Answered step by step

Verified Expert Solution

Question

1 Approved Answer

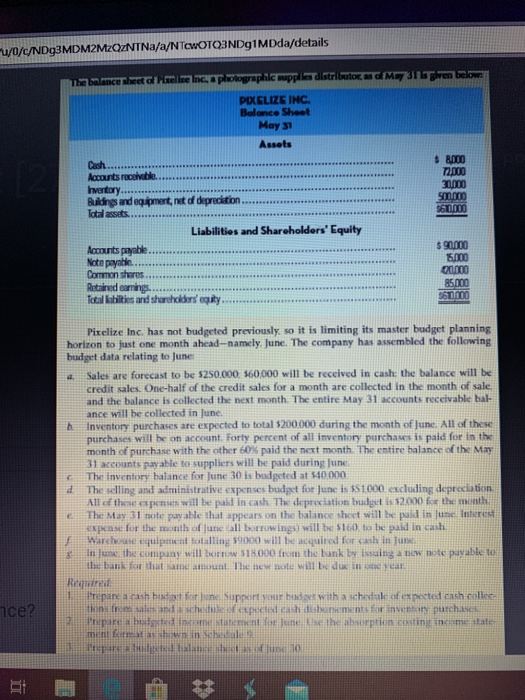

u/0/c/NDg3MDM2MZOZNTNa/a/NTCWOTQ3NDg1MDda/details The naceret M 311 given below elle Inc. a photographic mappila distributor PIXELIZE INC. Balance Sheet May 31 Assets $ 8.000 pom ST Lacourts

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

From Zero To Digital Hero Discovering Opportunities Navigating Challenges And Launching A Successful Online Business For Absolute Beginners

Authors: Nolan Stafford

1st Edition

180342592X, 978-1803425924