can be acquired outright for cash of GH450,000. The implicit interest rate of the lease is 10% and the expected useful life of the building is 7 years. In February, 2020, office equipment was sold for a consideration of GH 54,000 Required: i. Compute Capital Allowance for Twist manufacturing Company Limited for the relevant years of assessment in accordance with the third Schedule of the Income Tax Act 896. (Note your computation should not exceed 2020 year of assessment) (9 marks) iii. Provide notes to support your computation in (1) above (11 marks) b. ABC Ltd is a company under self-assessment and prepares accounts to 31st March each year. Its estimated chargeable income for the year 2016 was GHe 1.2 million. However, the Company's Returns which were submitted to the Large Tax Payers Office at the VAT House on 1st April, 2017 showed a chargeable income of GH1.8 million. During this period, Bank of Ghana policy rate was constant at 24% per annum. ABC Ltd made its first installment payment on 31 March, 2016. Required Compute the Interest payable by the company. (7 marks) ii. Determine the outstanding liability payable by the company to GRA. (3 marks) (Hint: Your answers should be in line with section 70 of Revenue Administration Act 2016 (Act 915)) (Total: 30 marks) Page 4 of 6 QUESTION THREE Chana has not entered into Double Taxation Agreement (DTA) with the government of Nigeria Ist April, 2017 and submitted the following extracts of his financial statements for the year ended 31st March, 2018 and 2019 to Ghana Revenue Authority. Ghana Revenue Authority is yet to audit and assess the accounts of George's Business since its commencement. Income Statement for the year ended 31 March, 2019 2018 GHC GH Gross profit 99,000 43,332 Salary (Note 1) (30,000) (35,000) Computer purchased (Note 3) (35,000) (29,200) Office Equipment (Note 3) (6,000) Employer's SNNIT Contribution (6,000) (5,000) Contribution and Donation (Note 2) (9,000) (8,000) Carry over loss from 2017-2018 year (Note 4) (19,000) Net Profit or (Loss) (39,868) Additional Information Note 1 Salary Mr. George Personal salary Other Permanent Staff's salary Wages paid to Casual worker 6,000 4,000 20,000 30,000 8,000 3,000 24,000 35,000 Note 2 Contribution and donation Page 1 of 6 Ghana Heart Foundation 5,500 4,000 Approved religious Institution 2,000 2,000 Custom Officials 1.500 2,000 9.000 8,000 Note 3 Tax Rates Corporate Tax Rate for 2018 year of assessment is 25% and Annual Graduated Tax Rate for 2018 year of assessment is shown below First GH3,132 Nil Next GH4840 5% Next GH1,200 10% Next CH33,720 175% Next GH38,892 25% Exceeding 120,000 35% Note 4 Carry Over Loss Mr. George decided to carry over the denied low of CH420.868 ( 39,868-19.000) from your ended 31 March 2019 to 31 March 2020 year end . er of assessment is 25% and Annual Graduated Tax Rate for 2018 year of assessment is shown below First GH43,132 Nil Next GH6840 5% Next GH41,200 10% Next GH433,720 175% Next GH

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Trusted Advisors Key Attributes Of Outstanding Internal Auditors

Authors: Richard F. Chambers, President And CEO Of The IIA

1st Edition

0894139819, 978-0894139819