Answered step by step

Verified Expert Solution

Question

1 Approved Answer

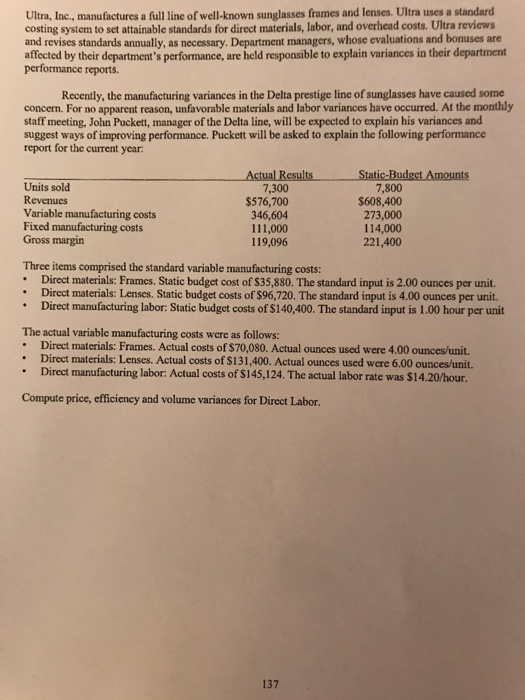

Ultra, Inc, manufactures a full line of well-known sunglasses frames and lenses. Ultra uses a standard costing system to set attainable standards for direct materials,

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Audit Planning Conduct And Closure Of Issues For Successful Resolution

Authors: Bincy Abraham, Imran Chaki, Naisarg Pujara

1st Edition

6200484961, 978-6200484963