Answered step by step

Verified Expert Solution

Question

1 Approved Answer

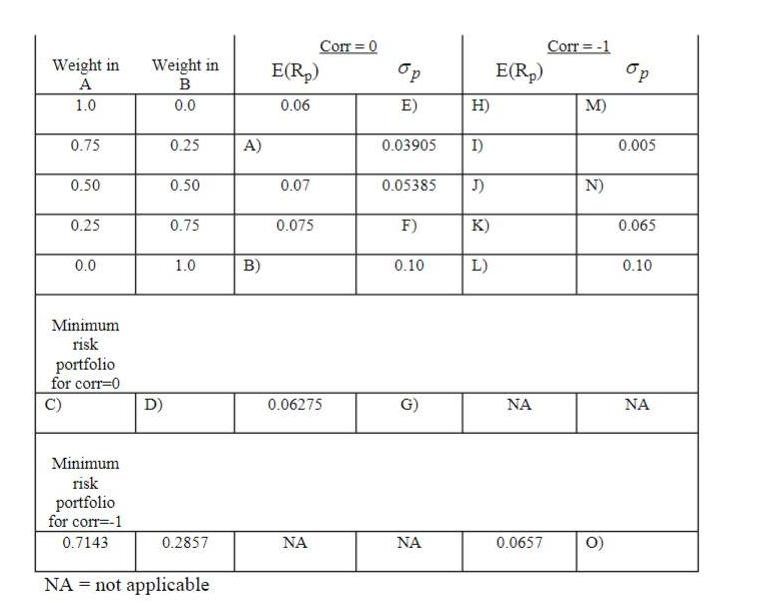

Two securities have the following characteristics: E(R) =.06 E(R) =.08 a = .04 % = .10 1A) (15 points) Fill in the missing cells

Two securities have the following characteristics: E(R) =.06 E(R) =.08 a = .04 % = .10 1A) (15 points) Fill in the missing cells (A through O) in the table. For each of two correlation cases, corr. = -1 and corr. = 0, calculate the attainable portfolios' mean and standard deviation from combining the two assets together using weights in increments of 25% from 1 to 0. Also, calculate the minimum risk portfolio's weights, mean and standard deviation for the correlation= 0 case (for the case of the correlation = -1, I have already calculated the weights for you!). Assume that the risk free rate is .04. Hint: in some of the cases, filling in the cells requires no calculations. Note, throughout this problem, returns are in decimal form, i.e.. 1%-0.01. Weight in A 1.0 0.75 0.50 0.25 0.0 Minimum risk portfolio for corr-0 C) Minimum risk portfolio for corr=-1 0.7143 Weight in B 0.0 D) 0.25 0.50 0.75 1.0 0.2857 NA not applicable = A) B) E(R) 0.06 0.07 0.075 Corr=0 0.06275 Op E) 0.03905 0.05385 F) 0.10 G) H) I) J) K) L) E(Rp) 0.0657 Corr= -1 M) N) op 0.005 0.065 0.10

Step by Step Solution

★★★★★

3.34 Rating (154 Votes )

There are 3 Steps involved in it

Step: 1

To fill in the missing cells in the table we can follow these steps 1 For the correlation case of ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

An Introduction To Statistical Methods And Data Analysis

Authors: R. Lyman Ott, Micheal T. Longnecker

7th Edition

1305269470, 978-1305465527, 1305465520, 978-1305269477