Answered step by step

Verified Expert Solution

Question

1 Approved Answer

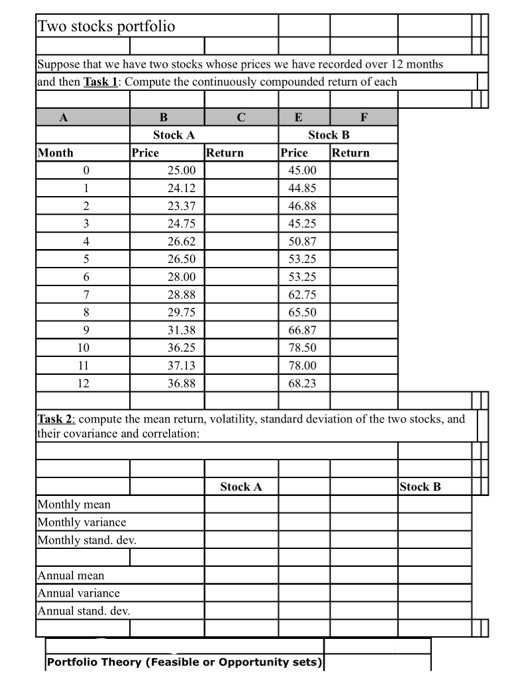

Two stocks portfolio Suppose that we have two stocks whose prices we have recorded over 12 months and then Task 1: Compute the continuously compounded

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Handbook Of Research On Decision Making Techniques In Financial Marketing

Authors: Hasan Dinçer, Serhat Yüksel

1st Edition

1799825590, 978-1799825593